File image of Elon Musk. Photo credit: NASA/Kim Shiflett.

U.S. economic outperformance has been a driver of Dollar outperformance since the pandemic, but it could finally be ending thanks in part to Elon Musk's (Department of Government Efficiency (DOGE).

The U.S. economy has remained resilient in the face of global economic uncertainty, but looming DOGE-related job losses and elevated policy uncertainty could pose headwinds to its outperformance, according to Torsten Sløk, Chief Economist at Apollo Global Management.

The Dollar was the best-performing major currency through the second half of 2024 as U.S. economic exceptionalism came to the fore with a solid run of above-consensus data releases.

However, Sløk cautions that "the near-term downside risks to the economy and markets are growing."

"Torsten Slok, who has been adamant and correct on the US economy for a long time (bullish) is turning more cautious and I think that’s worth paying attention to," says Brent Donnelly, founder of Spectra Markets. "It’s hard to say when the DOGE stuff will show up in the economic data, but the plunge in the S&P PMI on Friday might be a tell."

If data begins to underperform, the market will move to 'price in' additional Federal Reserve rate hikes over the coming months, lowering U.S. bond yields, which would mechanically weigh on the Dollar.

DOGE is a temporary government department led by Elon Musk, whose purpose is to carry out President Donald Trump's agenda of cutting federal spending and deregulation and boosting productivity.

Market consensus expects around 300,000 DOGE-related job cuts, but Sløk warned that the real number could be significantly higher when including contract workers.

Work by the Brookings Institution has shown that for every federal employee, there are two contractors. Based on this, says Slok, layoffs could potentially be closer to 1 million.

With 7 million unemployed in a 160-million-strong U.S. labour force, Sløk noted that the job losses might appear marginal.

However, he emphasised that such a shock could still "push jobless claims higher over the coming weeks," potentially pressuring the Federal Reserve’s policy outlook.

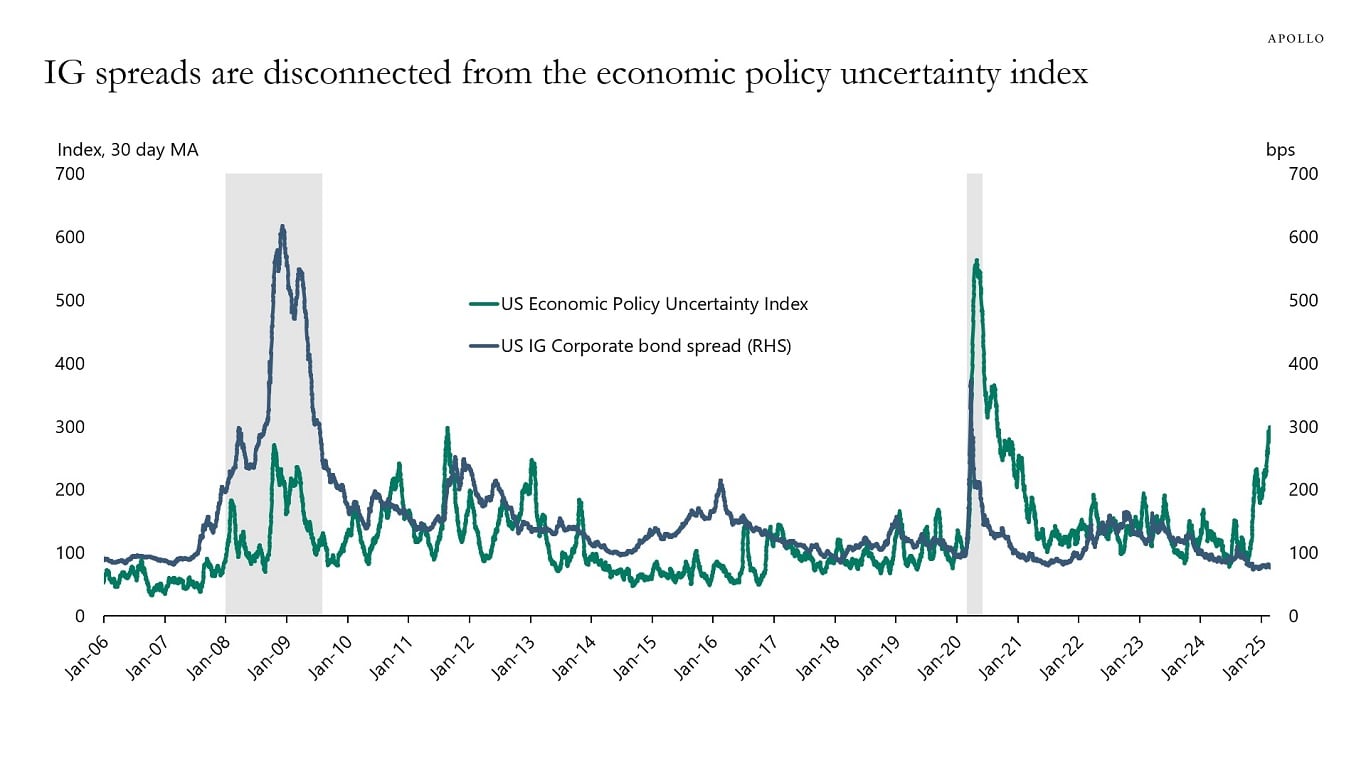

Despite rising economic policy uncertainty, financial markets have not reacted as expected, Sløk said.

"Credit spreads have not responded the way they normally do to rising policy uncertainty," he noted, pointing to historical trends where risk premiums typically widen in such conditions.

Sløk warns this prolonged uncertainty could start affecting corporate investment decisions, particularly capital expenditures (capex) and hiring.

"The question is whether persistently elevated policy uncertainty will begin to have a negative impact on capex spending and hiring decisions," he wrote.

For now, key indicators remain robust, supporting the narrative of U.S. growth exceptionalism in the global economy.

"The incoming data remains strong," Sløk said. "But we are starting to worry about the downside risks."

The consensus amongst institutional analysts is that 2025 will see the big USD trend turn, with most seeing the high tide around mid-year.

However, if Apollo's Slok is correct, it could be upon us.