Above: Bailey often gives an interview on decision days that have no scheduled press conferences. File photo of Andrew Bailey. © Pound Sterling Live, Still Courtesy of Bloomberg.

There are two-way risks facing Pound Sterling today. Here, we examine what the potential 'hawkish' and 'dovish' outcomes would look like.

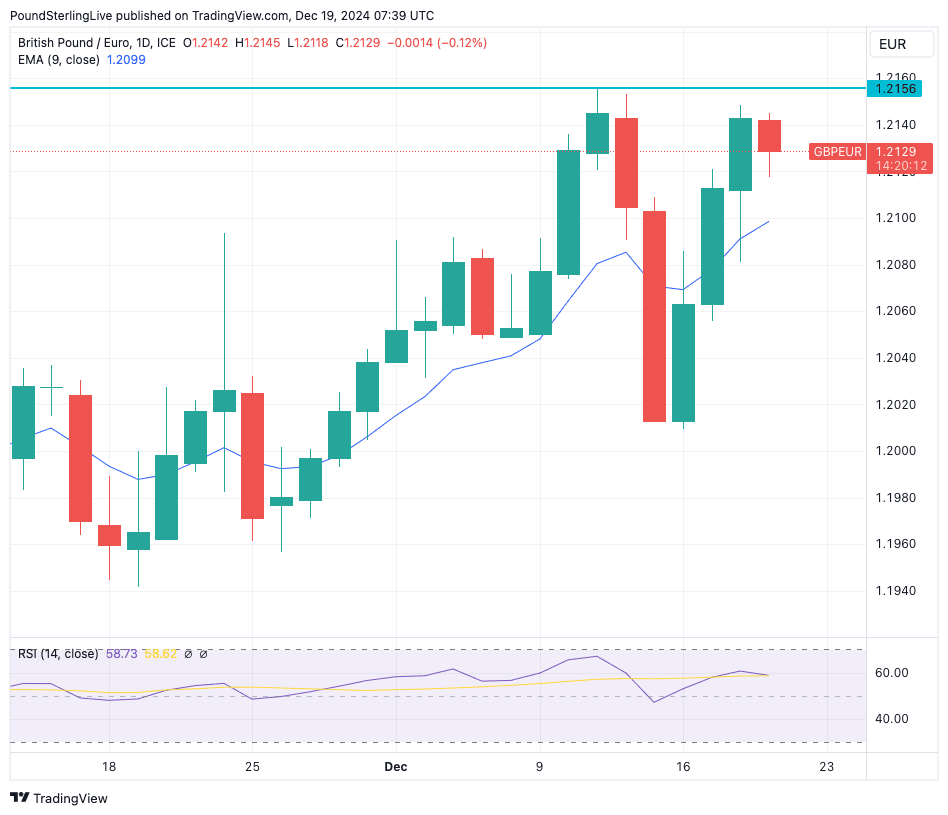

The Pound to Euro (GBP/EUR) conversion sits poised below the 1.2156 high in the approach to the Bank of England's final interest rate decision of 2024.

The Bank will leave interest rates unchanged, but what will it need to do to trigger further gains in the Euro? Likewise, what would send it lower?

Hawkish Outcome: Fresh Highs for GBP/EUR

Hawkish is a financial parlance used to describe a central bank that is leaning towards raising interest rates, or in the context of today's decision, a central bank that is rowing back from previously stated intentions to lower interest rates further.

Such outcomes are typically associated with rising bond yields and a rise in the currency.

Here, we would expect Pound Sterling and gilt yields to rise in tandem as markets lower expectations for the number of interest rate cuts that would likely be delivered in 2025.

The first signal the Bank would send under such an outcome is an overwhelming vote from the Monetary Policy Committee to vote to keep rates unchanged.

Only Dhingra is anticipated to vote for a cut, which would send the message that the vast majority of the MPC think inflation risks are growing again.

And so they should; UK CPI inflation rose to 2.6% y/y in November and looks likely to reach 3.0% before it hits the 2.0% target again. The pesky services inflation sub-component is at 5.0% and running above levels the Bank forecast at the November Monetary Policy Report.

Above: GBP/EUR at daily intervals.

The Bank's task is to bring inflation back to the 2.0% target, and with momentum going against them, any decisions or communications that might undermine the central objective could be detrimental.

Last week, the Bank's own survey of inflation expectations revealed a rise in public expectations for inflation to increase, with median expectations for the next year climbing to 3%, up from 2.7% in August 2024. Confidence in the Bank's abilities amongst the public were meanwhile shown to have fallen.

The risk is that inflation expectations will continue to grow, creating a self-fulfilling feedback loop in which businesses raise prices further and workers push for higher wages to compensate for expected price growth.

How the Bank addresses inflation developments is important: the Pound will likely rise, or at least hold recent gains if the Bank maintains recent guidance that a gradual removal of policy restraint is appropriate.

Here, we would also expect the Bank to say policy must stay restrictive for sufficiently long until inflation risks dissipate further.

There is no press conference due following the decision, but Bank of England Governor Andrew Bailey typically conducts an interview with a broadcast network following the decision, so we will be watching the newswires.

Expect him to shed more light on the decision that could trigger a movement in the market.

Dovish Outcome: A Fall Back to 1.20

A dovish outcome would describe a scenario where the Bank signals that the market is anticipating too few rate cuts on the horizon.

There is a good chance this will happen today, in which case the Pound-Euro exchange rate would likely slide back to 1.20 by the weekend.

A dovish outcome would see the Bank of England hint that market expectations for just two interest rate cuts in 2025 are too restrained.

Recent comments from Governor Bailey (made on Dec. 05) have suggested that four would be more appropriate, as it sticks to a quarterly rate cutting pace.

He would point to the recent weak run of GDP data (two consecutive monthly outturns of -0.1%) and survey evidence that private sector firms are cutting back on jobs.

The message would be that downside risks to growth and employment are emerging, which implicitly prompts the market to raise expectations for the number of rate cuts to come in 2025.

The Bank would also say the recent rise in inflation has 'base effects' to thank (i.e. falls in inflation one year ago mechanically raise the current outturn), which some analysts pointed out in the wake of Wednesday's inflation release.

Bailey would also use his post-meeting press interview to reiterate his message sent on the 5th of December that progress on inflation is being made and that four cuts in 2025 seem appropriate.

The ratcheting up of expectations for a cut would ease UK bond yields and drag the Pound lower.

That being said, for now, we would anticipate weakness in the Pound-Euro rate to be relatively contained, as there is limited scope for Bailey and the Bank to send 'dovish' signals.

The Euro is also likely to stay under pressure owing to the Eurozone's poor economic and political fundamentals.

The bigger downside risk would come against the Dollar, as we now know the U.S. Federal Reserve thinks it will only cut interest rates twice in 2025, creating scope for the Bank of England to 'outcut' the Fed.