Image © Adobe Images

The British Pound is in an uptrend against the Dollar and most signs point to continuation.

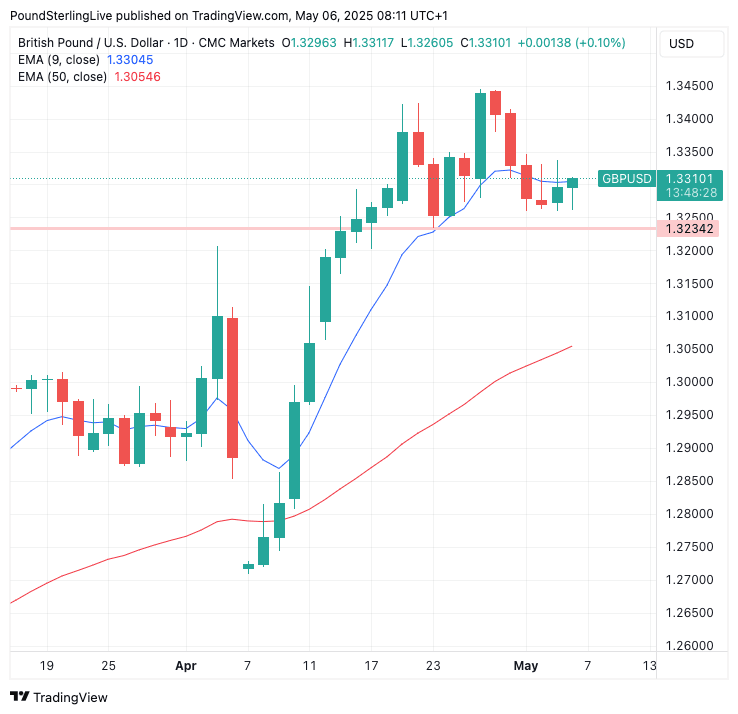

The Pound to Dollar exchange rate (GBP/USD) peaked at 1.3441 early last week. Since then, it has pared the advance as consolidation sets in, although weakness has failed to extend beyond support at 1.3234.

The ability to hold above this level confirms that the exchange rate remains in an uptrend, with dips being shallow and providing a platform for launches into new multi-month highs.

We think another leg higher is on the cards, with the move likely to extend beyond 1.3440, but this week might be too early for the next phase of the rally and further consolidation around the nine-day exponential moving average (EMA) is possible.

The nine-day EMA is located at 1.33 at the time of writing and has been in touch with the exchange rate for the past three trading sessions, and it could continue to act like a magnet in the coming hours and couple of days.

Sideways action is possible as markets await fresh impetus on trade talks between China and U.S., which were hinted at last week and would mark a further easing in concerns about global trade.

Above: GBP/USD at daily intervals.

We also await fresh data from the U.S. to indicate whether Trump's tariffs are having a real impact on the domestic economy. Last week's U.S. jobs report for April showed no immediate concerns, which offered investors some relief.

However, we found it curious that the Dollar failed to rally following the strong reading, which is in itself a signal that the currency really is lacking conviction.

As such, Pound-Dollar weakness will likely prove shallow and potentially restricted to horizontal visual support at 1.3234.

"Even after a swift move in recent weeks, we believe that the Dollar has further to fall. Less exceptional US asset returns will compress the Dollar's high valuation as global allocators move to a more diversified portfolio," says Kamakshya Trivedi, head of FX analysis at Goldman Sachs.

There are no significant data releases or events due from the U.S. this week, although U.S. President Donald Trump will surely keep us on our toes with his off-the-cuff proclamations that can tend to move the market.

The Federal Reserve's midweek decision should be the marquee event of the week, but the Fed will stay on hold and give very little away in terms of guidance, as it too awaits evidence of how tariffs and associated uncertainty is hitting the economy.

It really will be a placeholder meeting that offers financial markets limited signals.

China's commentary regarding the potential for trade talks will also be closely watched. However, the bottom line remains that a significant tariff barrier will remain place for the coming years, which is something that is likely to be a negative for the Dollar.

The UK will be of interest, with the Bank of England likely to inject some volatility into Pound Sterling.

The Bank will likely cut interest rates and signal the potential for a follow-up move in June, putting the Pound under pressure as it seeks to increase the amount of support it offers the economy.

The Pound has been conditioned to expect interest rate cuts on a quarterly basis, meaning a follow-up cut in June would break this assumption as it accelerates the pace.

Under such a scenario, there are elevated risks that the Pound-Dollar conversion will break below the 1.3234 interim support level and move to 1.32 and even below.

The Bank will potentially move to a faster pace of interest rate cuts owing to the slowdown in the economy signalled by incoming survey data. (The Bank's Monetary Policy Committee has traditionally tended to err on the side of caution by cutting interest rates on evidence of a slowing economy.)

A rise in employer National Insurance Contributions and the mandatory hike to the minimum wage, two hallmarks of Chancellor Rachel Reeves' fiscal policy, pushed the UK economy into contraction in April, according to the S&P PMI survey.

![]()

Image © Pound Sterling Live

The Lloyds Business Barometer reported a 10 percentage point drop in business confidence between March and April to a three-month low of 39%. This marks the biggest drop since June 2022, with both the economic optimism and trading prospects subcomponents registering a decrease.

Falling international gas prices, meanwhile, point to easing inflationary pressures on the horizon.

"What is perhaps more significant for a UK economy highly (negatively) geared to the gas price is the 2025 natural gas curve is now 20% lower than the level conditioned for the last inflation forecast back in February. This, lower oil prices, and a stronger GBPUSD all tee up a considerably more dovish Monetary Policy Report," says Simon French, Chief Economist & Head of Research at Panmure Liberum.

A 'dovish' report would weigh on the Pound.

However, given the prevalence of building inflationary pressures, the Bank will still be relatively contained in its ambitions and would surely need to signal some caution. In fact, there are risks that inflation forecasts are raised in the Monetary Policy Report, which will detail the Bank's latest economic projections.

This would put limits on the Pound's downside and help GBP/USD recover ahead of the weekend.

Indeed, the Bank is unlikely to trouble the exchange rate's uptrend, which is ultimately underpinned by the USD side of the equation, where more weakness can be expected.