Image © Adobe Images

Pound Sterling's recovery against the Dollar has been boosted of late by hopes of an end to the war in Ukraine, but technicals hint that a temporary setback at the 1.26 resistance level is possible.

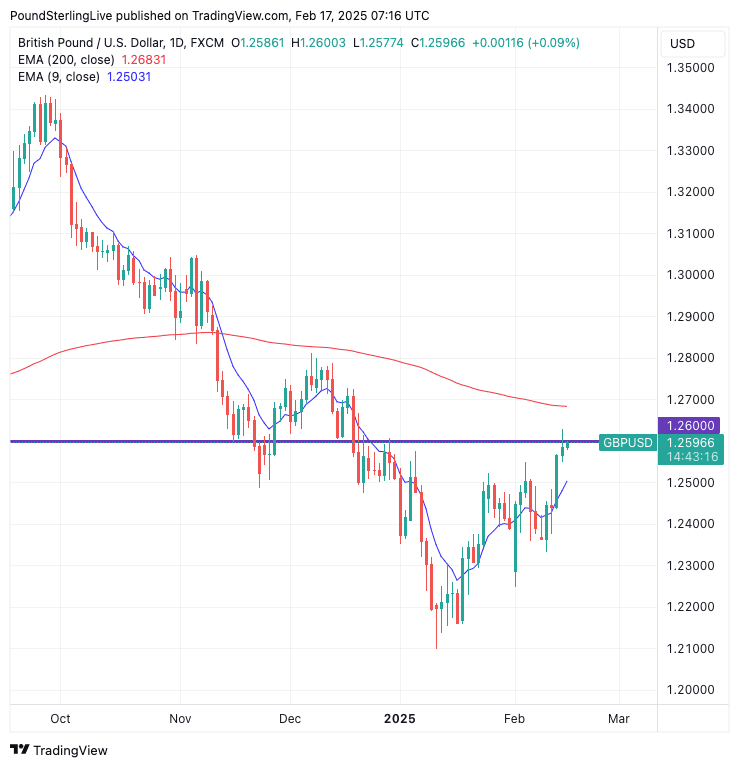

The Pound-to-Dollar exchange rate (GBPUSD) advanced 1.57% last week as it recorded its third weekly gain in four and firms out the interim floor that could put an end to the multi-month fall that started last September.

The recovery takes GBPUSD to 1.26 on Monday morning, a level that could provide some interim resistance. This, and the wide divergence from the nine-day exponential moving average (EMA) that has built up, leaves us anticipating a near-term pullback on a one to two-day timeframe, allowing the recovery to take a breather.

The nine-day EMA is a useful tool as it shows where near-term momentum lies, which can be helpful for predicting in the short-term timeframe, which is always a difficult prospect in currency markets. We also note exchange rates tend to hug the nine-day EMA, which means the emergence of big gaps tends to advocate for mean-reversion action.

On this basis, a decline to approximately 1.2530 is possible as the market recalibrates.

Above: GBPUSD could revert back to the 9-day EMA amidst an evolving recovery.

However, for now, weakness is expected to be shallow, and a decisive break above 1.26 is preferred. This is because last week saw GBPEUR move above the 50-day EMA, confirming near-term momentum has turned higher and advocates for gains on a multi-day timeframe.

The next major technical target is located at 1.2693, where resistance will likely be found. Should the exchange rate break above this level, then we would confirm the trend has flipped from medium-term bearish to medium-term bullish, and a multi-week rally is underway.

Technicals aside, Pound Sterling's recovery rests with hopes for a potential ceasefire and peace in Ukraine, which particularly supports European currencies.

"Hopes of a Ukrainian peace deal help lift Sterling and Euro," says a market note from Lloyds Bank.

In addition, the fear of tariffs is losing its grip on markets, which is weighing on the Dollar more broadly.

"It seems that each successive tariff announcement seems to be having less of an impact on markets. Markets seemed more interested in Trump's announcement that he had talks on Ukraine with Russian leader Putin. That has helped drive a bounce in both the euro and sterling against the dollar to their highest in around three weeks, despite there being little indication that these talks will produce a concrete outcome," adds the Lloyds Bank note.

The geopolitical situation involving Ukraine is moving rapidly, and we will be watching headlines for any positive developments, while it appears it won't be until April when we get substantive tariff news.

GBP Eyes, Wage Inflation Data

There's also a busy economic calendar to look forward to this week, which can drive GBPUSD volatility.

The UK calendar will be busy this week and offers some GBP-specific GBPEUR volatility.

The UK's data pulse is in the process of recovering, having cratered after the country came under new management following last year's July election.

With expectations so low, the prospect of upside surprises has grown, particularly on the inflation front, which can boost the Pound.

Here’s a breakdown of key UK economic events scheduled for next week, along with market expectations:

Tuesday, February 18

? Average Weekly Earnings (Dec, YoY)

Inc. Bonuses: 5.9% (expected) vs. 5.6% (previous)

Ex. Bonuses: 5.9% (expected) vs. 5.6% (previous)

? Market Impact: A higher-than-expected figure could reinforce inflationary wage pressures, which would imply the Bank of England has little scope to accelerate the rate cutting cycle. This would be supportive of GBPUSD.

? ILO Unemployment Rate (Dec)

Expected: 4.5%

Previous: 4.4%

? Market Impact: If unemployment rises, it could signal the labour market is softening, potentially weakening GBP.

? Employment Change (Dec, 3m/3m)

Expected: 50K

Previous: 35K

? Market Impact: A strong reading indicates resilient hiring trends, supporting growth and possibly keeping wage growth elevated.

? BoE Governor Andrew Bailey Speaks

? Market Impact: If Bailey delivers hawkish remarks, GBP may strengthen as markets price in fewer rate cuts in 2025. A dovish tone could weigh on GBP.

Wednesday, February 19

? Consumer Price Index (CPI) (Jan, YoY & MoM)

MoM Expectation: -0.3% vs. -0.2% (previous)

YoY Expectation: 2.8% vs. 2.8% (previous)

Core CPI (YoY): 3.7% vs. 3.2% (previous)

? Market Impact: A slowdown in inflation would increase the probability of BoE rate cuts later in 2025, weighing on GBP. However, economists see building upside risks for inflation this year, and a stronger print could make the case for the Bank of England to grow increasingly cautious about further rate cuts. This would boost GBPEUR.

? CBI Industrial Trends Orders (Feb)

Expected: -30

Previous: -34

? Market Impact: A higher-than-expected figure suggests improving UK manufacturing sentiment, but the sector remains weak overall.

Week Ahead: USD

Tuesday, February 18

? Empire State Manufacturing Index (Feb)

Expected: -1.0

Previous: -12.6

? Market Impact: A negative but improving figure suggests continued weakness in the manufacturing sector, but if the number beats expectations, it could provide a mild boost to USD.

Wednesday, February 19

? Building Permits (Jan, Preliminary MoM)

Expected: -2.3%

Previous: -0.7%

? Market Impact: A decline in permits suggests weakness in the housing sector, which could weigh on economic growth prospects.

? Housing Starts (Jan, MoM)

Expected: -7.0%

Previous: 15.8%

? Market Impact: A sharp decline may raise concerns about the real estate market, potentially dampening growth outlooks.

? FOMC Meeting Minutes (Jan 31 Meeting)

? Market Impact: The minutes will provide insight into Federal Reserve discussions on interest rates. If the Fed signals a more hawkish stance (delayed rate cuts), USD could strengthen. A dovish tone (softer inflation concerns) could weaken USD.

Thursday, February 20

? Initial Jobless Claims (Feb 15 Week)

Expected: 215K

Previous: 213K

? Market Impact: Low jobless claims suggest a strong labor market, which could reinforce higher-for-longer Fed rate expectations, supporting USD.

? Philadelphia Fed Manufacturing Index (Feb)

Expected: 25.4

Previous: 44.3

? Market Impact: A drop suggests slowing manufacturing activity, which may raise recessionary concerns if it continues.

? Eurozone Consumer Confidence (Feb, Preliminary)

Expected: -14.0

Previous: -14.4

? Market Impact: If consumer confidence improves, it may reduce recession fears, stabilizing USD against EUR.

Friday, February 21

? Markit Services PMI (Feb, Preliminary)

Expected: 53.5

Previous: 52.9

? Market Impact: A reading above 50 signals expansion, which is positive for USD as it suggests continued economic strength.

? Markit Manufacturing PMI (Feb, Preliminary)

Expected: 51.5

Previous: 51.2

? Market Impact: A stable or rising figure may indicate ongoing manufacturing recovery, which could support USD strength.

? University of Michigan Consumer Sentiment (Feb, Final)

Expected: 68.5

Previous: 67.8

? Market Impact: Higher consumer sentiment may indicate strong consumer spending ahead, which could reinforce positive economic outlooks and bolster USD.

? Existing Home Sales (Jan, MoM)

Expected: -2.1%

Previous: 2.2%

? Market Impact: A decline in home sales suggests weakness in the housing market, which could temper economic optimism.