Image © Adobe Images

Pound Sterling to extend a still-temporary rebound against Euro; UK jobs data & Eurozone inflation watched.

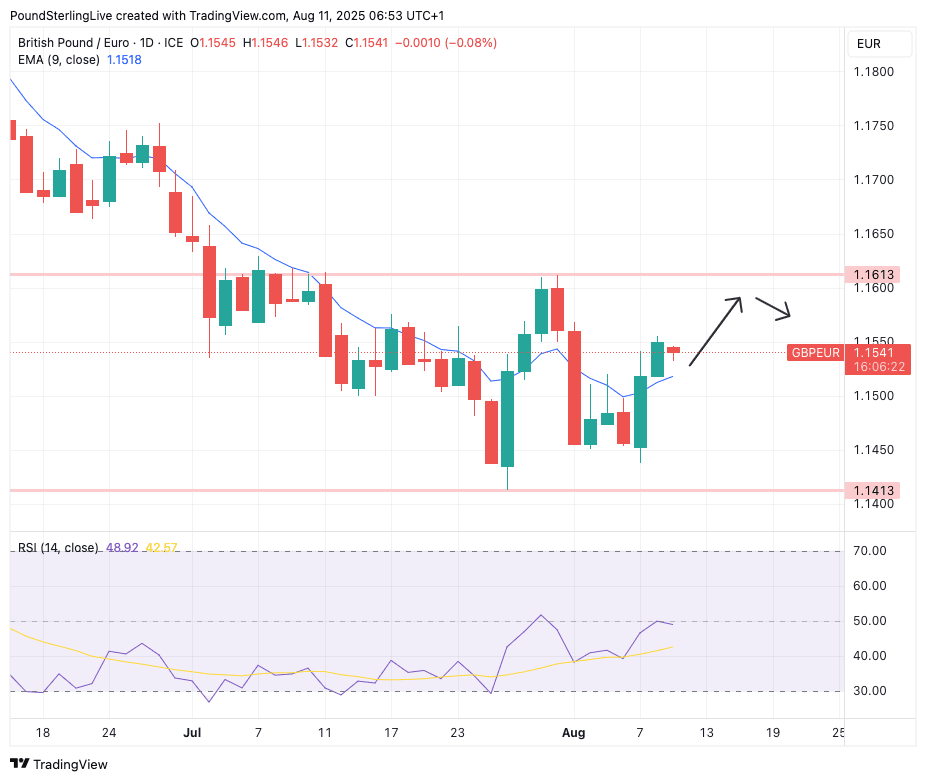

The Pound to Euro exchange rate rebounded 0.83% last week, spurred on by the Bank of England decision on Thursday, and momentum could carry it further in the near term.

The pair opens the new week at 1.1545, placing it in the middle of a sideways trending channel that has been in place since the 2nd of July. The top of that channel is 1.1613 and the bottom 1.1413; in the middle is the nine-day exponential moving average at 1.1518.

That the exchange rate is above the nine-day EMA on Monday is consistent with the potential for further near-term gains and is why we would anticipate the top of the channel at 1.1613 will be tested next.

A break of this ceiling would open the door to a move towards late-June highs at 1.1750. However, for now, we suspect the resistance level will hold and cap the advance

Momentum could be shifting too; the daily chart's RSI is also moving higher again and is no longer stuck in a lower gear in the 30-40 range, indicating the Euro could be losing its previous advantage.

The Pound's nascent rebound faces an initial test on Tuesday when the UK releases domestic payroll and unemployment data that should confirm the trend of a weakening labour market continued in June and July.

The unemployment rate is expected to remain steady at 4.7%, but a raft of measures of employment will likely point to an ongoing softening in the market that would typically weigh on Sterling.

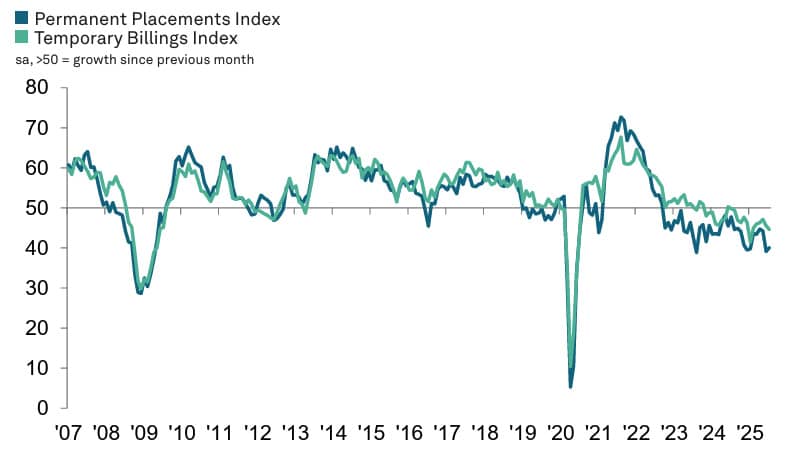

Surveys continue to point to deterioration, with KPMG and the REC's Report on Jobs for July was released on Monday, confirming the labour market is still suffering from the impact of higher payroll taxes and a hit to confidence.

REC/KPMG Report on Jobs, July 2025.

The report, which is also monitored by the Bank of England, said starting salaries for new workers were growing at the slowest pace since March 2021, and companies reported falling demand for workers in July.

This trend should be reflected in lower salary figures on Tuesday's official ONS release.

Weakening employment and salaries would typically invoke interest rate cuts at the Bank of England, which in turn would weigh on the British Pound.

However, last week's Bank of England policy decision revealed that the Bank was increasingly concerned about the UK's above-target inflation rates, while its own inflation forecasts for the near- and medium-term were revised higher in the Monetary Policy Report.

The market's takeaway from the event was that the Bank is increasingly concerned about inflation and might be more inclined to forgo another interest rate cut this year, disappointing a market that was looking for one more 2025 cut and at least one more next year.

"As of (Thursday), it was priced as a near-certainty that the Bank rate would end 2025 at 3.75%. Now, the market is less sure, and 2y yields are 5bps higher at the time of writing," says Sandra Horsfield, an economist at Investec. "Markets have reacted accordingly, with short-term rate expectations and sterling pushing higher."

It looks as though the Bank will be increasingly focused on inflation going forward, which means Tuesday's labour and wage data would have to show a significant deterioration in order to have a lasting impact on the direction of the Pound.

In the Eurozone, we get inflation data from Germany and Spain this week. These data should give a decent indication of where next week's Eurozone inflation print will land, and could therefore impact the market.

The sense is that the European Central Bank (ECB) has more or less completed its rate cutting cycle, but there is scope for another rate cut in September.

If the odds of this happening were to increase this week, on account of the German and Spanish inflation data, the Euro would come under pressure, although any significant reappraisal of Eurozone interest rate expectations is unlikely just yet.