Image © Adobe Images

Those hoping this week's key U.S. data drops would shift the dollar will be disappointed.

What we've learnt from midweek's two economic releases is that the economy is holding out, even if the labour market remains weak.

The dollar held recent highs against the pound and euro after the ISM Services PMI revealed a convincing return to growth for the U.S. private sector economy in October.

The reading of 52.4 was up from September's 50 and ahead of estimates for 50.8, pointing to a rebound in activity during the month.

But it's arguably what the report tells us about the U.S. jobs market that matters for markets, after all, future interest rate cuts at the Federal Reserve rest on the assumption that the labour market is still deteriorating.

The services PMI report's Employment Index contracted for the fifth month in a row with a reading of 48.2%, which is consistent with contraction.

Hints of a soft labour market were also forthcoming from the ADP report that showed job growth of 42K in October, which economists say is consistent with slowing employment.

"ADP's estimate suggests the labor market is continuing to cool gradually," says Samuel Tombs, Chief U.S. Economist at Pantheon Macroeconomics. "Labor market slack, therefore, likely continued to accumulate in October, suggesting the official data will make a strong case for the FOMC to ease again in December, if it’s available by then."

"The ADP report was better than expected, and showed a recovery from last month, but it was still enough to satisfy the narrative that the jobs market remains weak and needs more support from a rate-cutting Fed," says Chris Beauchamp, Chief Market Analyst at IG.

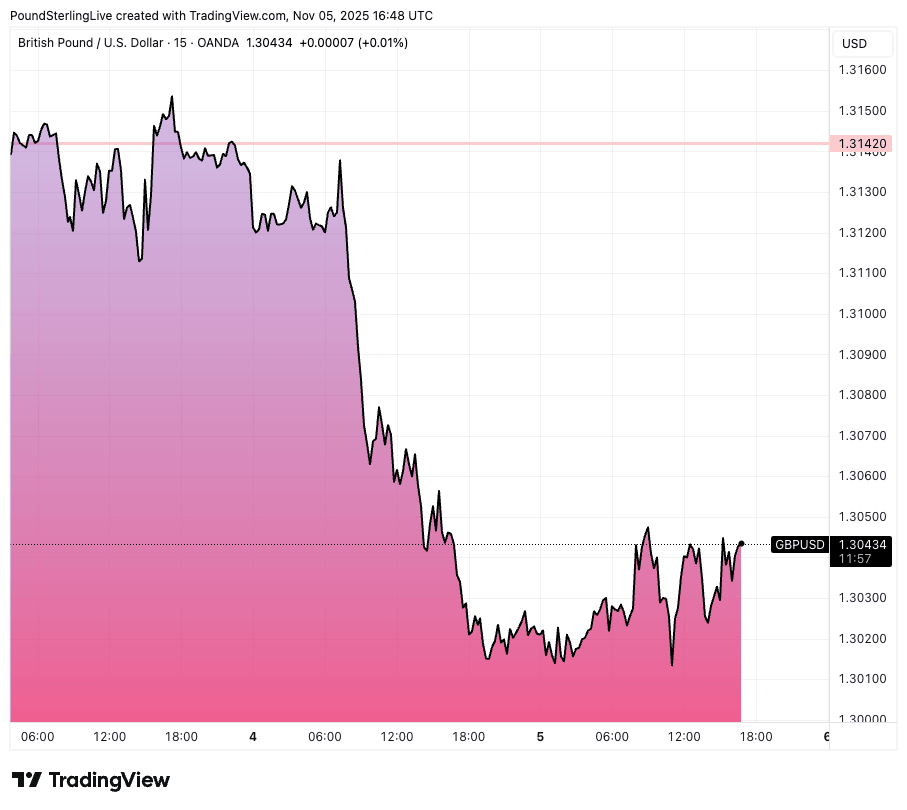

Above: GBP/USD stabilises after a tough couple of days.

Investors are increasingly focused on these private sector reports owing to the U.S. government shutdown, which means official agencies are unable to produce economic statistics.

This leaves the Federal Reserve unsure of how the labour market is progressing, and draws questions on whether or not another rate cut as soon as December is warranted.

For the dollar, this doubt is proving supportive. However, were odds of a rate cut begin to rise again, the currency could turn lower again, allowing GBP/USD to recover.

But there's nothing in this week's data to trigger such a shift, leaving the dollar with the upper hand.