Image © Adobe Images

The Pound to Euro exchange rate has stabilised following recent heavy losses and could yet recover further up ahead but it faces downside risks heading into the medium-term, according to RBC Capital Markets strategists.

Sterling recovered off three-month lows against the Euro on Wednesday and Thursday before overcoming some minor Fibonacci resistance at 1.1675 and testing its 200-day moving average at 1.1685 on Friday.

But the pair is likely to remain buoyant, and perhaps even rise further in the short-term, as UK interest rates are seen remaining among the highest in the G10 group over the coming year.

“With markets pricing a total of -100bps by next May, there is space for rate dynamics to buoy GBP,” RBC Capital Markets strategists wrote in a review of their Sterling forecasts on Monday.

Above: Pound to Euro rate shown at daily intervals with Fibonacci retracements of November uptrend and selected moving averages indicating prospective areas of support.

“This pace of cuts would still leave the UK with relatively high rates in G10. But with risk sentiment turning more jittery and GBP outperforming YTD, we prefer a neutral bias on EUR/GBP in the near-term,” they said.

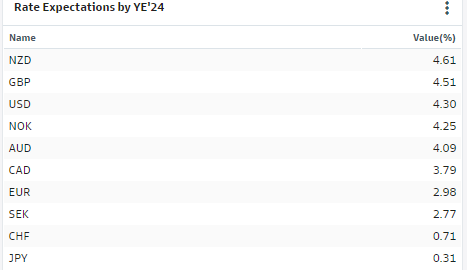

Overnight index swap rates implied on Friday that the Bank of England Bank Rate is likely to be the second highest in the G10 group at year-end even after the series of additional rate cuts envisaged by the market.

A comparatively high yield is likely to lift GBP/EUR further in the short-term but RBC Capital Markets strategists also say it’s likely to fall back to 1.1627 by year-end, and to 1.1235 next year.

This is because of risks stemming from the UK’s fiscal situation, and because the euro is likely to benefit more from the erosion of the US Dollar’s yield advantage once the Federal Reserve begins to cut rates.

“We have tempered the uptrend in our medium-term EUR/GBP profile, but it is still reflecting asymmetric downside risk to GBP,” they said, while tipping EUR/GBP to rise to 0.86 this year, and 0.89 next year.

Above: Market-implied expectation for G10 interest rates at year-end. Source: Goldman Sachs Marquee.