Image © Adobe Images

If the Bank of England is making a policy mistake, buying the Pound could make sense.

Strategists are looking at the rise in the British Pound following the Bank of England's policy decision as a fresh invitation to sell, judging that the UK economic setup is increasingly stagflationary.

"The kneejerk is GBP stronger, but a stagflation setup with a more-hawkish-than-expected central bank is not really bullish for the currency," says Brent Donnelly, a strategist at Spectra Markets.

Stagflation occurs when an economy stumbles to flat or negative growth while inflation rises, which describes the UK economy at present.

"The challenge for the MPC is the combination of still high inflation and weakening economic activity," says Knut A. Magnussen, a strategist at DNB Carnegie.

The deflationary setup doesn't lend itself to enduring Pound Sterling strength and Donnelly says he looks to sell recent Sterling strength on a short-term timeframe, opting to buy Euro against the Pound (EUR/GBP) in anticipation of the post-Bank of England move being faded.

Pound Sterling was the best-performing G10 currency for the first time in weeks following the Bank of England's 25 basis point interest rate cut. The cut was expected, but the clear signs of unease amongst a good portion of the Monetary Policy Committee (MPC).

The Bank was split 4-4 on whether to cut by 25 basis points or not, with one dissenter wanting an even chunkier 50bp cut. However, on a second vote, he switched to the 25bp camp, and the cut passed.

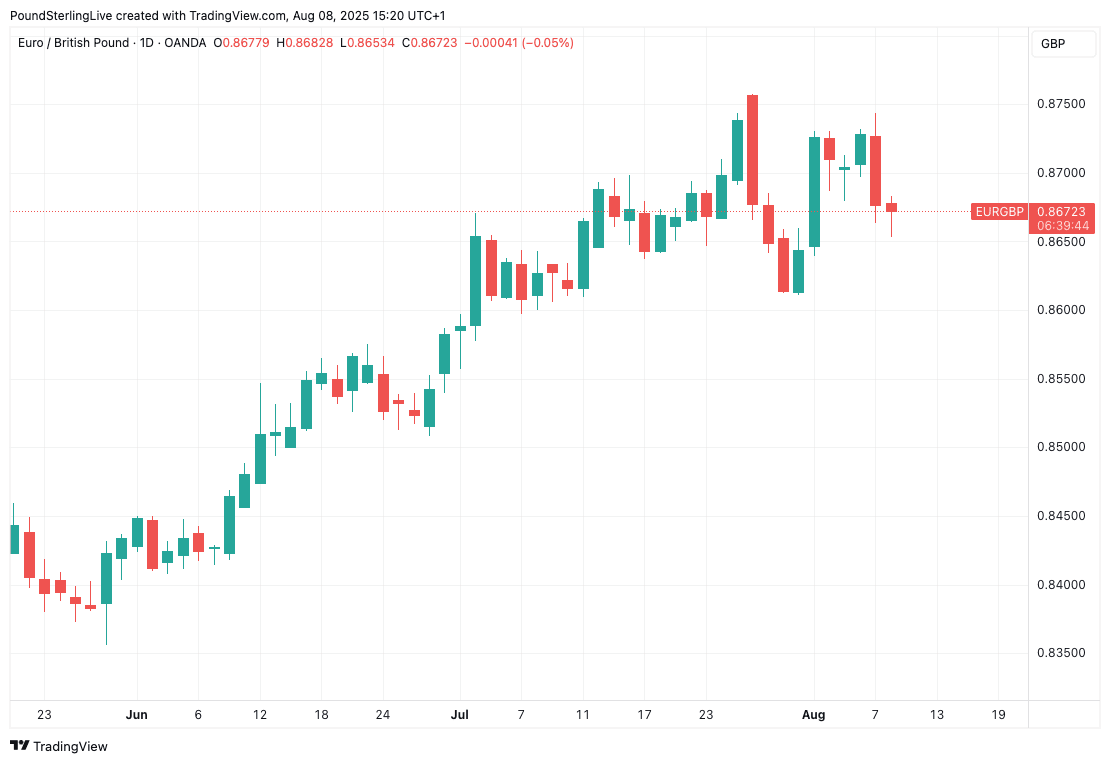

Above: EUR/GBP at daily intervals, a dip-buying opportunity?

Concerns about the Bank's judgment are evident in financial circles, particularly given signs of subtle political pressures potentially pushing the Bank's Monetary Policy Committee (MPC) to lean in favour of cuts.

The Bank is stretching the limits of its credibility by cutting while also raising its own inflation forecasts: it now sees CPI inflation hitting 4.0% in September, due largely to upside surprises in energy, food, and administered prices.

Medium-term inflation risks are also judged to be slightly higher than in May, with the 2026 (Q3) forecast being revised higher to 2.7% from 2.4%. The long-term (2027-2028) forecast shows inflation set at 2.0%, conveniently bang-on target.

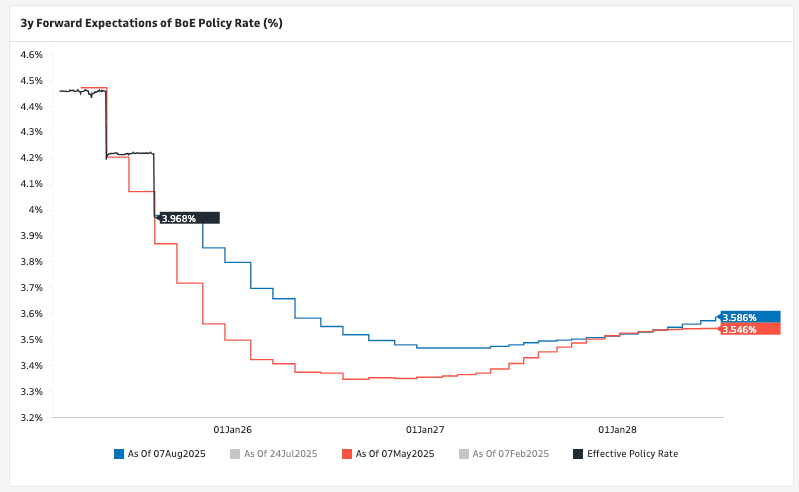

Above: Bank Rate expectations have lifted over the past two weeks.

A risk for Sterling assets - the currency and bonds - is that the Bank of England's credibility is undermined by the continued insistence on cutting interest rates into rising inflation.

A policy mistake becomes more likely, whereby the Bank is forced into an interest rate hike in the event of inflation continually exceeding forecasts. Usually, rising rates would be positive for a currency, but when these rate hikes are due to a policy error, and not because the economy risks overheating, they become a big negative.

Raising rates in a flat economy would only heighten the stagflationary setup, where the economy starts shrinking amidst high inflation.

UniCredit Bank thinks the market is going the wrong way entirely and that the Bank will cut interest rates more than is currently anticipated, in spite of Thursday's policy meeting.

Economists at the Italian-based investment bank expect two rate cuts over the rest of this year and 75bp of cuts next year; far more than financial markets expect.

Such a sharp reduction in interest rates would also weigh heavily: the old-fashioned playbook says a currency falls when the market shifts to anticipate more interest rate cuts would kick in.

"This is based on our forecast for further deterioration in the labour market. The risks are skewed towards a slower, quarterly pace. We see the bank rate ending next year at 2.75%, which we see as broadly neutral. At the time of writing, financial markets are pricing only a 70% probability of 25bp cut in the remainder of this year, and only 40bp of cuts by the end of next year, to 3.6%," says UniCredit.

The Pound therefore finds itself in a 'damned if you do, damned if you don't' setup whereby interest rate cuts and rises contribute to weakness.

The only real way out of this bind is for the economy to start growing and putting in some pleasant data surprises, as this diminishes the dreaded stagflationary setup while also justifying the UK's still-high overall interest rate setup.

The ball is now in Chancellor Rachel Reeves' hands to deliver.