Official White House Photo by Shealah Craighead

GBP/USD could come under renewed pressure as a recent relief-style rally fades on fresh Trump talk and U.S. data is set to come back into focus.

Fresh tariff threats from President-elect Donald Trump over the weekend are helping the Dollar reassert itself at the start of the new week.

The Pound to Dollar exchange rate (GBP/USD) is lower at 1.2696 on Monday, in sympathy with the broader rally in the USD that follows Trump's threat to levy a 100% tariff on BRIC countries.

"The idea that the BRICS Countries are trying to move away from the Dollar while we stand by and watch is OVER. We require a commitment from these Countries that they will neither create a new BRICS Currency, nor back any other Currency to replace the mighty U.S. Dollar or, they will face 100% Tariffs," said Trump on social media.

"The USD was the outperforming currency during the Asian session following a social media post by US President-elect Donald Trump saying he wanted the USD to maintain its reserve currency status," says David Forrester, Senior FX Strategist at Crédit Agricole.

One week after Trump threatened Canada, Mexico, and China with tariffs, the latest development confirms that Trump is already using tariff threats to pursue his geopolitical agenda.

This makes for a highly uncertain environment for financial markets as there is no economic template that would allow traders to anticipate where tariffs will land and how significant they will be.

"It's unclear how 100% tariffs on a group of countries that make up 37% of global GDP would happen in practice, but serves as a possible preview of tariff diplomacy under Trump 2.0," says Michael Wan, Senior Currency Analyst at MUFG Bank Ltd.

On the other hand, Trump's approach leaves ample space for countries to negotiate with the Trump administration, which opens the door to worst-case scenarios being avoided.

"The impact of Trump on the USD is going to be anything but linear. Instead, we expect more twists and turns and the short-term impact might look very different than the longer term impact," says a note from TD Securities.

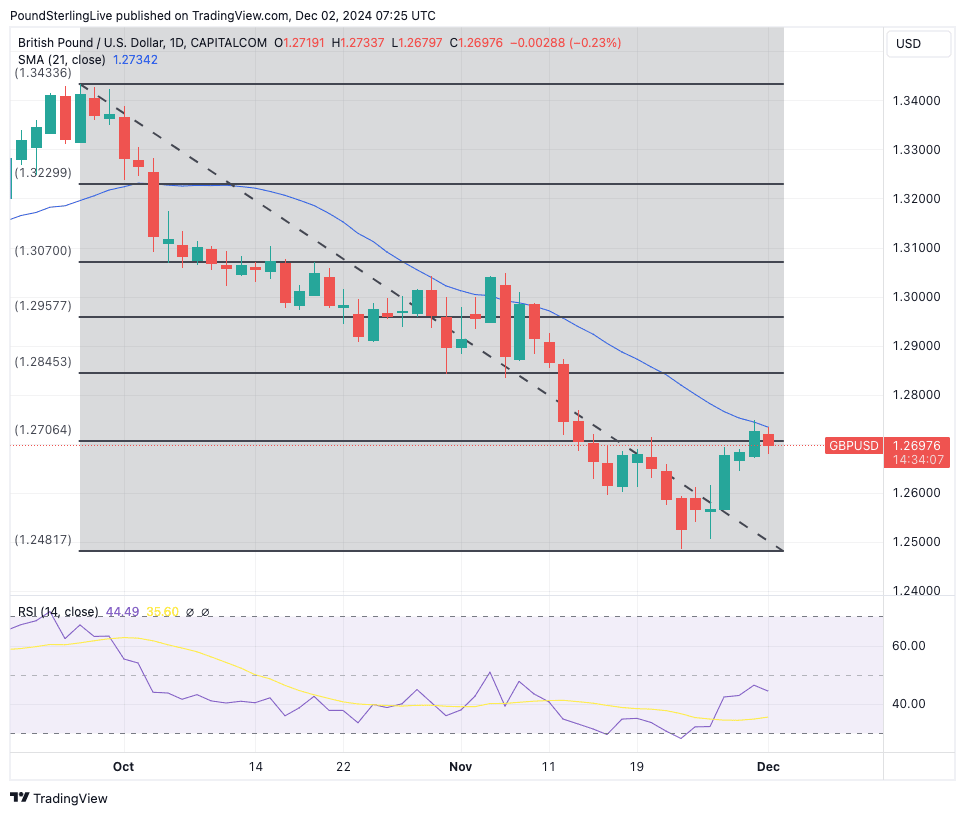

The Dollar's rebound at the start of the new week suggests the Pound-Dollar exchange rate might now be capped at the descending 21-day moving average, which is annotated in the below chart:

Also note that the GBP/USD rebound appears to have found some resistance at the 23.6% Fibonacci retracement of the recent November selloff, which coincides with the meeting of the descending 21 DMA.

The RSI is at 43 (lower panel in the above), which is relatively neutral, but we also note that it has turned lower, which could be confirmation that momentum has once again shifted to the downside.

Taking a step back, the overall trend remains to the downside, given the exchange rate is below its 200-day moving average. This means GBP/USD rallies will likely be shallow and strength will be sold into.

"We continue to favour fading GBP/USD rallies up to the 20 November high at 1.2715," says Jeremy Stretch, FX Strategist at CIBC Capital Markets.

Looking forward to the coming days, U.S. data will take control of the agenda once more.

The ISM manufacturing release is due Monday, where a reading of 47.5 is expected, consistent with the broader retreat the global manufacturing sector is currently experiencing.

Federal Reserve policy-setter Waller is due to speak today, which could shed some light on the prospects for further rate cuts in 2025. Williams is also due to speak later in the day.

Kugler and Goolsbee are due to speak on Tuesday.

Wednesday has the more important services PMI release from the ISM, which will give a more accurate insight on how the broader economy is evolving, which could elicit more of a reaction from the Dollar.

The PMI is expected to read at a healthy 55.5%.

Friday is the more important day as we will receive the U.S. employment report, where analysts expect 183K jobs to have been created in November.

Anything less will bolster rate cut expectations, which can weigh on the Dollar.

Also, keep an eye on average hourly earnings, which are expected to have risen 0.3% month-on-month in November, while the unemployment rate is expected to steady at 4.1%.

One of the major themes in global FX since September has been the robust nature of U.S. economic data that saw a rapid reappraisal of the number of times the Fed can realistically cut rates.

This has bolstered the Dollar, with Trump's win in the November election giving the rally fresh impetus.

To be sure, much good news is already priced into the Dollar, and we wonder whether 'peak USD' is at hand.

Also, note that December is traditionally a month of USD weakness, and if history repeats, the GBP/USD could find itself better supported in the coming weeks.