Gilts and the pound fell in July when Chancellor Reeves was defeated by her own party on attempts to lower welfare spending. Image: Parliament TV.

France's political problems risk exacerbating the UK's fragile financial standing.

Rising borrowing costs in France are pulling up corresponding borrowing costs in the UK, at a time when the UK government is setting its next budget and will likely limit pound sterling's ability to rise.

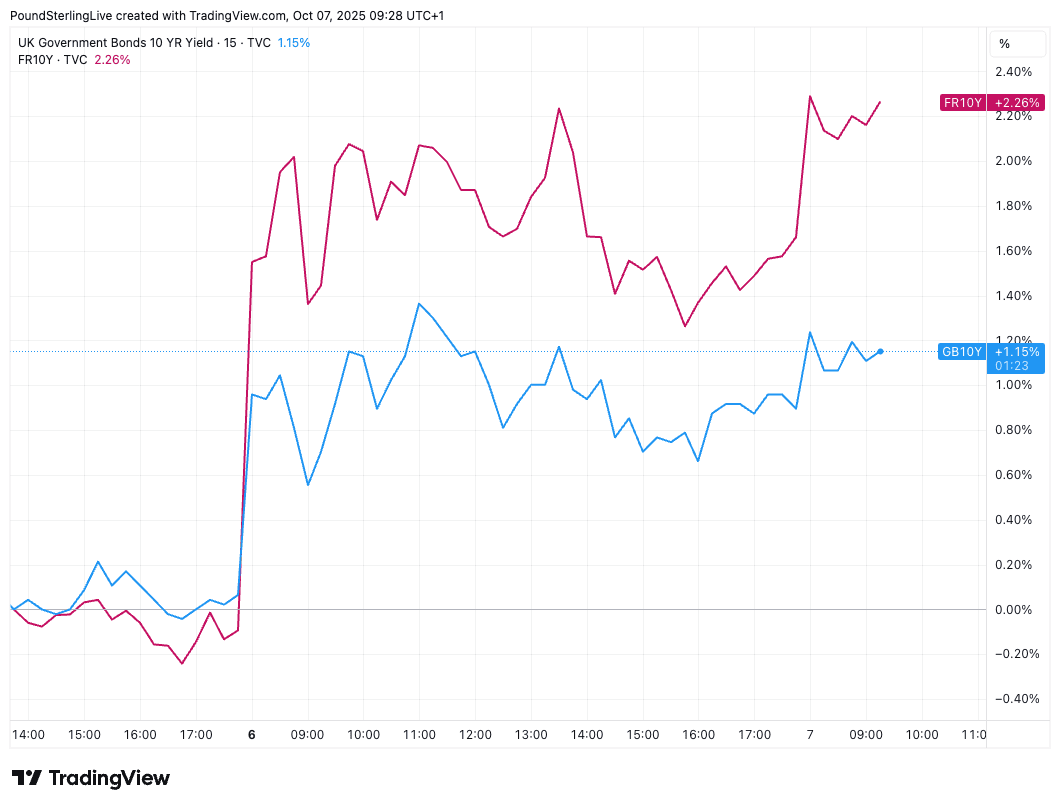

The cost of borrowing rose sharply in France on Monday after the failure of yet another government, meaning the country will almost certainly be unable to consolidate its increasingly unsustainable debt trajectory.

Rising borrowing costs across the channel drew corresponding costs higher in the UK, with domestic bond yields rising in response to the more pronounced jump in their French counterparts.

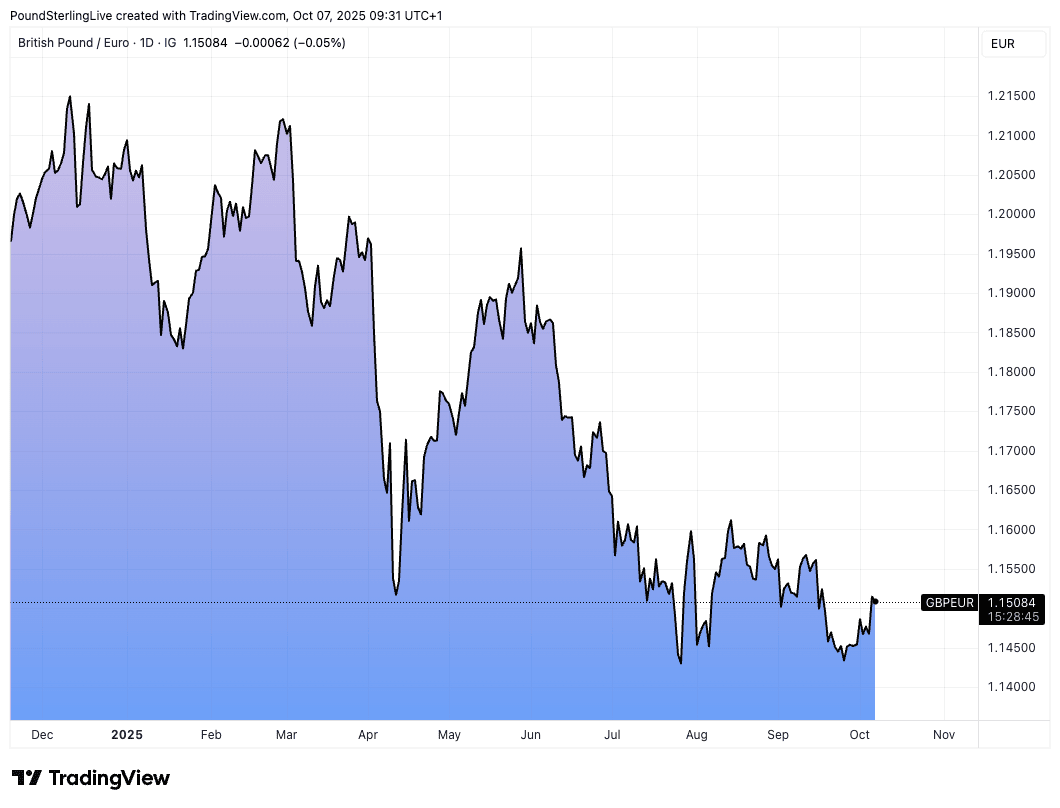

The pound rose against the euro in response, but fell against a host of other major currencies, signalling that demand for UK assets as an alternative to those in the Eurozone is tepid, at best.

This is understandable:

"We've also seen spillovers into other fiscally compromised sovereigns, including gilts," says Sam Hill, Head of Market Insights at Lloyds Bank, referencing UK bonds, which are known as gilts.

Above: The rise in French bond yields drew UK borrowing costs higher, turning the heat up on the British government.

"These developments come at a nervous time for the UK, the government currently in discussions with the OBR over its economic assumptions," he explains.

The UK government is in a similar position to that of France in that it is unable to pass any reductions in spending through parliament, as exemplified by a failed attempt to cut benefit spending in July to the tune of 'just' £5BN.

Despite having a large majority in Parliament, left-wing members of the ruling Labour Party blocked legislation to reduce some benefit spending, sending gilts and the pound tumbling.

Although UK assets have since regained composure, gilt yields are still uncomfortably elevated and command a premium relative to most G7 peers. The pound is meanwhile near multi-week lows against the euro and other European assets, despite Monday's France-inspired rally.

Hill explains that the Office for Budget Responsibility, which provides the forecasts the government needs to set its budget, will likely revise lower some key projections.

Most important of which is the productivity forecast which is to be cut, thereby automatically lowering the expected revenues the Treasury should receive.

This in turn increases the budget gap that must be filled via lower spending and tax rises. With spending unlikely to be cut, the onus falls on taxes, meaning the government is at risk of suffering unintended side effects.

Above: GBP has lost notable value against the EUR this year as concerns about the economy and debt build.

The best example of such an outcome is last year's increased tax on national insurance contributions, which has prompted businesses to cut back hiring.

Now rising debt costs, linked to France, only make the government's situation all the more difficult.

"The expected downward revision to the productivity forecast risks adding to the impact of current budget slippage, U-turns made on spending cuts and new spending demands, alongside the eroding effects of elevated bond yields. The mooted fiscal hole of 'only £30bn' is looking increasingly best case against all of that," says Hill.

Although France might at first appear to offer a route to a higher pound vs. euro, the reality is that it could be a harbinger of problems the UK is about to face and why pound sterling upside should remain limited into November.