Image © Adobe Images

Pound Sterling's selloff against the Dollar reflects fears the UK economy is firmly in stagflationary territory.

The Pound to Dollar exchange rate dropped by nearly 1.0% to reach 1.2376 after the Bank of England unleashed a series of stagflationary growth forecasts.

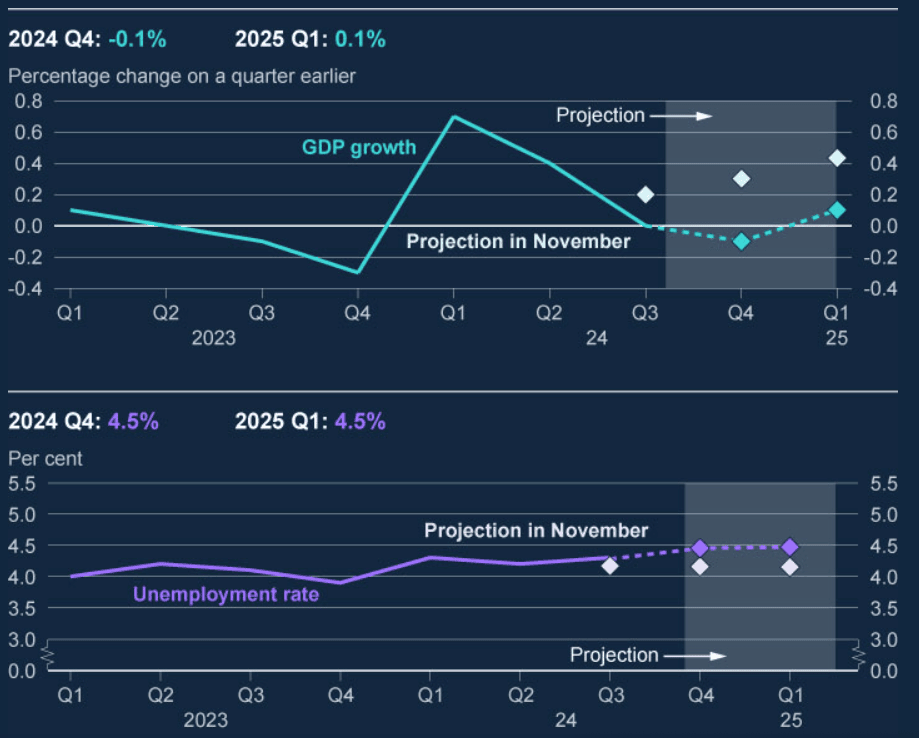

The Bank's updated GDP growth forecasts show annual growth is at just 0.4% by the end of the first quarter, drastically lower than the 1.4% forecast issued in the November Monetary Policy Report.

"Prospective growth challenges and data dynamics, impacting March pricing, supports the notion of GBP retreating towards 1.2230," says Jeremy Stretch, Chief International Strategist at CIBC Capital Markets, of the GBP/USD's near-term outlook in the wake of the Bank's latest guidance.

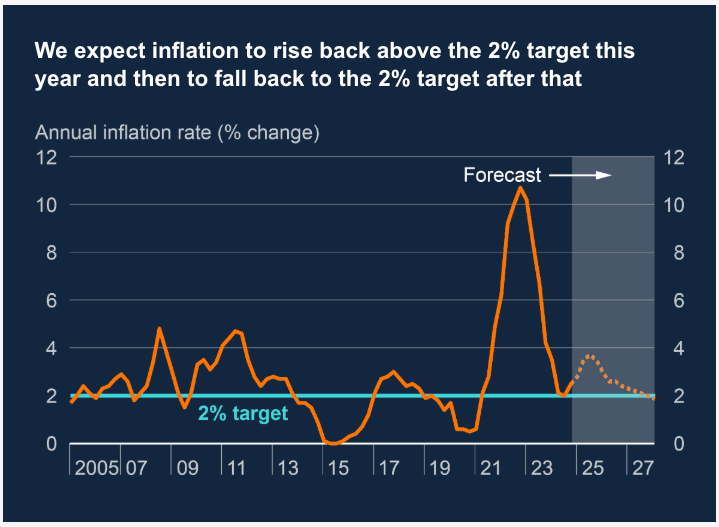

The new inflation projections add nearly a full percentage point to the peak: the 2025 Q3 CPI forecast is revised up to 3.7% from 2.8% previously.

Low growth and high inflation have the makings of a stagflationary environment, which is traditionally negative for a currency.

The Pound has lost notable ground against all its major peers on the day. However, weakness could soon fade as it is clear the Bank won't be able to deliver much more than three further cuts this year, given the troubling inflationary outlook.

"The Bank also provided a surprisingly hawkish set of forecasts, warning that inflation could accelerate 'quite sharply' later this year before subsiding, and outlining a policy path that includes just two more cuts over the next three years. The pound’s losses may prove somewhat limited," says Karl Schamotta, Chief Market Strategist at Corpay.

Fears of stagflation explain why two members of the Bank's Monetary Policy Committee (MPC) voted to cut interest rates by a more aggressive margin of 50 basis points, judging that boosting inflation was a price worth paying to save growth.

However, such aggression is at odds with the Bank's mandate to bring inflation back to the 2.0% target and risks embedding higher inflation expectations amongst businesses and consumers.

The latest growth projections reflect weaker business confidence, softer investment activity, and persistent inflationary pressures that continue to weigh on the UK economy.

Updated GDP Growth Forecasts:

- 2025 Q1: 0.4% (previously 1.4% in November 2024)

- 2026 Q1: 1.5% (previously 1.6%)

- 2027 Q1: 1.3% (previously 1.1%)

- 2028 Q1: 1.8%

Updated Inflation Forecasts:

- 2025 Q3: 3.7% (previously 2.8%)

- 2025 Q4: 3.5% (previously 2.7%)

- 2026 Q1: 3.0% (previously 2.6%)

- 2027 Q4: 2.0%, aligning with prior expectations

The sharp downward growth revision for 2025 comes as business investment sentiment weakens and external demand slows. The BoE also cited fiscal tightening measures and continued restrictive monetary policy as factors holding back growth in the near term.

However, the Bank expects a gradual recovery from mid-2025 onwards, with growth reaching over 1.5% by the end of the forecast period, supported by stronger consumer spending and easing financial conditions.

The latest report also signals a deterioration in the UK labour market, with higher unemployment forecasts and slower employment growth. The BoE now projects a gradual rise in unemployment, reflecting softening demand for workers and weaker hiring intentions among businesses.

The Unemployment Rate (2025 Q4) is seen rising to 4.75%, whereas the peak was seen at 4.5% as of the November forecast.

The Bank pointed to declining private sector payroll employment and rising employer costs, including higher National Insurance Contributions (NICs), as key factors affecting hiring decisions. Weaker business sentiment and reduced vacancy levels further reinforce expectations of a looser labour market in the coming quarters.

Despite these downward revisions, the BoE maintains that the UK economy will eventually recover, with growth rebounding from mid-2025 and inflation pressures easing over the medium term.