Above Howard Lutnick confirmed tariffs on Mexico and Canada would proceed this week. File image of Howard Lutnick. Copyright Pound Sterling Live, still source: U.S. Gov.

Pound Sterling fell against the Dollar last week but could resume higher if the U.S. prints underwhelming data and Trump delays tariffs on Canada and Mexico.

Indeed, this is an important week for the tariff trade as Canadian and Mexican import tariffs are due to be confirmed on Tuesday.

We know from Commerce Secretary Howard Lutnick's Sunday media round that they are proceeding. However, there is ample scope for a delay and the final measures to be less severe than first touted:

"There are going to be tariffs on Tuesday on Mexico and Canada, exactly what they are, we're going to leave that for the president and his team to negotiate," he said.

The comments confirm that the advertised blanket 25% import tariff is likely to be avoided, which would prompt some relief for the CAD and MXN, as well as tariff-sensitive currencies such as the EUR.

For the USD, any watering down or delay would trigger weakness.

"The main risk to our view of a higher USD this week is if President Trump reverses or delays increases to tariffs that are scheduled for Tuesday 4 March (US time). In this case, the USD would fall by at least 1%," Kristina Clifton, Senior Currency Strategist at Commonwealth Bank.

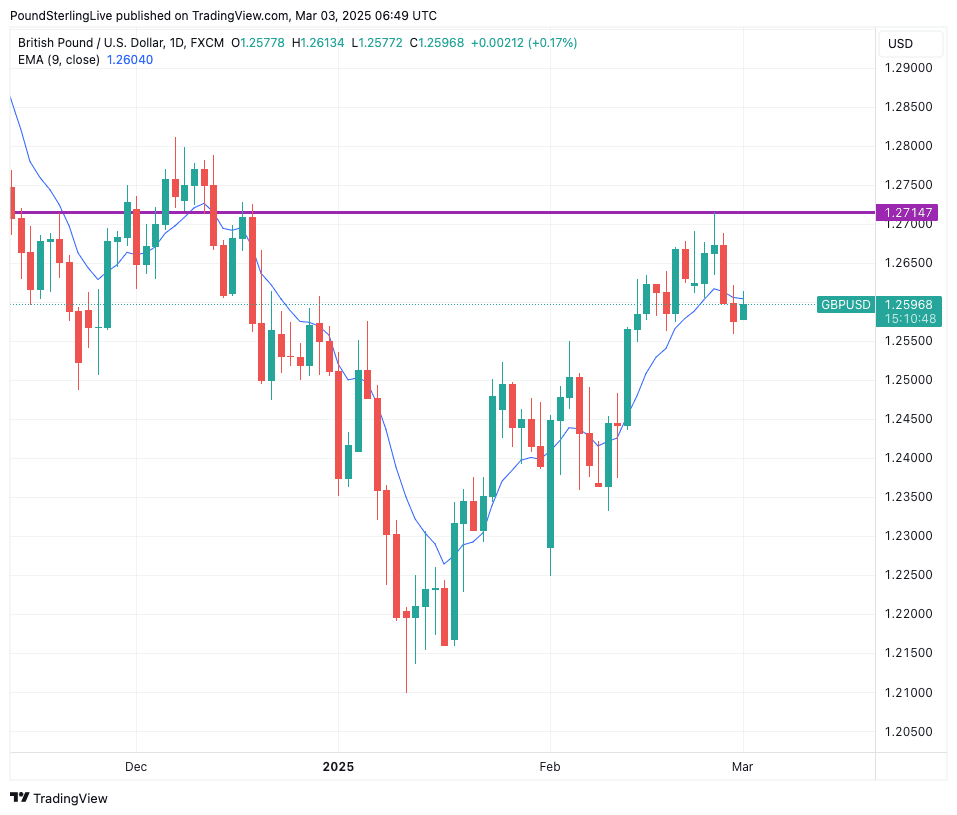

Under such a scenario, we would forecast GBP/USD to retest the 2025 high at 1.2714.

Above: GBPUSD at daily intervals.

We think the USD can resume lower against the GBP because we suspect Trump will want to avoid the full inflationary impact of tariffs while also being keen to avoid any damaging reciprocal tariffs.

He will point to concessions by Canada and Mexico and efforts to reduce the flow of drugs across the border as signs of success, allowing him to announce a more nuanced tariff regime.

The Pound-to-Dollar exchange rate (GBPUSD) last week dipped below the nine-day exponential moving average (EMA) at 1.2640, which confirms a near-term, multi-day stint of weakness is underway.

Based on this technical observation alone, we would expect a week of losses ahead.

However, the two-way tariff risks associated with the tariff announcements suggest that we should not overestimate the predictive power of this technical indicator this week.

A Busy Event Calendar

While there is little to look forward to in the UK, the U.S. has a busy calendar that culminates in the job report.

Monday, March 3

? Markit Manufacturing PMI (Feb, Final)

Expected: 51.8

Previous: 51.6

? Market Impact: A stronger reading above 50 signals expansion in the manufacturing sector, which could support USD. A miss could indicate slower growth, weighing on sentiment.

? ISM Manufacturing PMI (Feb)

Expected: 50.5

Previous: 50.9

? Market Impact: A reading near or above 50 suggests continued expansion, supporting the Fed's higher-for-longer rate stance, which may boost USD.

? Construction Spending (Jan, MoM)

Expected: -0.1%

Previous: 0.5%

? Market Impact: A decline in construction spending suggests weaker housing sector activity, which could weigh on GDP growth outlooks and limit USD gains.

Wednesday, March 5

? ADP Employment Change (Feb)

Expected: 150K

Previous: 183K

? Market Impact: A stronger-than-expected reading could signal continued labor market strength, reinforcing the Fed’s cautious rate-cut approach, which would support USD. A weak print may raise concerns about slower job growth, potentially weakening USD.

? ISM Services PMI (Feb)

Expected: 53.0

Previous: 52.8

? Market Impact: Services are a dominant part of the U.S. economy. A reading above 50 suggests expansion, reinforcing Fed hawkishness and boosting USD. A miss below 50 could undermine USD strength.

? Factory Orders (Jan, MoM)

Expected: 1.4%

Previous: -0.9%

? Market Impact: An increase suggests improving manufacturing demand, which may support GDP growth and USD. A miss could weaken USD sentiment.

Thursday, March 6

? Initial Jobless Claims (Week of March 1)

Expected: 230K

Previous: 242K

? Market Impact: A lower-than-expected print signals a strong labor market, reinforcing Fed’s hawkish stance and supporting USD. A sharp rise could signal labor market cooling, potentially weighing on USD.

? Trade Balance (Jan)

Expected: -$129.0B deficit

Previous: -$98.4B deficit

? Market Impact: A larger trade deficit could weaken USD by signaling higher import demand and potential slowing exports. A narrower deficit would be USD-positive.

Friday, March 7

? Nonfarm Payrolls (Feb)

Expected: 185K

Previous: 143K

? Market Impact: A strong jobs report reinforces economic resilience, pushing back rate cut expectations and boosting USD. A disappointing print could weaken the dollar.

? Average Hourly Earnings (Feb, MoM & YoY)

Expected: 0.3% MoM (4.2% YoY)

Previous: 0.5% MoM (4.1% YoY)

? Market Impact: Wage growth is a key inflation driver. A higher-than-expected reading could reinforce inflation concerns, boosting USD. A weaker print may ease inflation fears and weaken USD.

? Unemployment Rate (Feb)

Expected: 4.0%

Previous: 4.0%

? Market Impact: If the unemployment rate remains stable, it supports USD. A higher reading may pressure USD downward.

? Fed Chair Powell Speaks at Chicago Booth 2025 US Monetary Policy Forum

? Market Impact: Powell’s remarks could set the tone for future rate cuts. Hawkish signals (suggesting no rush to cut rates) would support USD, while dovish guidance may weaken it.

Potential Market Implications for USD

✅ Bullish (USD Strengthening) Scenarios:

Stronger-than-expected labor market data (NFP, ADP, jobless claims) reinforces Fed’s higher-for-longer stance, delaying rate cuts.

ISM & Services PMI readings above 50, signaling continued economic expansion.

Powell delivers a hawkish speech, maintaining a cautious approach to rate cuts.

Lower trade deficit signals stronger exports, supporting GDP and USD.

❌ Bearish (USD Weakening) Scenarios:

Weak NFP or ADP data, suggesting job market cooling, increasing rate cut bets.

Disappointing ISM/Services PMI, indicating slowing economic momentum.

A dovish Powell speech, hinting at faster rate cuts, weakening USD.

A widening trade deficit, signaling weaker net exports, which may drag USD lower.