Image © Adobe Images

The US Dollar fell broadly alongside local stock and bond markets last week as some public and private investors were said to have taken flight, perhaps as if they were Israelites fleeing from the great house of Pharaoh.

On Friday, and the eve of Passover, there were numerous reports from market participants and other market professionals of an exodus from US Dollar assets, by private and public investors who might have at least resembled the earliest Israelites in their flight from Egypt and the house of Pharaoh.

“The end of US hegemony trade is in full force as the Trussification of the dollar continues. Those who are old enough to remember Liz Truss remember that her policy mix was poorly received by the markets,” says Brent Donnelly, CEO at Spectra Markets, a veteran FX trader and Canadian national.

“Now, the embargo on Chinese trade, RNG tariffs that change daily, long time allies stabbed in the back all at once, and a concomitant collapse in business, investor, and consumer confidence have triggered a flight out of US assets. In soccer, this is called an ‘own goal,’” he adds.

Donnelly says this has “the makings of another great USD down move like the one from 2002 to 2008,” in which an eight-year bubble in US equities, and a 50% rally by the US Dollar Index were unwound over the course of three years, and is now watching Magnificent 7 stocks especially closely.

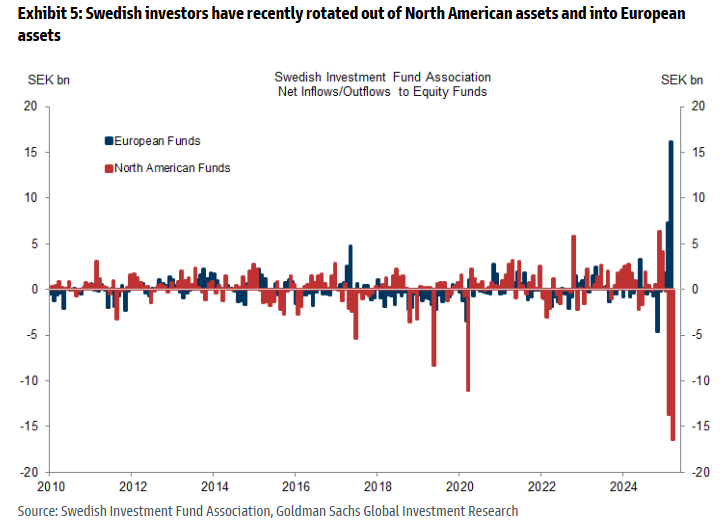

Above: Equity investment flows of Swedish institutional investors. Source: Goldman Sachs.

“If someone threatens to burn down my house, and then in the interest of self-preservation, I make a deal with them not to burn it down, I’m not going to trust that my family is safe,” Donnelly says.

“In other words, the global investors, wealth funds, and pension money selling US assets are not coming back. When these Canadian or European pension funds are done selling their US overweights, they are never buying them back again, at least until 2028 or later,” he adds.

Others noting the flight from US assets included commentators at Deutsche Bank and Berenberg, with each questining the US Dollar’s position as the main global reserve currency.

“Despite President Trump's reversal on tariffs the damage to the USD has been done: the market is re-assessing the structural attractiveness of the dollar as the world's global reserve currency and is undergoing a process of rapid de-dollarization. Nowhere is this more evident than the continued and combined collapse in the currency and US bond market,” says George Saravelos, of Deutsche Bank.

“Given the centrality of the dollar to the global financial system there are likely to be many unpredictable consequences to the epochal shifts in capital flow allocation that have been unleashed. We think the process of de-dollarization has more to go, but we are keeping a very open mind as to how this process plays out and what the ultimate new equilibrium in the global financial architecture will be,” he adds.

Meanwhile, peers at Berenberg said the Dollar now looks less like a safe-haven, among other things.

Above: US Dollar Index at daily intervals with S&P 500 index, US 10-year and 30-year Treasury yields. Click for closer inspection.

“The initial US Treasury sell-off may have been triggered by technical factors and – perhaps – even the Chinese government; however, long-term fundamentals also point to higher US government bond yields and a lower dollar, in our view,” says Holger Schmeiding, chief economist at Berenberg, in a Friday note.

“Policies that gamble with a country’s public finances and/or its growth outlook can cause bond investors to question the assumption that government debt is risk free. The breakdown in the relationship between US Treasury yields and the dollar highlights the concerns of investors about Donald Trump’s policy agenda. We have long argued that the fiscal position of the US is unsustainable,” he adds.

The possible role of “the Chinese government,” in the Treasury sell-off is a highly salient point, however, given the intense pressure on the trade-weighted Renminbi in recent weeks, its quasi peg with the trade-weighted US Dollar, and the numerous apparent FX interventions undertaken last week in support of the currency.

Beijing’s basket-based approach to its managed-floating exchange rate does create a positive correlation with, if not quasi peg to, the US Dollar so it’s possible that both currencies’ losses have been mutually reinforcing.

However, peers at UBS said, “demand for reserve currencies will slow (and may even fall in absolute terms),” because trade is likely to fall as a share of global GDP due to changes in US tariff policies, but that “the dollar is not going to be replaced, and it is very unlikely that any single alternative will emerge,” and that the “parallel is perhaps to the declining importance of sterling in the 1930s with several other currencies playing a larger role, rather than the replacement of sterling.”

Above: US Dollar Index at monthly intervals with Fibonacci retracements of 2014 and 2021 uptrends highlighting possible areas of technical support. Click for closer inspection.