Image © Adobe Images

Pound Sterling is forecast to remain under pressure against the Euro.

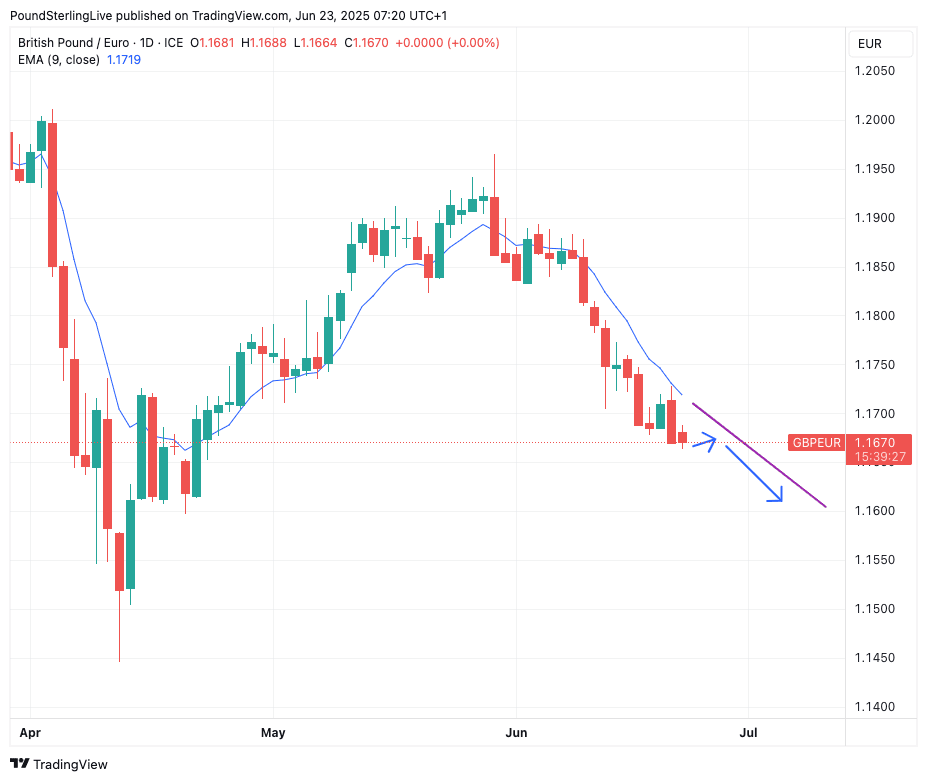

The Pound to Euro exchange rate (GBP/EUR) has fallen for four consecutive weeks, and our Week Ahead Forecast model says not to stand in the way of this short-term trend.

The pair reached 1.19 in late May, but this was a peak and losses have since ensued, taking it to a low of 1.1664 on Monday morning.

Weakness comes amidst rising volatility in global markets owing to an escalation in the conflict between the U.S. and Israel, which culminated with a weekend attack by the U.S. on Iran's nuclear weapons sites. Fears that Iran will shut the key shipping lane in the Strait of Hormuz are keeping markets on edge, and we think this will weigh on Sterling more broadly.

However, GBP/EUR weakness also has domestic economic concerns to blame, with rising unemployment and elevated inflation pointing to the potential for the UK economy to fall into stagflation.

The exchange rate has fallen below the nine-day exponential moving average (EMA), which is pointing lower and looks set to guide GBP/EUR to below 1.16 in the next two to three weeks.

In the near term, there is scope for brief recovery attempts that would allow GBP/EUR to reconvene with the nine-day EMA, which would be expected as the exchange rate does tend to mean-revert towards the trend line.

However, these kinds of intra-day gains won't be substantial and will likely be sold into by traders looking to push GBP/EUR to an ultimate target at 1.1446, which is the April 11 low.

Above: GBP/EUR at daily intervals, showing the near-term downtrend.

Action in the week ahead will be primarily guided by events in the Middle East, with an escalation likely to weigh on GBP/EUR.

However, there are some calendar events in both the Eurozone and UK that are worth watching.

The new week starts with some good news out of Germany, with the composite PMI - a measure of private sector business activity - expanding in June. The PMI read at 50.4, up from May's 48.5, which beats expectations for another sub-50 reading of 49.

The Eurozone PMI also registered an expansionary 50.2, which is unchanged from June's reading.

These data point to the economy humming along through the mid-point of the year, defying President Trump's tariffs and giving credibility to expectations that the European Central Bank (ECB) can now pause its rate-cutting cycle, a development that would be bullish for the Euro.

?? United Kingdom

? Monday, 23 June

S&P Global UK PMIs (June, preliminary) at 09:30 BST:

Composite PMI: Watch for movement around 53.0 level.

Services PMI (prior: 50.9): Expected to rise to 51.3.

Manufacturing PMI: Directional surprises could sway sentiment.

? Key Sensitivities: Watch employment and business costs, recent releases have flagged dovish risks.

? Tuesday, 24 June

Bank of England Speakers:

Greene at 10:30 BST

Ramsden at 14:35 BST

Bailey (Governor) at House of Lords hearing at 15:00 BST

Breeden at 16:50 BST

? Market Implication: No major policy shift expected, but tone on inflation and growth will be monitored. Markets still lean toward an August rate cut.

? Wednesday & Thursday, 25–26 June

BoE Lombardelli speaks Wednesday at 09:45 BST

BoE Breeden and Bailey speak again on Thursday (09:30 and 12:00 BST respectively)

? Tone Watch: Commentary follows last week's decision to hold interest rates unchanged, although the odds of an August rate cut are elevated. Commentary is likely to reinforce this expectation, which will contribute to the Pound's soft underbelly.

?? GBP Summary:

Event Date Expectation / Impact

UK PMIs (Jun P), Mon 23 Jun: Services seen improving slightly; details on hiring/costs crucial

BoE Speakers, 24–26 Jun: Close watch on rate cut timing clues; August cut still priced

Market Implication: Dovish tone or soft PMIs = GBP bearish; upbeat tone = GBP support

?? Eurozone

? Tuesday, 24 June

Germany IFO Survey (June) at 09:00 BST

Focus on business climate, current assessment, and expectations

Historically a more accurate sentiment gauge than ZEW

ECB’s Lane Speaks in London at 14:55 and again at 15:15 BST

? Watch: Any dovish signal could push EUR lower.

? Thursday & Friday, 26–27 June

Germany GfK Consumer Confidence (July) – Thursday at 07:00 BST

Forecast: -19.2 (still in negative territory)

Preliminary CPI:

France (07:45 BST) and Spain (08:00 BST) – Friday

Expectation: Slight acceleration in MoM inflation; YoY trends still gently easing

Eurozone Economic Confidence (10:00 BST) – Friday

Italy PPI (11:00 BST) – Friday

?? EUR Summary:

Eurozone PMIs (Jun P), Mon 23 Jun: Services >50, Mfg recovering; upside = EUR support

Germany IFO Survey, Tue 24 Jun: Stable outlook expected; surprises more impactful than ZEW

France & Spain CPIs (Jun P), Fri 27 Jun: Seasonal MoM uptick; underlying core inflation still gently declining

Eurozone Confidence Surveys, Fri 27 Jun: Any decline could reinforce dovish ECB bias

ECB Speakers (Nagel, Lane), 23–24 Jun: Hawkish = EUR ↑; Dovish = EUR ↓