Image © Adobe Images

Pound Sterling's latest slide means it is behaving as we expected.

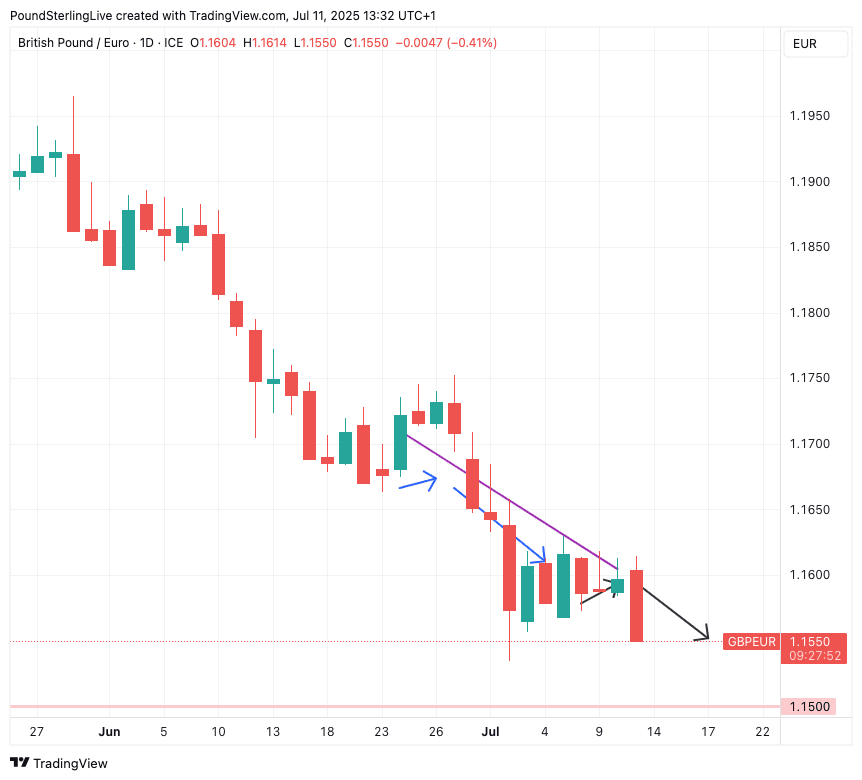

Three weeks ago, we published our regular Week Ahead Forecast that contained a chart showing a trend line and a couple of arrows that told readers what to expect from the Pound to Euro exchange rate in the coming two weeks.

Then on Monday, we updated that chart with our latest predictions:

It's always great to know the market is behaving as we expected it to, and those readers who have been keeping in touch should be comfortable with any decisions they have made.

As a reminder, we don't offer technical analysis, rather we try to set out some directional biases with likely levels, which allows readers to come to rational decision making when transferring funds.

Given the recent developments, the move to 1.15 we have been looking for remains intact.

So what is driving the latest fall in Pound Sterling?

A decline in UK GDP was reported on Friday, showing the economy shrank for a second consecutive month in May, this time by -0.1%.

The ongoing slump in industrial and manufacturing output was a major driver of the disappointment, while an uptick in the mighty services sector will have saved Chancellor Rachel Reeves from further blushes.

"Industrial production and manufacturing production also missing badly. GBP underperforming a bit at the margin, related to this news," says W. Brad Bechtel, Global Head of FX at Jefferies LLC.

Talking of Reeves, it was her teary appearance in the UK Parliament last Wednesday that refocussed minds on how dire the UK's finances are. The surprising sight of her crying behind Prime Minister starmer triggered a market selloff, as investors fretted he was about to ditch her for someone who might be more inclined to splash the cash.

UK finances are in a desperately poor state, as confirmed by the OBR this week, with the current government seemingly unable to make the necessary cuts. Unfortunately, for left-leaning readers out there, the wealth tax being touted as a solution simply won't cover the yards needed to bring the UK back on a sustainable footing.

With the economy struggling, and Reeves looking to raise taxes, it's little wonder economic sentiment is subdued, and will remain so until the Autumn.

At the same time, we can look forward to another Bank of England interest rate hike in August, and another by December, which should go some way in improving sentiment.

However, for the Pound, this turn towards further cuts will also weigh, as is traditionally the case when markets are focused on relative monetary policy.

For the Pound-Euro exchange rate specifically, the Bank of England's two (or maybe even three) rate cuts would surpass the number the European Central Bank will deliver. Indeed, today we heard from ECB Governing Council Member Isabel Schnabel that the bar was set high for further rate cuts in the Eurozone.

"EUR outperformance also perhaps related to the ECB's Schnabel, who said in an Econostream article, that 'the bar for another rate cut is very high' and that fear of downward pressure on inflation from a stronger EUR is 'exaggerated'. The major shift in tone on EUR from ECB officials continuing and spreading from not just Lagarde, but to many others on the board as well," says Bechtel.

Add to this Europe's relative attractiveness in the Trump 2.0 era, and we understand why Euro exchange rates are outperforming.

Given the above, we would be inclined to stick with our expectation for more GBP/EUR declines.