Photo by Tim Brown, GPA Photo Archive.

The Pound to Dollar exchange rate (GBP/USD) will likely remain under pressure in the coming days, with bouts of strength likely to prove short-lived.

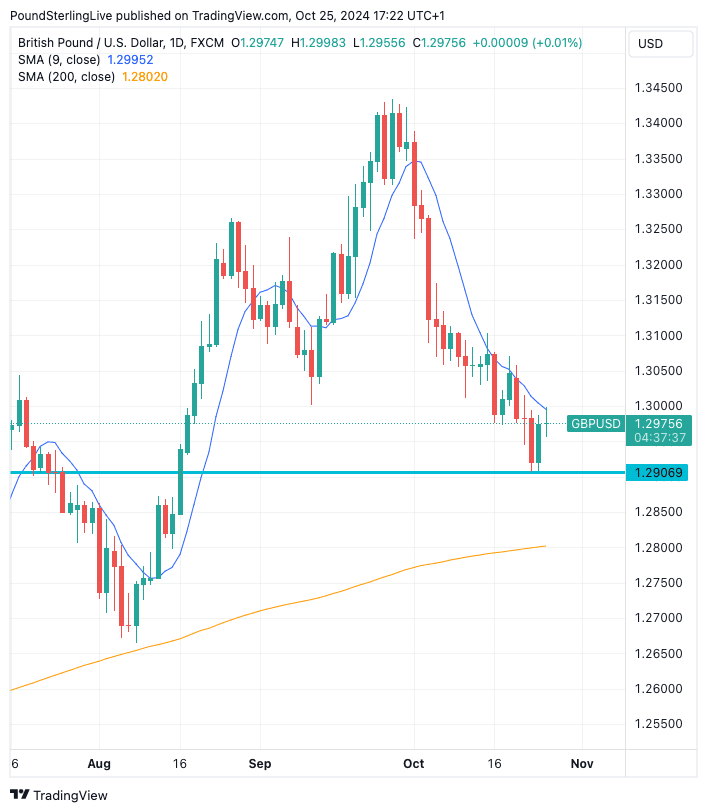

The previous edition of our GBP/USD Week Ahead Forecast said the downside was preferred as the exchange rate was capped by the nine-day moving average.

Fast-forward to this week, and the same remains true: the exchange rate is still being frustrated by the 9-day MA, with the downside preferred for the next five days, setting a target at 1.2909.

To be sure, U.S. Dollar momentum stalled through the latter half of the previous week, prompting some to think the downtrend was starting to fatigue.

GBP/USD attempted a rebound amidst a softening in the U.S. Dollar.

However, the rally failed at the 9-day MA at 1.2995, which signals a distinct lack of appetite to bet against the Dollar in the face of impending event risk.

Risk management fundamentals suggest standing in the way of GBP/USD weakness is unwise at this juncture and those looking to buy dollars should clear some of their exposure ahead of the U.S. vote next Tuesday.

Ahead of the November 05 election we have the U.S. non-farm payroll numbers to contend with, due Friday.

The Dollar's October assault has been underpinned by a tranche of above-consensus economic data releases that speak of a robust economy where further interest rate cuts from the Federal Reserve are not desperately needed.

Having entered the month thinking another 75 basis points of cuts were required of the Fed, the market is now consigned to expecting just one further cut.

To be sure, this repricing is substantial and could well be nearing its end, which can ease the downside pressure on GBP/USD and potentially spark a rebound and a period of consolidation.

But a strong U.S. labour market reading on Friday would likely aid U.S. bond yields and the Dollar and weigh on GBP/USD.

Expect the U.S. election to hold the market's focus through all this. What we have seen in recent days is that rising odds of a Trump win are consistent with Dollar strength.

To be sure, market-implied odds are settling around a 65% chance of a Trump win, and stabilisation around here could ease downside pressure GBP/USD in the coming days. (Why would you push out when the polling is still neck and neck?!).

That said, we think markets are going to remain nervous ahead of the vote, with uncertainty remaining high. This is fertile ground for the Dollar and can only add to the sense that GBP/USD is biased lower.

It's also a big week for Pound Sterling as the UK government will announce its budget on Thursday.

We know this is likely to be a difficult budget for businesses and investors and is, therefore, a potential headwind for growth. This could weigh on the Pound, particularly if the market thinks the new tax rises will lower the UK's growth potential.

However, analysis suggests the budget will be expansionary as the Chancellor has changed the UK's fiscal rules to allow her to borrow more money in order to invest in projects that would boost the UK's growth potential.

Some estimates suggest the boost to growth could amount to 0.50% in 2025, which would require the Bank of England to be more cautious in cutting interest rates. This would amount to a GBP-positive outcome.

Risks to the Pound would be the market not taking kindly to expectations for increased borrowing, similar to the reaction to Liz Truss' aborted mini-budget of 2022 that caused a meltdown in the Pound.

However, all analysts we follow say they have seen and heard enough to believe this is unlikely, so we think the budget is no significant downside risk to GBP.