Above: Chancellor Rachel Reeves' budget plans will be stymied by the rise in bond yields we have witnessed today. Picture by Simon Walker / HM Treasury

The British Pound really should be higher following an above-consensus inflation print.

However, it is lower against most of its peers, signalling growing investor fears that the UK might be entering a period of stagflation.

Inflation data was hot right across the board, from services to goods, from housing to transport, meaning the 'breadth' of inflationary pressures is elevated, discounting the notion that a couple of one-offs are to blame.

This raises the risk that the Bank of England abandons its interest rate cutting cycle sooner than anyone expected. In fact, money markets now have just one more 25 basis point cut 'priced' for the remainder of the year.

"Strong underlying inflation is more obvious," says Andrew Wishart, an economist at Berenberg Bank, noting that recent data have been flattered by statistical tricks. He warns inflation is now too high for another Bank of England rate cut.

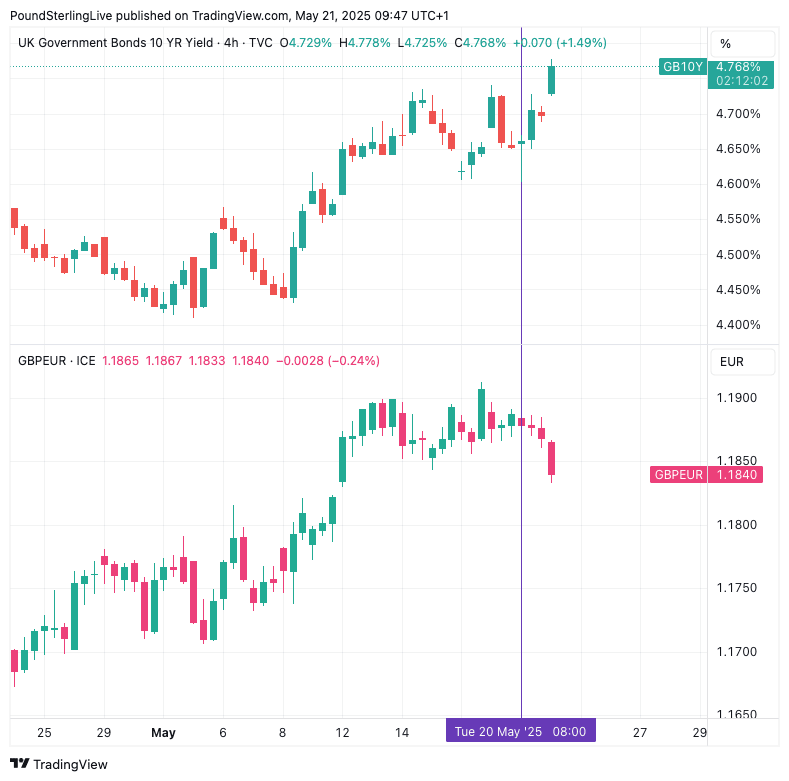

This shift in expectations is etched in bond markets where the ten-year bond yield has spiked 1.55% to 4.771%, meaning the cost of government borrowing is rising, which will worry Chancellor Rachel Reeves.

Normally, higher yields would spell a higher Pound, but when yields and the Pound decouple, it confirms investors are confirmed.

The worry is the UK is entering a stagflationary period of elevated inflation and low growth, and this is bothering Sterling: the Pound to Euro exchange rate is down by a quarter of a per cent at the time of writing at 1.1839.

Above: GBP ten-year bond yields have spiked but GBP/EUR has fallen (lower panel). We can see a breakdown in the correlation at the blue vertical line that hints some unease.

In fact, it is down against the majority of G10 currencies, which speaks of idiosyncratic GBP weakness.

High inflation is pushing up UK bond yields, which means the cost of government borrowing is set to remain high. It also means pressure will grow on the government to enact more economic growth-killing tax hikes in the Autumn.

Currencies rise when their economies are on the up, and the UK's looks decidedly unattractive given the stagflationary tones.

Yet, there are the usual suspects in the UK economic fraternity - the perma doves - who say this is a mere temporary blip and it will all calm down again soon.

They have been saying this for months, and yet here we are: inflation continues to rise amidst signs that consumers and businesses are increasingly disenchanted with the view that the 'miraculous disinflation' will win the day.

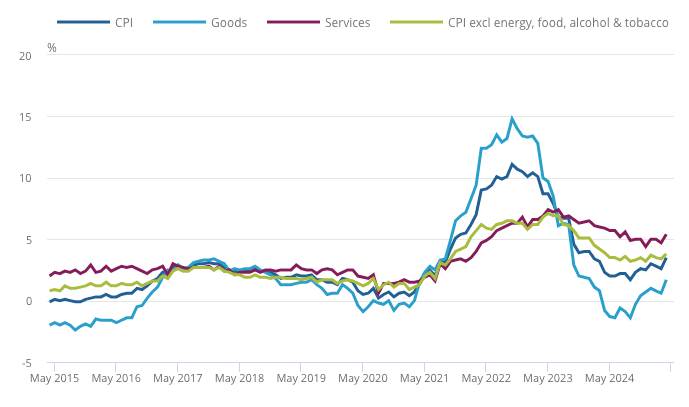

Above: Inflation won't fall to 2.0% until services inflation falls materially. Unfortunately for the optimists, it's rising again.

Most worryingly, services inflation jumped from 5.0% in March to 5.4% in April, easily outstripping the Bank of England's prediction made in the May Monetary Policy Report.

Berenberg's Wishart says it could rise further: "That would be evidence that demand is solid enough for companies to pass on increases in their costs, and force the BoE to take an extended pause in their cutting cycle until services inflation is on a downward path again."

Services inflation matters, as headline inflation can't fall sustainably to the 2.0% level until it falls, and it needs to fall materially. Yet, instead of falling, it is actually rising.

This discomfort is clearly weighing on the Pound today.