Image © Adobe Images

Pound Sterling rallied after UK wages stoked inflationary fears and Germany's ifo sentiment indicator confirmed a tepid end to a poor 2024 for the Eurozone's largest economy.

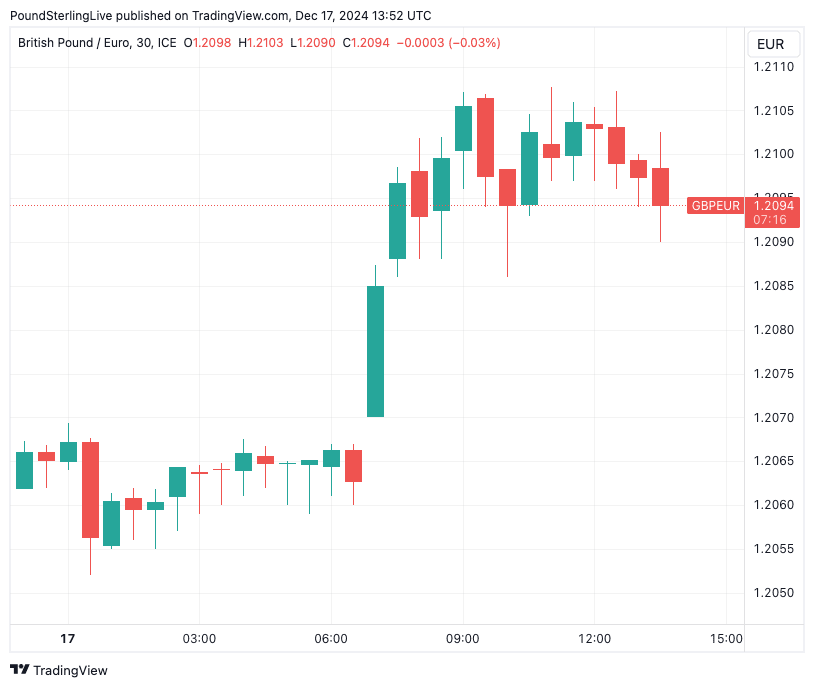

The Pound to Euro exchange rate rallied to the 1.21 mark after UK wage growth blew past expectations after hitting 5.2% in October.

The figure is in no way compatible with the Bank of England achieving a 2.0% inflation target, and markets are betting the response will be to keep UK interest rates higher for longer.

In fact, according to a reading of overnight index swaps, only two-and-a-bit interest rate reductions in 2025 are now anticipated.

At the same time, the European Central Bank (ECB) will comfortably cut interest rates by a greater margin, creating a yawning gap between UK interest rates and those of the Eurozone. Critically, the gap favours the Pound, and is why Pound-Euro has rallied towards two-year highs again.

ECB Governing Council member Olli Rehn said on Tuesday that he finds it to be the "right policy that we continue our rate cutting cycle once the new year starts."

With the ECB to be quick out the blocks in 2025, he thinks this can continue through to the "coming spring-winter". This is a wide target outlined by Rehn, as it implies the uber-dovish scenario for the ECB will see it cutting through to next December.

The ECB will have little choice but to ease monetary policy aggressively unless Germany gets its skates on and recovers.

The ifo Business Climate Index for Germany fell to 84.7 points in December, down from 85.6 points in November. This is the lowest level since May 2020 and the decline was due to more pessimistic expectations, although companies assessed the current situation as better.

"The only good thing about Germany's just-released Ifo index is that it is the final major macro indicator released this year. Time to take a breather and to end a year that will go down as the second consecutive year of economic stagnation," says Carsten Brzeski, Global Head of Macro at ING.

The UK economy is also stagnating, but crucially, wages are elevated enough to ensure inflation errs towards 3.0% rather than 2.0% at this stage.

The ONS said regular UK pay (without bonuses) rose to 5.2% in October from 4.9% and outstripped expectations for 5%.

Above: GBP/EUR hit 1.21 on Dec. 17.

"Sterling and Gilts are setting the tone after hot UK wage data," says Kenneth Broux, a strategist at Société Générale. "The acceleration to 5.2% 3m/yoy for both series is a disappointment for the BoE and simply is not compatible with 2% inflation. It reinforces the arguments of the hawks that policy must stay tight and any dialling back of restriction must be gradual."

Broux's colleague at Soc Gen, Kit Juckes, explains, "the EUR/GBP cross is as rate sensitive as all the others at the moment, and so maybe it’s no surprise that a stronger than expected set of wage data in the December labour market overview have helped edge EUR/GBP a little lower, again testing the 0.82 area."

"Given the political and growth woes of the Eurozone, we don’t expect GBP to weaken much against the EUR, but we don’t see dramatic downside either. If EUR/GBP trades under 0.81 over Christmas, I'll definitely stock up," he adds.

EUR/GBP below 0.81 equates to GBP/EUR above 1.2350.

Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole, says GBP should closely follow UK rates.

"We also note that the GBP has recently been trading at a significant discount when compared to its relative rate appeal vs the rest of G10. The GBP could thus regain some ground as FX spot starts to close the gap to its relative rate spread if the data comes in as expected and especially if it exceeds market expectations," he adds.