Image © Adobe Images

Given the fundamentals, it is hard to see any enduring strength, leaving 1.14 more achievable than 1.20.

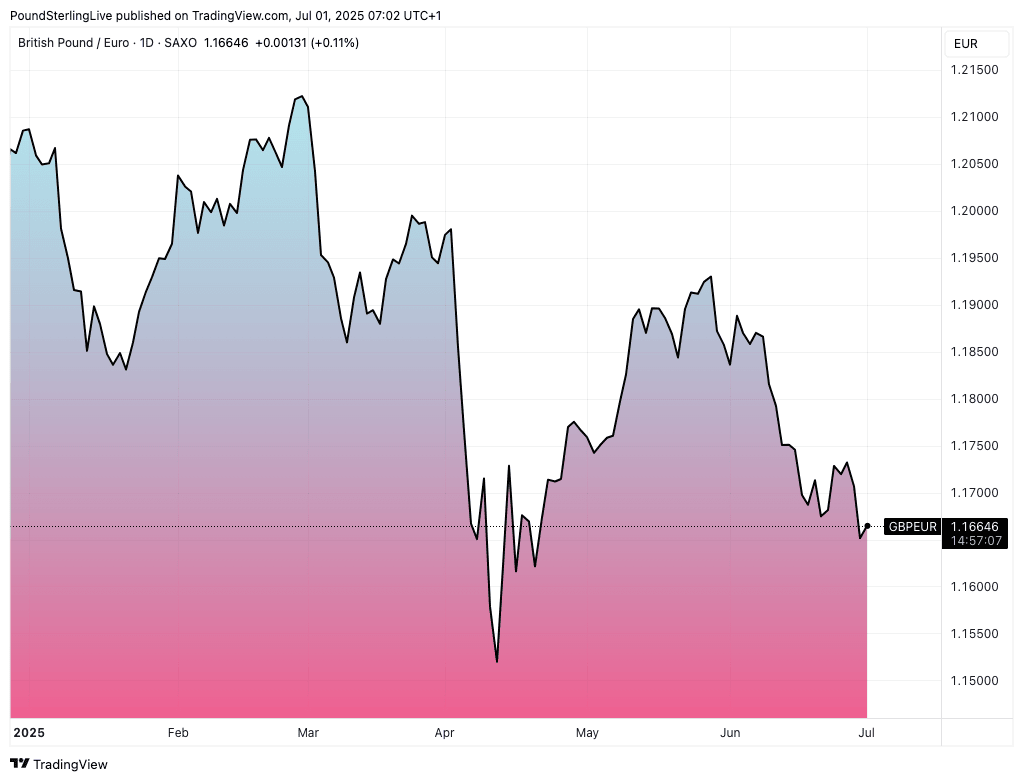

The Pound to Euro exchange rate starts July with a daily gain of a third of a per cent, reaching 1.1682 at the time of writing, having closed the previous month at 1.1650.

The advance is a partial paring of recent losses and isn't driven by any news or events, meaning it is more a technical development than anything fundamental.

There is scope for a further rise in the coming days, and June could even be a positive month for the exchange rate, particularly if the current equity rally extends.

The Pound-Euro tends to gain when markets are in a constructive mood, and fall when volatility is on the rise, as is currently the case.

However, the second half of the year will be a challenging one for Britain's currency as economic challenges press the Bank of England into further rate cuts and a deteriorating fiscal outlook prompts the government to raise taxes again.

These issues are already weighing on Sterling, which fell 3.5% against the Euro in the first half of 2025, with June witnessing the biggest single monthly decline of 1.70%.

The June decline reflected a poor month for UK economic news, with employment, GDP and inflation releases all undershooting expectations and raising the odds of an interest rate cut at the Bank of England in August.

Above: GBP/EUR on a daily timeframe, showing action in 2025.

In fact, because the trajectory of the UK economy is looking increasingly challenged, economists at Goldman Sachs say the Bank could even start cutting interest rates on a meeting-by-meeting basis, whereas the preferred approach of the past year has been to cut on a quarter-by-quarter basis.

Although the economy started the year on a strong footing, growing 0.7% year-on-year in Q1, GDP looks to have decelerated sharply in the second quarter, with June's GDP release showing a -0.3% month-on-month slump in April.

Just as the market gets used to the idea of more Bank of England cuts, it sees that the European Central Bank (ECB) is nearing the end of its cutting cycle, anticipating it to keep rates on hold in July and lower rates for the last time in the cycle in September.

"We expect price pressures to subside in the euro area as a whole and see some downside risk compared to consensus, but this is most likely not enough to prompt the ECB to cut interest rates again in July," says Amanda Sundström, an economist at SEB.

Recent communications support SEB's view that the ECB wants to await more information, especially on tariff and trade developments. "We believe the next cut will come in September, when the ECB also publishes updated macro forecasts," says Sundström.

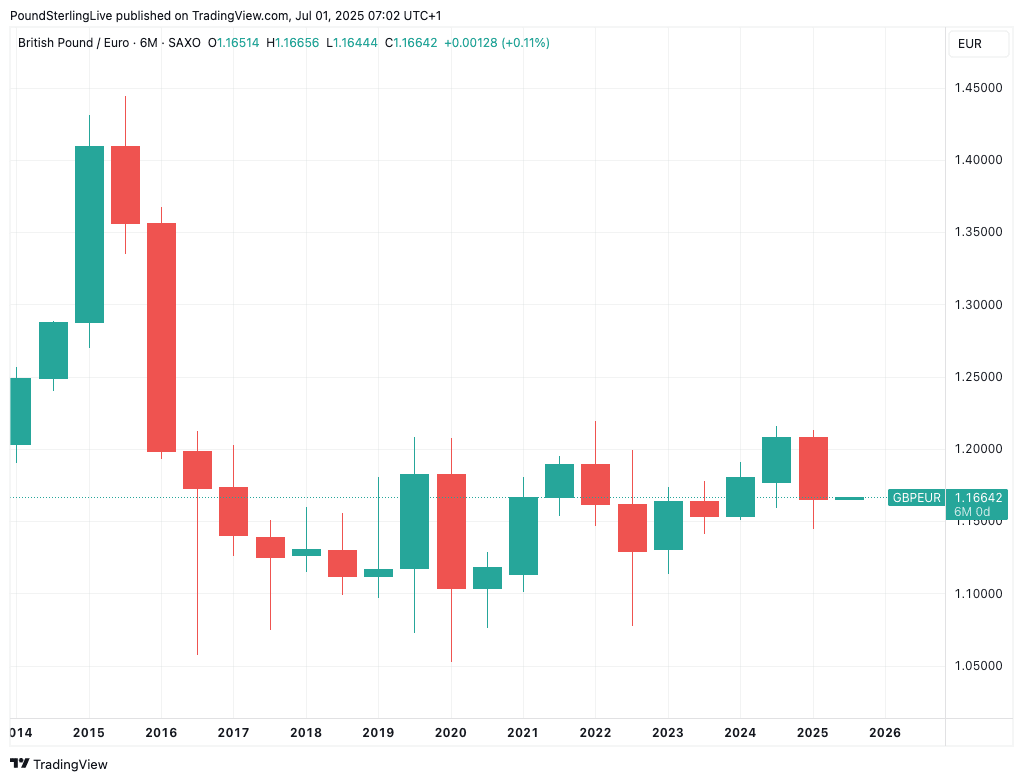

Above: Bigger picture, GBP/EUR hasn't recovered from the Brexit shock, whereas some other GBP pairs have.

The outlook for the second half is one that has a potentially significant divergence in central bank monetary policy, with interest rates falling faster in the UK than in the Eurozone, lessening the appeal of UK bonds, and creating ongoing selling pressure on the Pound.

Domestically generated downside risks for Sterling in the second half of the year will coincide with the love-in between international investors and Europe, now that the U.S. is looking less appealing under Donald Trump's leadership.

"In FX, the greenback’s steady decline looks set to continue, as the idea of 'U.S. exceptionalism' continues to wane," says Michael Brown, Senior Research Strategist at Pepperstone. "The EUR, in the G10 world, looks likely to benefit most here."

"European outperformance should continue," he adds.

This all leaves the Pound-Euro vulnerable to further losses over the remainder of the year. We could still see some 'up months' for the exchange rate as it corrects previous selloffs, but given the fundamentals, it is hard to see any enduring strength, leaving 1.14 more achievable than 1.20.

However, the Pound continues its ascent against the U.S. Dollar, rising nearly 10% in the first half of the year.

Yet the gain is almost exclusively a result of USD weakness; in fact, the U.S. dollar index - a measure of broader USD performance - lost 10.7% in the first half of the year.

That was the weakest start to a year since 1973.

Because the Dollar is a global reserve currency, analysts say GBP/USD does not accurately reflect UK internal dynamics.

Instead, GBP/EUR gives the best insight into the UK economy and sentiment, with expected underperformance in the exchange rate over the coming months confirming growing unease about the UK economic trajectory.