Image © Adobe Images

A November interest rate cut at the Bank of England could put 2022 Truss-era lows in the frame.

Société Générale says pound sterling could be set to extend losses against the euro as the Bank of England could cut interest rates sooner than markets expect.

In a regular currency note, Soc Gen analyst Kit Juckes says "winter is coming" for the pound, explaining that "a UK rate cut at a time when the ECB is on hold" would have a noticeable impact on the level of the pound to euro conversion rate (GBP/EUR).

He explains that a client recently asked him how much EUR/GBP might rise if the market priced in more easing from the Bank of England.

The question's relevance becomes apparent when we note just how little the market currently expects from the Bank of England by way of interest rate cuts:

Money market pricing shows just one full cut is anticipated by the end of March; the rule of thumb is that a repricing for more rate cuts would weigh on the pound relative to the euro, where the European Central Bank is expected to keep interest rates unchanged for an extended period.

"The UK rates market doesn't fully price a BoE cut until the end of winter, next March. The Eurozone rates market doesn’t price a further ECB cut for a very long time indeed," explains Juckes.

However, he thinks the risks to the pound stem from an earlier rate cut than anticipated.

"I think the more relevant question is what might happen if we saw an earlier BoE move, due to a deterioration in the economic backdrop. Winter is coming, and so are higher taxes," he says.

The odds of a November cut are seen as low, with just 6 basis points priced. This means the pound is vulnerable to those odds rising.

"A UK rate cut at a time when the ECB is on hold, could put EUR/GBP 0.90 in the spotlight," says Juckes.

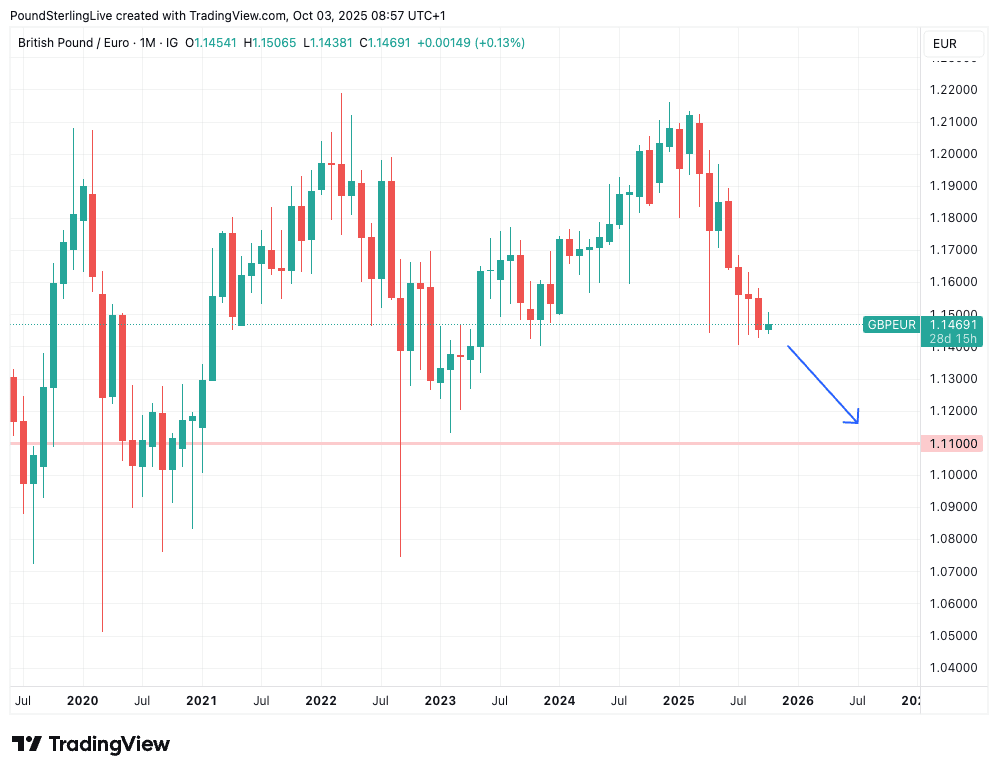

EUR/GBP at 0.90 gives a pound to euro conversion of 1.11. For context, this level was last visited during the Liz Truss days, when the exchange rate cratered to as low as 1.0843 in the wake of her ill-fated budget.

Above: GBP/EUR at monthly intervals, showing the relative move required to achieve a 1.11 forecast target.

And it's talk of budgets that is keeping sterling on edge in 2025.

We're in the run-up period to the November 26 budget, and markets are on the lookout for potential tax rises being floated by the Treasury.

This can keep the UK currency on edge.

In fact, Soc Gen's FX Volatility Wizard Barometer shows that GBP volatility stands apart from the broader G10 trend.

It shows that while most currencies have seen implied volatilities and risk reversals ease in recent months, Sterling remains an outlier.

EUR/GBP volatilities are higher than three months ago as spot tests resistance near 0.8750, and GBP/USD risk reversals have risen despite softer volatility, pointing to a clear bearish bias from the options market.

What this means is that traders and investors are buying hedging protection against a sharp fall in the pound as they see risks ahead.

"This divergence highlights the unique risk profile of GBP and the value of our Barometer in capturing these shifts," explains Juckes.

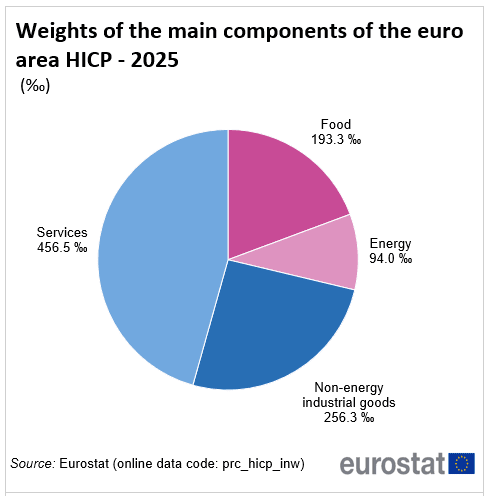

This week's data from the Eurozone meanwhile bolstered the view that the European Central Bank (ECB) should be happy to keep interest rates unchanged at coming meetings, which should favour the euro.

Eurostat reported the bloc's inflation rates stayed broadly steady, but services inflation picked up in key economies.

HICP inflation for September came in at 2.2% y/y, up from 2% in August. Core inflation held at 2.3% for a 5th straight month.

Services inflation meanwhile edged higher, to 3.2% from 3.1% in August.

The ECB should be broadly comfortable with this release.

"We continue to expect the ECB to keep policy on hold at least until end-2026," says economist Bill Diviney at ABN AMRO.