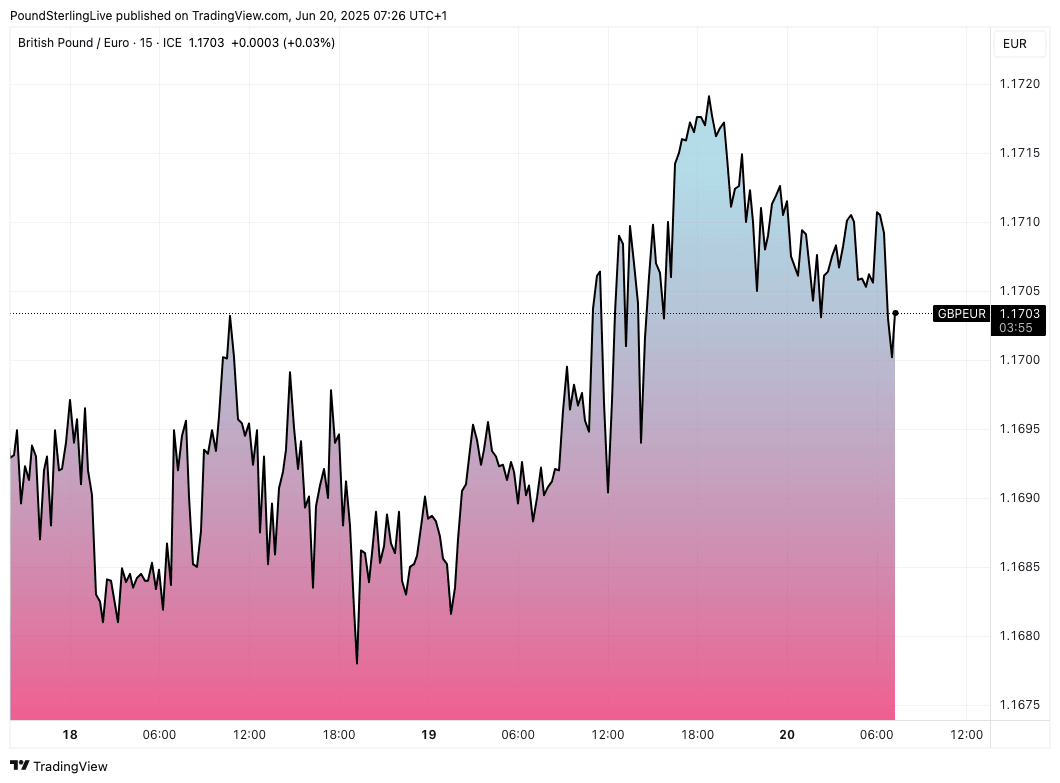

- GBP/EUR retreats to 1.17

- Retail sales slump in May

- But, consumer confidence rises in June

- Bank of England repricing no longer a headwind

- Middle East tensions subside, somewhat

Image © Adobe Images

Retail sales fell notably in May, but Pound Sterling is finding some support from easing Middle East tensions.

The Pound to Euro exchange rate saw some selling pressures after the ONS said retail sales fell 2.7% month-on-month in May from +1.3% in April, and below consensus expectations for -0.5%.

On a year-on-year basis, retail sales slumped to -1.3% from 5%, undershooting estimates for +1.7%.

There was always going to be some give-back following April's weather-related stellar figures, but of concern is that sales volumes fell across all sectors, according to the ONS.

The Pound to Euro exchange rate was at 1.1710 ahead of the release but dropped to 1.1690 in the minutes following the retail sales announcement, confirming financial markets were paying attention.

However, downside will be limited as the retail sales data follows the release of the GfK consumers’ confidence survey, which showed consumer confidence rose to a six-month high of -18 in June, up from -20 in May.

This suggests consumer confidence can sustain retail sales in the coming weeks and that maybe the disappointing May figures are a blip.

"We think the economic fundamentals of real wage gains, steady economic growth, and a strong labour market will place a secure floor under consumers’ confidence in H2," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.

Given this, the selloff in GBP/EUR is unlikely to be significant, and raises the likelihood of further consolidation at 1.17.

Above: GBP/EUR at daily intervals.

Pound Sterling rose from recent lows against most major currencies following the Bank of England's decision to keep interest rates unchanged at 4.25%, while indicating that an August rate cut is likely.

Given that the market was virtually fully geared up for this outcome, there were no surprises for the Pound, and markets adopted a sell-the-rumour / buy-the-fact attitude to the UK currency.

The Pound was heavily sold against the Euro over the past ten days, as markets adjusted from seeing no August cut to fully pricing one in. This repricing followed a string of soft data prints, chief amongst them a weak labour market report.

With the Bank indicating an August rate cut is indeed on, the market's 'dovish' repositioning will stall for now, giving the Pound a break.

Trump Pulls Back

Official White House Photo by Daniel Torok.

GBP/EUR is also taking cues from headlines concerning the Iran-Israel conflict, with an apparent easing in tensions offering some temporary support for the exchange rate.

White House spokeswoman Karoline Leavitt said late on Thursday that President Donald Trump will decide within two weeks whether to strike Iran.

“Based on the fact that there’s a substantial chance of negotiations that may or may not take place with Iran in the near future, I will make my decision whether or not to go within the next two weeks,” Trump said in a message conveyed to the press by Leavitt.

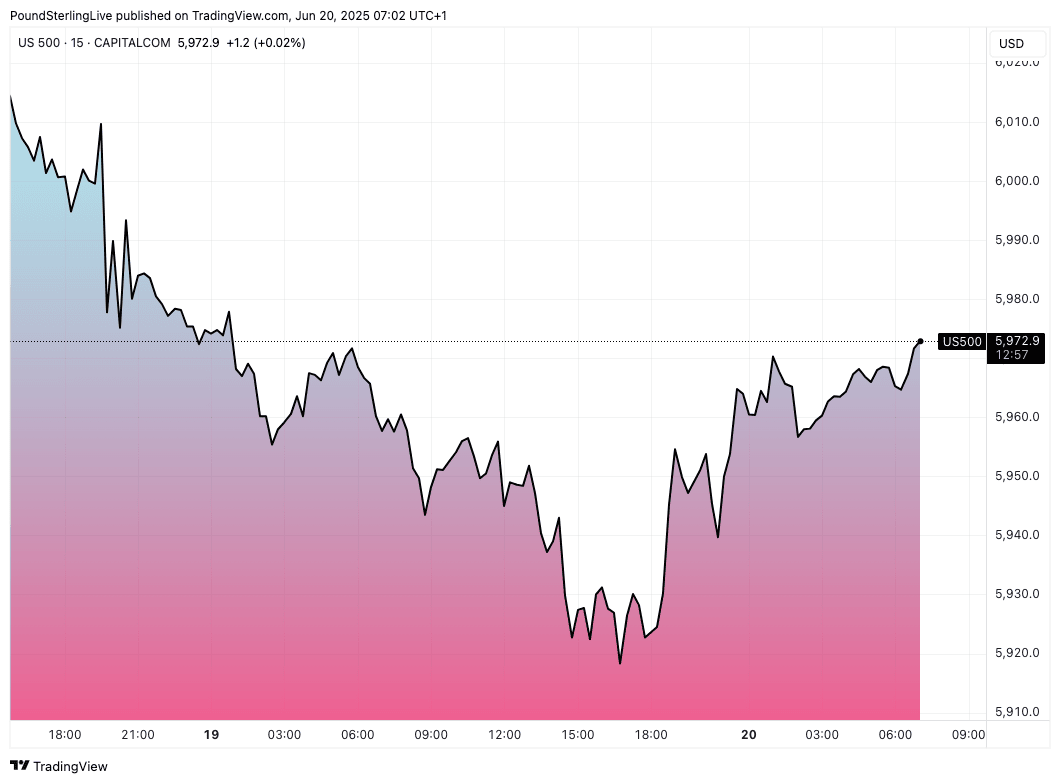

Above: The U.S. S&P 500 is off the recent lows. The recovery speaks of improving risk sentiment.

The prospect of an extended deadline to any military action contrasts with reports earlier on Thursday that suggested they might be imminent.

Mention of negotiations also clearly signposts a diplomatic solution to the Iranian nuclear issue.

Oil prices are lower as a result, which is helping equity markets extend a recovery. For risk-sensitive currency pairs like GBP/EUR, this can offer some support.

"Fears of an immediate US strike on Iran have receded, but the redeployment of military assets continues, indicative of preparations for U.S. forces to join Israel’s campaign," says Chris Beauchamp, Chief Market Analyst at IG.

"So long as the conflict remains contained, then we can expect market reaction to remain similarly muted; how much U.S. participation is now priced in given Trump’s rather transparent comments on the subject remains to be seen,” he adds.