- USD rises on improved mood music

- As U.S. PMIs prove robust

- But 'sell America' hasn't disappeared

- This will keep USD trending down

Image © Adobe Images

The U.S. economy is doing well, to the relief of the Dollar.

Dollars were bought after an economic survey for May confirmed the economy continued to hum along nicely.

The U.S. gave a "punchy" account of itself as the Composite PMI rose to 52.1 from 50.6 in April, surpassing a consensus expectation for 50.3.

The composite PMI measures activity in the U.S. private sector and is considered a decent benchmark for official economic data outturns, with a reading above 50 representing expansion.

"Punchy U.S. PMI overrules fiscal fears," is the headline takeaway from Harun Thilak, Head of Global Capital Markets at Validus Risk Management.

The PMI survey has three main components, and all came in above the expectation line:

- Composite PMI: 52.1, expected: 50.3, previous: 50.6

- Manufacturing PMI: 52.3, expected: 50.1, previous: 50.2

- Services PMI: 52.3, expected: 50.8, previous: 50.8

"All signs point to a robust U.S. economy," says Thilak.

Subcomponents showed employment that was consistent with ongoing resilience in the labour market and becalmed inflationary pressures. With no nasty inflationary surprises, the market is betting the Federal Reserve will be able to cut interest rates in the coming months.

"We remain optimistic that restrained underlying services inflation will provide the Fed with breathing room to ease policy by 75bp later this year," says Oliver Allen, Senior U.S. Economist at Pantheon Macroeconomics.

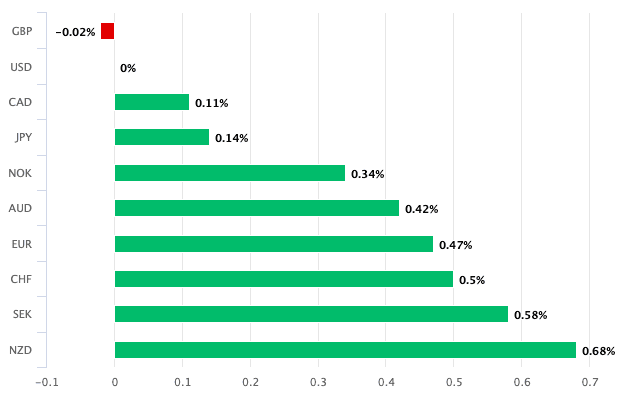

The Dollar seems to have let go of any correlation with Fed interest rate expectations, instead it is simply responding positively to the improved mood music regarding the outlook.

It rose across the board, with only a small daily loss being registered against a resurgent British Pound:

For its part, the Pound to Dollar exchange rate hovers near multi-month highs at 1.3468, as Pound Sterling also looks to have lifted its chin following a bruising week.

These data come at the end of a difficult week for the Dollar as investors turned attention to the USA's rising debt pile and rising bond yields, and fretted that the U.S. was losing its lustre as the go-to global investment destination.

"The recent headlines around proposed tax cuts and a deteriorating US fiscal balance have led to a weakening in USD and rise in US yields. However, today’s stronger U.S. data has provided some relief, easing the recent pressure on these asset classes," says Thilak.

The U.S. House of Representatives narrowly passed President Donald Trump's expansive "One Big Beautiful Bill" early Thursday morning, marking a significant legislative victory for the administration, but one that saddles the country with more debt.

The federal debt held by the public currently stands at around 100%, its highest since the Second World War, and it is set to rise to 117% in ten years, even with current law.

The bill pushes the 2034 debt-to-GDP ratio to 125% as written, and 129% if the plans are made permanent.

The concern for markets is that at some point, foreign demand for this debt doesn't meet supply, creating financial and fiscal risks.

The spotlight on debt comes after U.S. investors had to negotiate frantic tariff developments and Trump's attacks on the Federal Reserve.

"We expect President Trump’s erratic policymaking is set to increase the number of 'Sell America' days," says Mansoor Mohi-uddin, Chief Economist at the Bank of Singapore. "That keeps us cautious on long-term Treasuries and the U.S. dollar."

“We think the greenback will weaken further over the next 12 months to 1.23 against the euro as investors reassess their U.S. exposures,” he adds.