Above: Trump and Commerce Secretary Howard Lutnick in the White House. Official White House press image.

It will all depend on whether or not the Dollar rekindles its love for tariffs.

The Dollar has found itself better supported through the latter half of March but could be on course to resume the selloff in April.

The new month commences with a barrage of tariff announcements from U.S. President Donald Trump that some major investment bank analysts think could boost the Dollar.

"We maintain our forecasts for a USD rebound in Q2," says Daniel Tobon, a currency analyst at Citi. "Tariff risks look underpriced and we expect USD undervaluation to correct on a hawkish April 2 announcement."

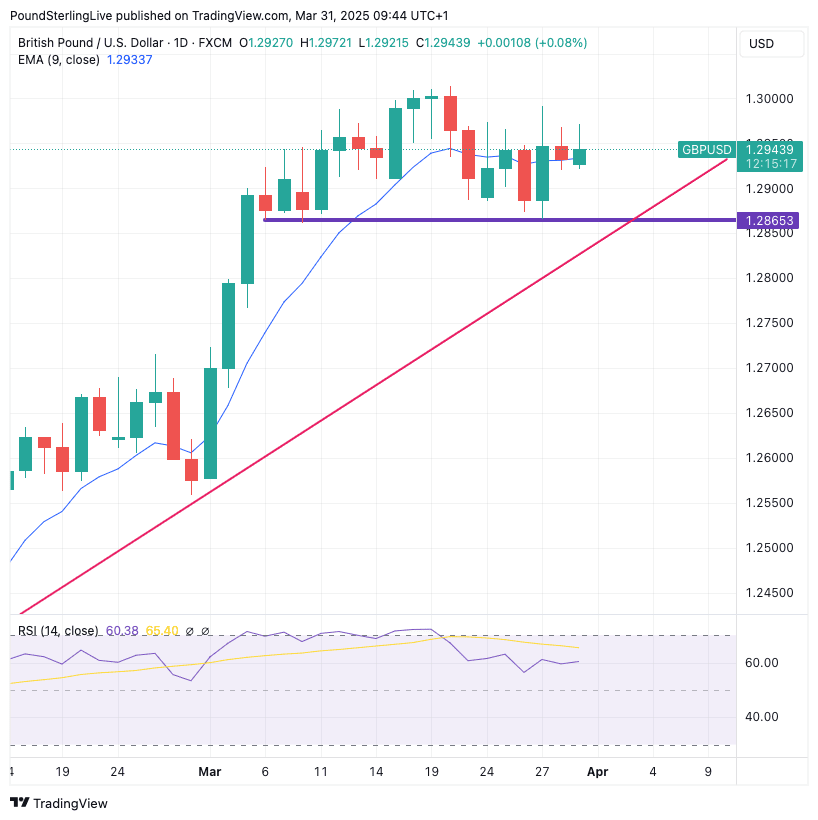

The expectation of a Q2 rebound would mean the Pound-to-Dollar exchange rate's recent high of 1.30 won't be threatened again, and a retreat to 1.25 evolves over the coming weeks.

However, this assumption will be severely challenged if the Dollar maintains recent trends that confirm it to be one of the most at-risk currencies to tariff headlines in the G10.

Why 1.30 is in Play this Week

There was a universal expectation heading into the year that the Dollar would outperform in the first half of the year as Trump's tariffs rolled out, putting pressure on the global economy and encouraging safe-haven demand for the Greenback.

However, the Dollar has struggled in 2025 as U.S. President Donald Trump's tariff agenda has proved less than helpful for the U.S. economy.

The reality is that the DOGE programme and other policy decisions from the White House are sapping U.S. economic exceptionalism and letting the air out of an inflated U.S. equity bubble, and playing negative for USD.

We are now at a fork in the road: do tariffs start to play positive for USD again, or will 2025's playbook be followed?

If 2025's template stays in place, then severe tariff announcements could well see Pound-Dollar test and break the 1.30 level in the coming days.

"GBP/USD price action continues to look solid, holding within the consolidation range things have sat in since the early March (upward) break. That keeps the 1.3044 line in play, above which a push to the 1.3108/42 band would be the goal," says Nick Kennedy, FX analyst at Lloyds Bank.

A Dollar Strength Scenario

Bear in mind that the selloff in global stocks we are witnessing on Monday looks to be a positioning adjustment ahead of Wednesday. This would imply negatives are being well priced ahead of the decision itself.

This opens the door to a classic "sell the rumour, buy the fact" reaction that would bolster the USD in the event of a U.S. equity market recovery as investors reckon we are reaching the limits of negative U.S. tariff headlines.

Pound-to-Dollar Forecasts Upgraded at Goldman Sachs, Crédit Agricole

There is also a scenario in which the Dollar rallies on severe headlines whereby investors wake up to the risks for the global economy posed by the escalating trade war.

"We see some upside potential for the dollar this week as markets may have turned a bit too sanguine on the tariff view, and Trump has suggested over the weekend that he will impose tariffs on all countries," says Francesco Pesole, FX Strategist at ING Bank.

"We think the risks are skewed towards a stronger dollar and yen and weaker European currencies alongside the Australian and New Zealand dollars," he adds.

If this view is correct, then Pound-Dollar would be on track to test 1.2865 by the weekend, ahead of a potential break.

For now the uptrend remains intact, but should the market dip below the red line annotated on the chart, then a more enduring setback in Q2 becomes visible.

A Busy Calendar

Don't lose sight of the U.S. economic calendar, as we will likely get some clear indications as to how the economy is holding up under Elon Musk's DOGE cuts and volatile policy making.

Surveys show a sharp deterioration in sentiment is underway, and we will be interested in seeing if this is impacting other data.

If yes, then the prospect of a USD slump and GBP/USD push to 1.30 and above becomes a real prospect.

In fact, some analysts reckon the data will be of greater importance to the Dollar than the tariff news.

Tuesday, April 1

? ISM Manufacturing PMI (Mar)

Expected: 49.8

Previous: 50.3

? USD Sensitivity:

A reading below 50 indicates contraction.

Stronger-than-expected data would support USD, signalling ongoing resilience in the manufacturing sector.

A drop could raise concerns about economic momentum, mildly negative for USD.

? JOLTS Job Openings (Feb)

Expected: 7.69 million

Previous: 7.74 million

? USD Sensitivity:

If job openings remain high, this would indicate tight labour conditions, potentially delaying Fed rate cuts and supporting USD.

A sharp drop could imply cooling demand for labour, possibly weakening USD.

Wednesday, April 2

? ADP Employment Change (Mar)

Expected: +119K

Previous: +140K

? USD Sensitivity:

A strong print reinforces confidence ahead of NFP, supporting USD.

A significant miss may trigger caution, potentially softening USD ahead of Friday's payrolls.

? Factory Orders (Feb)

Expected: +0.4%

Previous: +1.7%

? USD Sensitivity:

Resilient orders = strong investment demand = USD positive.

A weak result may reinforce concerns of slowing business activity.

Thursday, April 3

? Initial Jobless Claims (Week ending Mar 29)

Expected: 225K

Previous: 224K

? USD Sensitivity:

Stable or lower claims = tight labour market, reinforcing Fed caution on rate cuts → USD support.

Higher claims = softening jobs market → mild USD weakness.

? Trade Balance (Feb)

Expected: -$110.0 billion

Previous: -$131.4 billion

? USD Sensitivity:

A narrower deficit supports GDP tracking, potentially positive for USD.

A wider gap may imply slower net exports, modestly negative for USD.

? ISM Services PMI (Mar)

Expected: 53.1

Previous: 53.5

? USD Sensitivity:

As services dominate U.S. GDP, this is a key growth gauge.

A reading well above 50 supports economic optimism → USD bullish.

A surprise dip could signal demand softening, weighing on USD.

Friday, April 4

? Non-Farm Payrolls (Mar)

Expected: +135K

Previous: +151K

? USD Sensitivity:

A strong NFP print would reinforce Fed’s cautious stance, delaying rate cuts → USD strength.

A weak report could signal labour market cooling, increasing rate cut bets → USD negative.

? Average Hourly Earnings (Mar)

Expected: +0.3% MoM (3.9% YoY)

Previous: +0.3% MoM (4.0% YoY)

? USD Sensitivity:

Sticky wage inflation supports a hawkish Fed outlook, supportive for USD.

Cooling earnings growth may ease inflation concerns, weighing on USD.

? Unemployment Rate (Mar)

Expected: 4.1% (unchanged)

? USD Sensitivity:

Stable = neutral to mildly positive.

Surprise rise may raise concerns about labour market deterioration.

? Fed Chair Powell Speech (11:25 AM EST)

? USD Sensitivity:

Markets will look for cues on policy direction.

Hawkish tone (e.g. "too early to cut") → USD support.

Dovish tone → increases expectations of rate cuts → USD weakness.