UK inflation is in focus this week. Image © Adobe Images

Pound Sterling's soft underbelly against the Euro is evident for all to see.

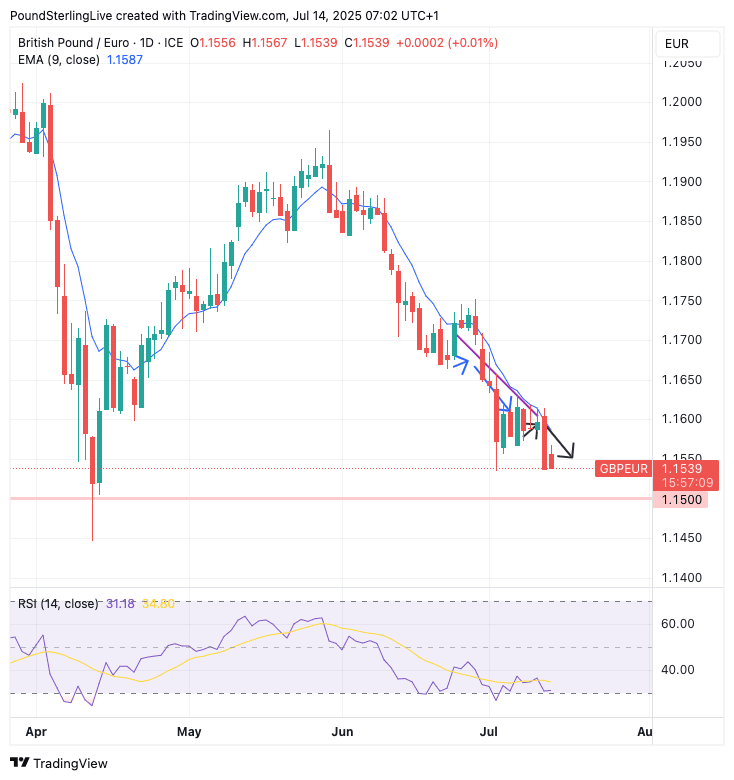

The Pound to Euro exchange rate (GBP/EUR) has fallen in six of the past eight weeks and we see little reason to bet against this trend in the coming five days.

Periods of strength in the pair are currently capped by the nine-day exponential moving average (EMA) on the daily chart, which is angled lower and confirms this could be the week when the 1.15 level is tested again.

The below chart shows the GBP/EUR at daily intervals, with annotations made three weeks ago on June 24 (blue lines and purple trend line). It then shows follow-up markers, made last Monday:

Above: GBP/EUR daily chart with previous Week Ahead Forecast annotations shown.

The past three editions of our Week Ahead Forecasts have proven to be on the money and we are minded to retain the chart and its annotations today, as it still gives a clear visual as to how near-term direction is likely to evolve.

On this basis, 1.15 is seen as the next objective, and below here lies 1.1446, the April 11 low, which is a possible target on a one-to-two week timeframe.

Friday witnessed another leg lower in the GBP/EUR selloff following the release of below-consensus (-0.1% m/m) UK GDP for May, which bolstered expectations that the Bank of England might speed up the pace it considers cutting interest rates.

This market assumption was backed by Bank of England Governor Andrew Bailey, who spoke to the Times newspaper and said the Bank stands ready to accelerate the pace at which it cuts rates if "slack" opens up in the economy.

Slack refers to an economy that is running below potential via falling employment and output, with central bankers judging that such outcomes are conistent with falling inflation.

The problem for the Bank is inflation is rising right now, despite the economy's stagnation, restricting the Bank to a cut-a-quarter pace. GBP softness suggests the market sees Bailey's comments as evidence that the pace can be accelerated to reach a runrate of a cut being delivered at consecutive meetings.

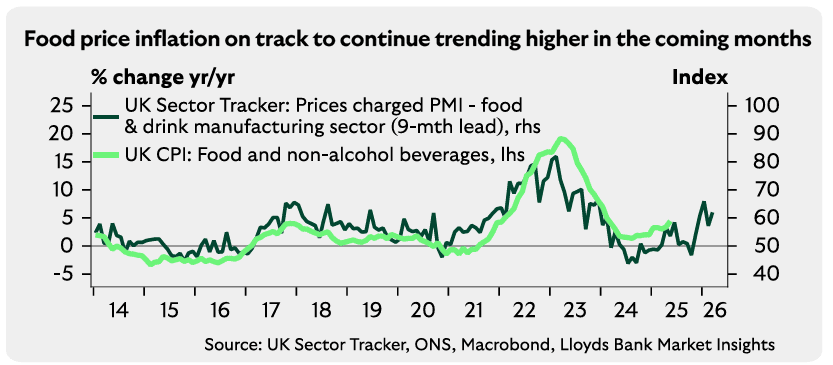

This week's UK inflation data, due Wednesday, will stir the debate further, although we see little prospect of it altering the Pound's prospects in a material way.

Typically, we would expect the Pound to strengthen when inflation beats expectations; however, we think an above-consensus inflation print would merely stir fears that the UK is entering a period of stagflation (high inflation combined with low growth). These episodes rarely support a currency.

Above image courtesy of Lloyds Bank.

The rate of CPI inflation is forecast to be unchanged from May’s 3.4% y/y print.

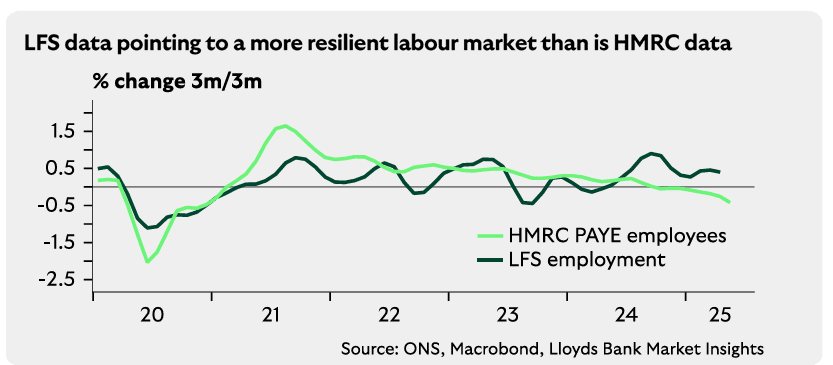

Thursday's UK labour market report is equally important for the Pound as it is expected to provide further indications that the UK labour market is cooling.

There are ongoing signs that Rachel Reeves' job tax is weighing on employment, and further job losses are likely. The problem for traders is that the UK's job market statistics are a mess, with some elements of the survey simply considered to be inaccurate.

"As has generally been the case in recent months, the extent to which conditions are viewed as having loosened is like to differ across the various measures. Most attention is likely to be on the HMRC/PAYE data which showed the number of payrolled employees fell for a seventh straight month in May," says a note from Lloyds Bank.

Image courtesy of Lloyds Bank

A soft jobs report will provide further evidence to the Bank of England that economic slack is opening up, inviting more interest rate cuts.

Also bear in mind that the Pound has been hit by bouts of concerns over the UK's fiscal position. Predicting these episodes is difficult, and we would just remind readers that this will remain a background concern that will simmer through the summer.

It provides additional support to the view that the Pound-to-Euro will stay pressured.