Image © Adobe Images

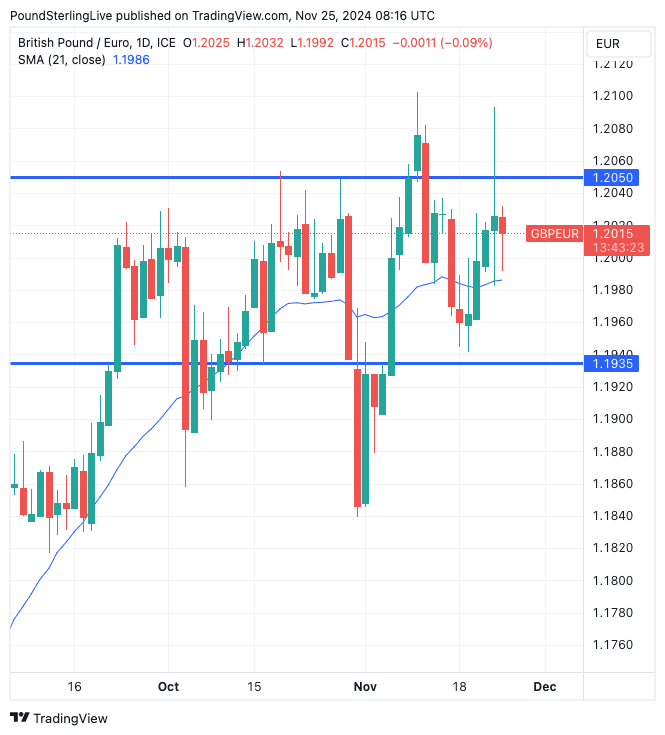

The Pound to Euro exchange rate (GBP/EUR) will respect the September-November range during the course of the next five days, with the 21-day moving average having a gravitational effect.

Eurozone inflation data will be the economic highlight of the week for the exchange rate, but the figures are only due on Friday, and events in the U.S. are again impacting global foreign exchange movements at the start of the new week.

Pound Sterling is stronger against the U.S. Dollar but is slightly under pressure against the Euro, with markets reacting to weekend news that Donald Trump has appointed Scott Bessent as his Treasury Secretary.

Bessent is a seasoned Wall Street professional who is seen as a better option than some of the more interesting names that were once considered for this all-important posting. His selection removes some of the more extreme tariff scenarios that had dominated FX markets after Trump's win.

The fall in the US dollar comes amid rising demand for U.S. bonds, which is a strong signal that markets welcome a pragmatic hire. This is particularly helpful for Euro exchange rates, as the Eurozone is highly exposed to US tariffs.

The news is understandably helping the Euro recover against both the Dollar and Pound, with GBP/EUR settling near 1.2020.

"We maintain our view that many negatives are in the price of the EUR already and would expect the currency outlook to stabilise but only in the absence of any significant escalation of geopolitical risks," says Valentin Marniov, Head of G10 FX Strategy at Crédit Agricole.

GBP/EUR spiked as high as 1.2094 last Friday following the release of disappointing Eurozone PMI data that showed the Eurozone was once again flirting with recessionary conditions in November.

However, the spike was soon reversed after UK PMI data showed the UK was not faring much better, thanks largely to a significant sentiment hit that followed the UK tax-grabbing budget of Chancellor Rachel Reeves.

The Pound tends to outperform the Euro when the UK economy is outperforming that of the Eurozone, but these PMI data suggest such UK exceptionalism is at risk of waning.

From a technical perspective, the picture reflects this, and we continue to see a high probability that the exchange rate will respect the September-November range. The top of the range is located at approximately 1.2050, and GBP/EUR has only closed above this level once this year.

The lower end of the range is at around 1.1935, with the pair only closing below here on a handful of occasions.

The majority of price action is now occurring around the 21-day moving average, which is in the centre of the range at 1.1986 and will be the centre of gravity for the exchange rate in the near term.

The highlight for the coming week will be the release of Eurozone CPI inflation figures as they could determine whether the European Central Bank (ECB) cuts interest rates by a sizeable 50 basis points at next month's interest rate decision.

Thursday morning, Germany's states will release inflation numbers ahead of the official German inflation release later in the day. Spain also releases inflation numbers on the day.

The German and Spanish releases often serve as a good guide as to where the Eurozone inflation release - due on Friday - will land, and because of this, the impact on the Euro can be notable if there are some surprising deviations from expectation.

Eurozone CPI is forecast to have risen to 2.4% from 2.0% in October, which should ensure the ECB sticks to a 25 basis point cut next month.

However, if the inflation data undershoots, then the ECB could consider cutting rates by more, particularly given last week's disappointing PMI data.

If this is the case then the Euro could come under pressure.

There are no major data releases due from the UK this week, leaving the Pound exposed to global elements.