Image © Adobe Images

Pound Sterling starts the new week with a solid advance against the Dollar, although a busy U.S. data calendar and the UK's elections could offer up some volatility.

The Pound to Dollar exchange rate is sitting on a daily gain of 0.30% (1.2678) at the time of writing. The Pound has been boosted by a rally in European assets as investors expressed relief that Marine Le Pen's National Rally party is less likely to secure an absolute majority in the National Assembly following the weekend election.

This after her party underperformed relative (~33% of the vote) to what the polls were suggesting it would achieve (~36%).

A hung legislature is the odds-on outcome of Sunday's second round of voting, particularly given the far-left and centrist parties are willing to collaborate in an anti-Le Pen voting strategy.

The net result is that European assets are on the rise, including the Pound.

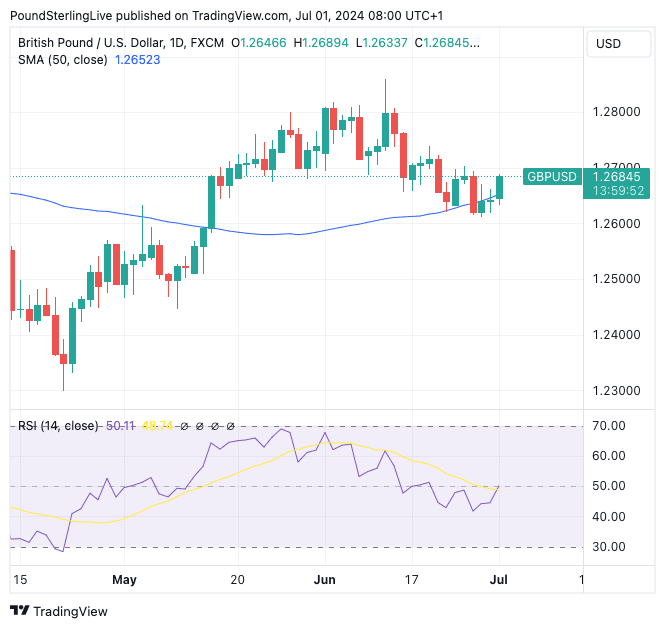

Pound-Dollar has moved above the 9-day moving average, the first real positive technical development we have seen for the pair since mid-June. It could signal some near-term follow-through gains are possible, with 1.27 being a potential target. The RSI is at 50 (neutral), but it has turned higher again (positive development for the coming hours).

We note that the pair has also broken above the 50-day moving average which had turned into a source of resistance last week. A daily close above this level (1.2654) could signal a more constructive technical outlook is building again. A rise in the Pound would put it on course for the median point forecasted by the world's major investment banks.

Above: GBP/USD at daily intervals, 50-day MA in top panel, RSI in lower panel. Track GBP/USD with your own alerts, find out more here.

Looking at the calendar, numerous releases and speeches in the coming week can offer Pound-Dollar volatility.

The U.S. ISM manufacturing survey will be released on Monday, potentially offering further signs of an economic slowdown.

Federal Reserve Chair Jerome Powell will speak at the ECB's central bank conference in Sintra, Portugal, on Tuesday. Markets will be interested to hear his updated views on the possibility of a 2024 Fed rate cut.

This theme continues through midweek when the Fed releases the minutes for its June 11-12 policy meeting. This should offer up some more colour to markets on the all-important question of interest rates. Wednesday also sees the ISM PMI survey for the services sector, another potential market-moving release.

As a reminder, should the market raise expectations for a September rate cut following these data and appearances, then the Dollar can fall. Any disappointments will boost the Dollar. The market is currently pricing in a 56% chance of a September rate cut.

The week's highlight will be Friday's non-farm jobs report. A headline figure of 180K is expected, down from 272K. Average hourly earnings are expected to print at 0.3% month-on-month in June.

The UK election on Thursday is a low-risk event at this stage as the odds of a Labour victory are set very high and we have not seen any shift in the polling to suggest this won't be the outcome.

The first key event to watch is the exit poll due at 10PM on Thursday night. This has been a very accurate indicator in recent history.

The surprise would be a stronger showing by the Conservatives that results in a 'hung parliament' where no single party is able to command a majority on its own.

This would result in a softer Pound as markets contemplate a period of uncertainty. We would expect volatility to be shortlived as there is nothing radical in the spending and tax plans of Labour, the Conservatives or Liberal Democrats.