Image © Adobe Images

The Pound to Dollar exchange rate can remain under pressure into a potential UK interest rate cut and Friday's U.S. jobs report.

This week's Bank of England decision will be the key focus for the Pound, and the market is currently split 50/50 on whether the Bank will proceed with a rate cut.

Elevated uncertainty means the market will be sensitive to the outcome, and we could, therefore, see some elevated volatility this week.

Our overall Week Ahead Forecast stance is to expect near-term softness as traders position for this possible volatility. This caution could reflect a weaker Pound-Dollar and a retreat towards 1.28 cannot be ruled out in the near term.

A retreat to this level would be made all the more likely if global equity markets continue to struggle; last week, we saw the Pound-Dollar come under pressure amidst a widespread stock market selloff, reminding us that the exchange rate is sensitive to broader sentiment.

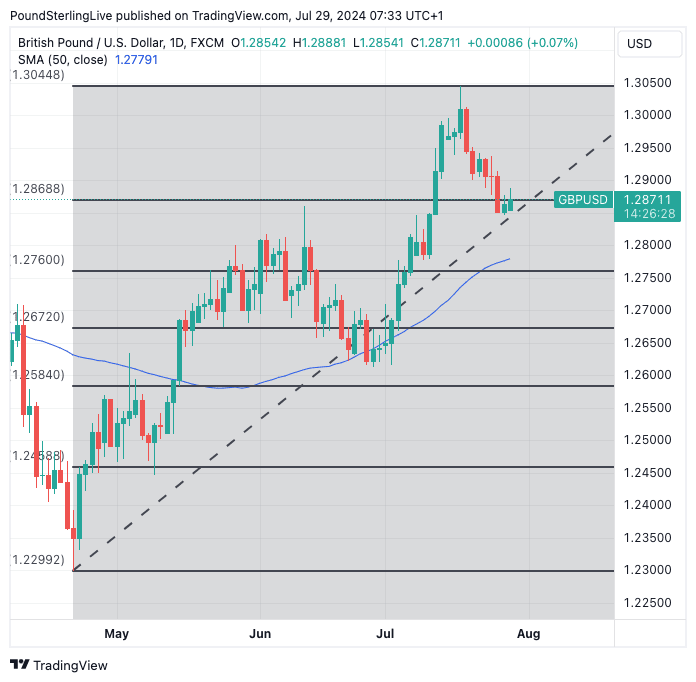

We think any weakness could see the exchange rate fall back to the 1.2760 area. This would be consistent with a 38.2% Fibonacci retracement of the April to July rally and bring the 50-day moving average (DMA) into play (1.2780). The 50 DMA arrested the June pullback, from where the uptrend reasserted.

Above: GBP/USD at daily intervals with Fibonacci retracement levels shown. Track GBP/USD with your custom alerts; find out more here

Markets are currently seeing little more than 50% chance of a rate cut on Thursday. To be sure, last week's weakness in the Pound reflects a rebuilding of these expectations, as the odds of a cut were closer to 40%.

Kamal Sharma, analyst at Bank of America, says, "headed into the rate meeting we think the risks are skewed asymmetrically to GBP weakness if the BoE cuts. Two factors suggest this: positioning as IMM GBP longs are crowded; and the rise in market volatility which historically has been bearish for the high beta currencies."

The market has built up a record-long position on the Pound over recent weeks as investors look for further outperformance. The risk is that this crowded positioning is washed out by any disappointment, exposing Pound exchange rates to a deep pullback.

"Should the BoE cut rates as we expect, by a likely 5:4 margin, with Governor Bailey having the casting vote, we would expect the GBP correction from recent 1.3044 highs to extend towards the mid-point of the year-to-date trading range, at 1.2672, once we clear strong support at 1.2765/75," says Jeremy Stretch, an analyst at CIBC Capital Markets.

Bank of America's Sharma says even in the case of a hawkish cut, he is inclined to think that markets will continue to sell GBP on the cut as positions are pared back. A 'hawkish cut' is when the Bank cuts rates but signals to markets that further cuts are not guaranteed and are dependent on upcoming data.

What if the Bank doesn't cut interest rates? This might offer some upside relief to the Pound, which can rebound into the end of the week, particularly if Friday's U.S. jobs report undershoots expectations.

However, GBP/USD upside will likely be limited as the Bank would almost certainly 'nail on' a September rate hike. "The conditions are in place for the MPC to cut, but we think they will wait until September to avoid surprising markets," says Andrew Goodwin, Chief UK Economist at Oxford Economics.

A firm commitment to a September rate cut would make this a 'dovish' hold, which is not entirely consistent with a rebound in the Pound.

Beyond the prospect for near-term weakness, Bank of America thinks the structural backdrop remains supportive of the Pound:

"With event risk out of the way, and the new Government seemingly in a hurry to announce policy, we look for further GBP upside in the months ahead. Carry remains supportive but near-term positioning is crowded," he explains.

This fits with the broader theme of near-term weakness ahead of a resumption of the rally at some point in the coming weeks.

Big Week for the Fed

Turning to the Dollar, the Federal Reserve policy decision is due Wednesday. No change in interest rates will be made. Instead, expect cautious guidance that is consistent with expectations for a first interest rate in September.

The market is now 'fully priced' for such an outcome, meaning the Dollar would rally if the Fed cast any doubt on firing the starting gun to a rate cutting cycle in September. We would anticipate the Fed to continue with its new strategy of highlighting concerns that keeping rates unchanged for too long could negatively impact the labour market.

This is consistent with the Fed saying it thinks it can afford to cut interest rates before inflation falls back to the 2.0% target.

The more important event for the Dollar comes on Friday when the U.S. jobs report is released. Should the data undershoot expectations the market will price in more policy easing from the Federal Reserve for the coming months, which will weigh on the Dollar.

July non-farm payrolls are expected to print at +178k, with the unemployment rate remaining at 4.1%. That follows a stronger-than-expected print of +206k in June.

"The bigger driver for USD would be on payrolls report and the next few inflation readings – to get a sense of the possible extent of rate cuts," says Christopher Wong, an analyst at OCBC.