Above: Emmanuel Macron. GUE/NGL, accessed Flickr, reproduced under CC Licensing.

Pound sterling starts the new week with a solid advance against the euro, but can it make it stick?

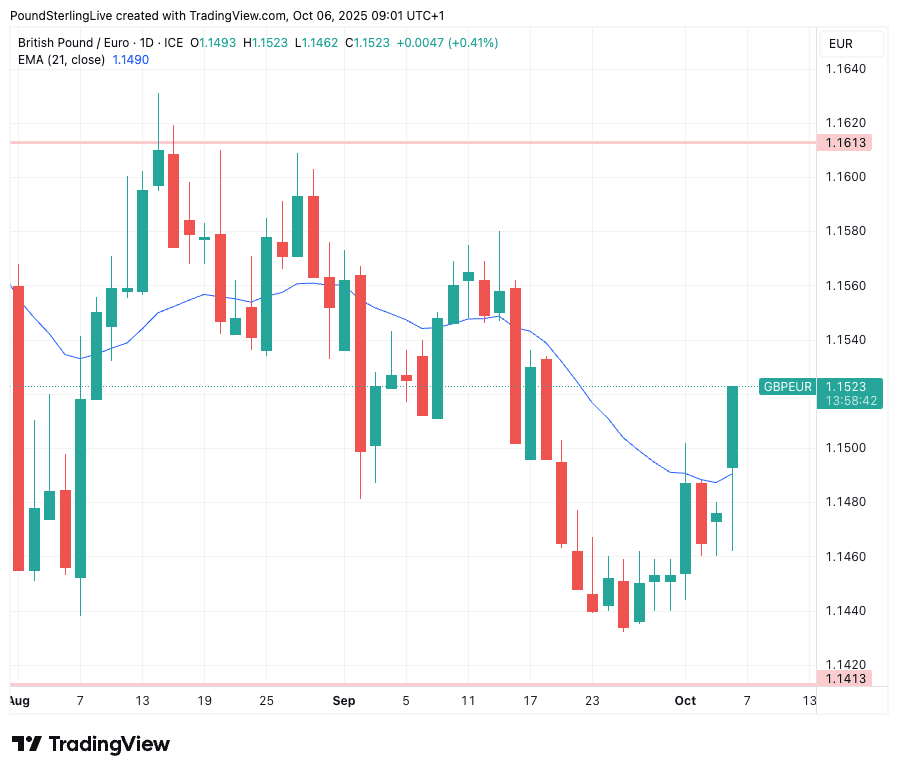

The pound to euro exchange rate (GBP/EUR) starts the new week with a solid 0.36% gain, hitting 1.1521, which is the highest level since September 18.

The move looks to be part of a broader selloff in the euro, as euro-dollar trades nearly two-thirds of a per cent down at 1.1664. In fact, looking at the performance chart, the euro is down against everything apart from the yen (which has some domestic politics on its mind).

We suspect the movement is linked to news of another French Prime Minister resigning: French President Emmanuel Macron last night unveiled his new cabinet which immediately drew criticism from across the political spectrum, most likely because it was broadly the same as the last one.

Prime Minister Sebastien Lecornu announced his resignation this morning, leaving France rudderless and significantly raising uncertainty on multiple fronts.

France's economy has been struggling of late as a result of this uncertainty, and today's news certainly bakes this theme into the outlook.

Concerns will build as to how the country can consolidate its debt amidst a political void, with matters certainly not being helped by further economic underperformance: economies must grow to service their debt.

We will be watching French sovereign debt yields through the day to gauge just how worried markets are. But for now at least, the currency is showing its displeasure.

In response, GBP/EUR rises through 1.15 and above the 21-day exponential moving average (at 1.1490), a key technical level that must be breached and defended if sterling is to enter a short-term uptrend.

If GBP/EUR closes above the 21-day, then 1.1560 becomes achievable in the coming days. Those with FX payment requirements should consider locking in current levels for a portion of their payment, and setting an order for higher levels to ensure they are not missed.

GBP/EUR had been under pressure through the August-September period but ultimately formed a base above 1.1440 in late September and early October.

The jump on Monday underpins that base and could even allow for a short-term rally to form.

However, the UK's own problems won't be forgotten and we think GBP/EUR upside could prove limited as a result.

Rally-busting issues include the Bank of England's desire to raise interest rates at any given opportunity and the government's inability to control spending, which inevitably boosts inflation and increases the odds of tax rises at the November 26 budget.

"The UK rates market doesn't fully price a BoE cut until the end of winter, next March. The Eurozone rates market doesn’t price a further ECB cut for a very long time indeed," says Kit Juckes, FX analyst at Société Générale. "What might happen if we saw an earlier BoE move, due to a deterioration in the economic backdrop. Winter is coming, and so are higher taxes."

Juckes says such outcomes could press a move in EUR/GBP to 0.90 and GBP/EUR to 1.11.

Pound sterling will keep its soft underbelly thanks to a challenging fundamental narrative linked to the government's spending policies and the Bank of England's inability to bring inflation under control.

The budget forecasting process began last week, with the Office for Budget Responsibility (OBR) giving the government an initial 'pre-measures forecast, one of a number of iterations ahead of the day itself.

OBR downgrades to productivity forecasts, increased social spending and higher debt costs mean the Chancellor will need to raise taxes, raising uncertainty for businesses and households.

For financial markets, the impact this uncertainty has on data will be important. Also, the market will be nervous about whether or not the government passes the credibility test when addressing the UK's difficult fiscal path.

"Sterling markets will be sensitive to any leaks on its contents," says a note from Lloyds Bank.

The new week commences with a timely article in Bloomberg that points to rising gold and bitcoin prices, which come at the expense of some currencies. It describes the phenomenon as the "debasement trade".

Investors are worried about inflation and lax fiscal policies, which ultimately debase traditional currencies.

The pound is a prime example of a currency at risk of debasement: the government has the spending taps turned fully on, ensuring UK inflation is the highest in the G7, and rising. And despite this, the Bank of England continues to insist it must go further with interest rate cuts.

In short, British authorities are doing nothing to protect the currency from debasement, something that will surely have an impact on the pound's long-term trajectory.