Image © Adobe Images

The Pound to Dollar (GBP/USD) exchange rate looks set to carve out a shallow rebound in the coming days, but this mustn't be mistaken for strength.

After all, the more significant trend in GBP/USD is to the downside.

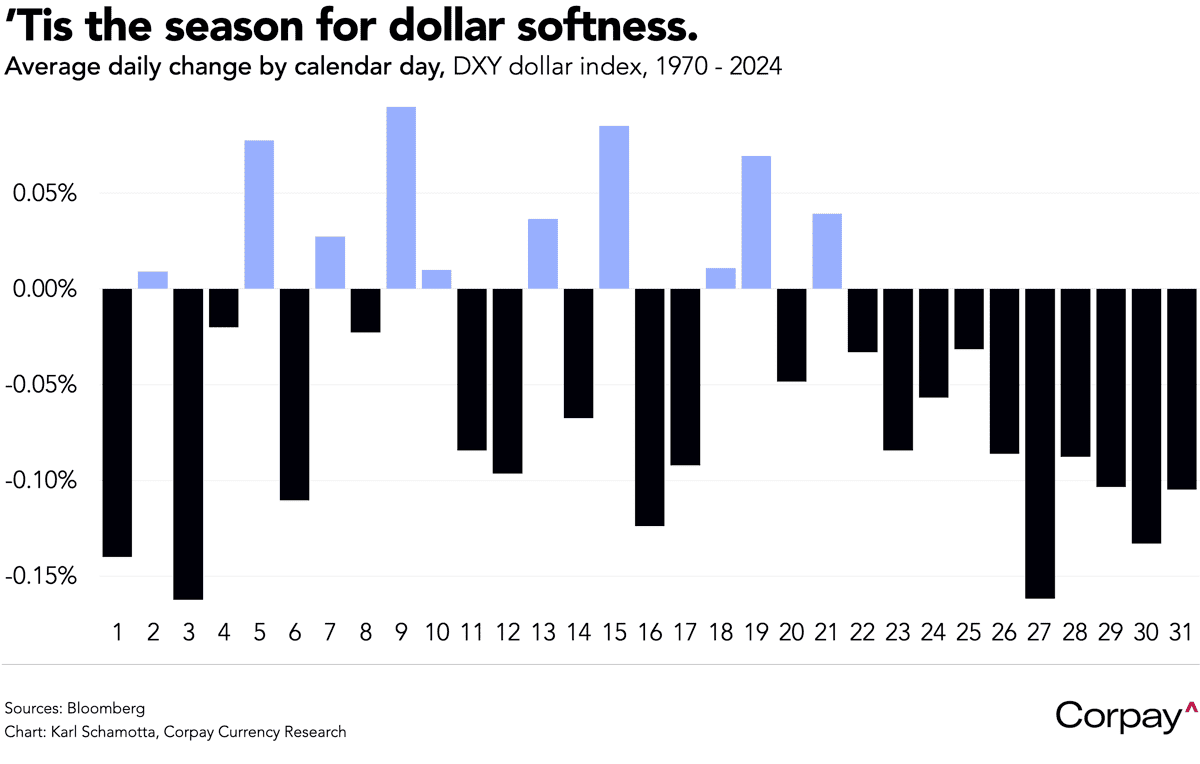

That trend has been paused, and the exchange rate entered a consolidation pattern this December, consistent with a strong seasonal signal that shows December is a month in which the dollar tends to decline.

Near-term strength will require this week's busy calendar, which includes two central bank decisions, inflation and labour market data, to land favourably.

Pound Sterling was bid on Monday, thanks partly to an above-consensus reading from the UK's Services PMI for December, with S&P Global saying the UK's services PMI rose to 51.4 in December from 50.8 in November, beating expectations for 50.9.

However, the report's details that the UK economy has cooled notably since the first half of the year will limit the upside in GBP/USD. S&P Global said survey respondents widely commented on growth headwinds from fragile consumer confidence, tighter corporate budgets, and cutbacks to non-essential spending.

A marked labour market deterioration is a risk to the Pound in 2025, with S&P Global saying employment fell in December at the fastest rate since the global financial crisis in 2009 (if the pandemic is excluded) due to the jobs tax introduced by the new Labour government in October.

Although fundamental headwinds are blowing, it won't be until 2025 that the official ONS data verifies the findings presented by survey data.

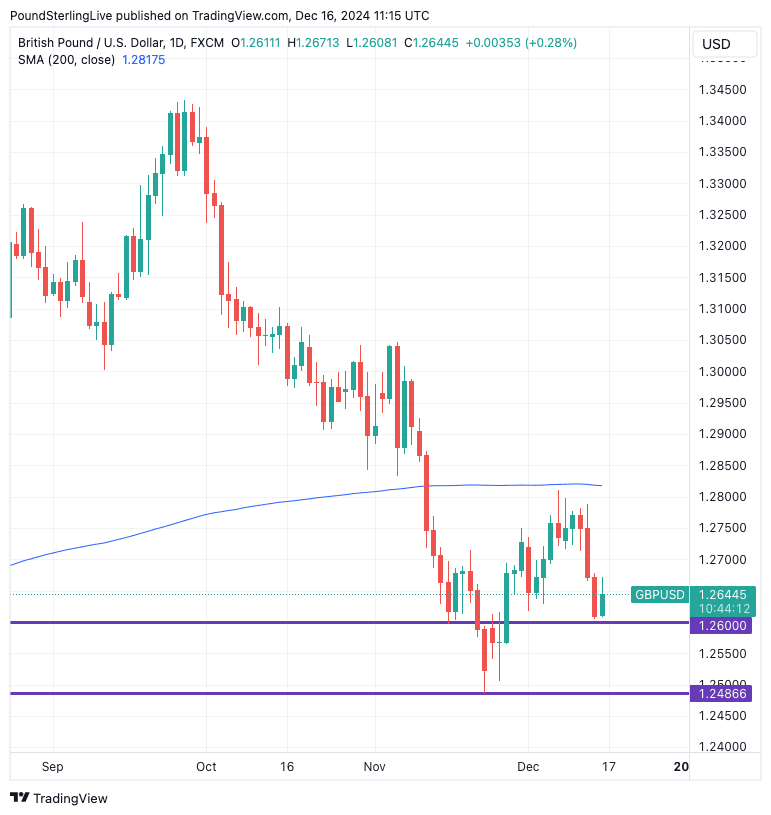

Near-term, therefore, there is scope for GBP/USD to firm, as the daily chart suggests Monday's bid reinforces a horizontal support level that is found at 1.26:

A recovery back above 1.27 is possible if Tuesday's labour market statistics reveal an ongoing stubbornness in UK wages, which would be consistent with the Bank of England keeping interest rates unchanged on Thursday.

Wednesday will prove to be a key test for Pound-Dollar, with UK inflation numbers due for release in the London morning and the U.S. Federal Reserve decision due in the evening.

UK inflation is expected to tick up, as it journeys back to the 3.0% level, putting it further out of reach of the Bank of England's 2.0% target.

The Federal Reserve will cut interest rates by 25 basis points in a move that is now fully absorbed by the Dollar.

However, new forecasts will be released by the Fed, which should give a gauge as to how many cuts are likely in 2025.

The market has already slashed expectations and it is difficult to see the Fed giving the kind of guidance that would lower expectations even further, which poses a headwind to the Dollar.

This opens the door to further drift in GBP/USD.

Perhaps the biggest risk to Sterling exchange rates comes on Thursday when the Bank of England will give its latest interest rate decision. Here, rates are expected to remain unchanged.

The vote composition for the decision will potentially move GBP/USD, with the risk being that a number of policy setters vote for a cut, which implies they are keen to get on with the job.

Yet, it is clear their hands are tied given the drift higher in inflation, and any weakness in GBP/USD stemming from the Bank of England will be limited.

Indeed, the headline is that the Bank will likely cut only four times in 2025, which can ensure that the Pound retains much of its support from the UK's elevated interest rates.

But, the U.S. Dollar also has high interest rate settings behind it, plus a strong economy.

The conditions for ongoing Dollar strength are firmly in place, underscoring the view that the broader trend for GBP/USD remains bearish. There is a decent probability of a return to the 1.2486 November 22 low in early 2025.