Above: File image of Huw Pill, Chief Economist at the Bank of England. Image © Sérgio Garcia/Your Image for ECB.

A key member of the Bank of England is unlikely to vote for a November interest rate cut.

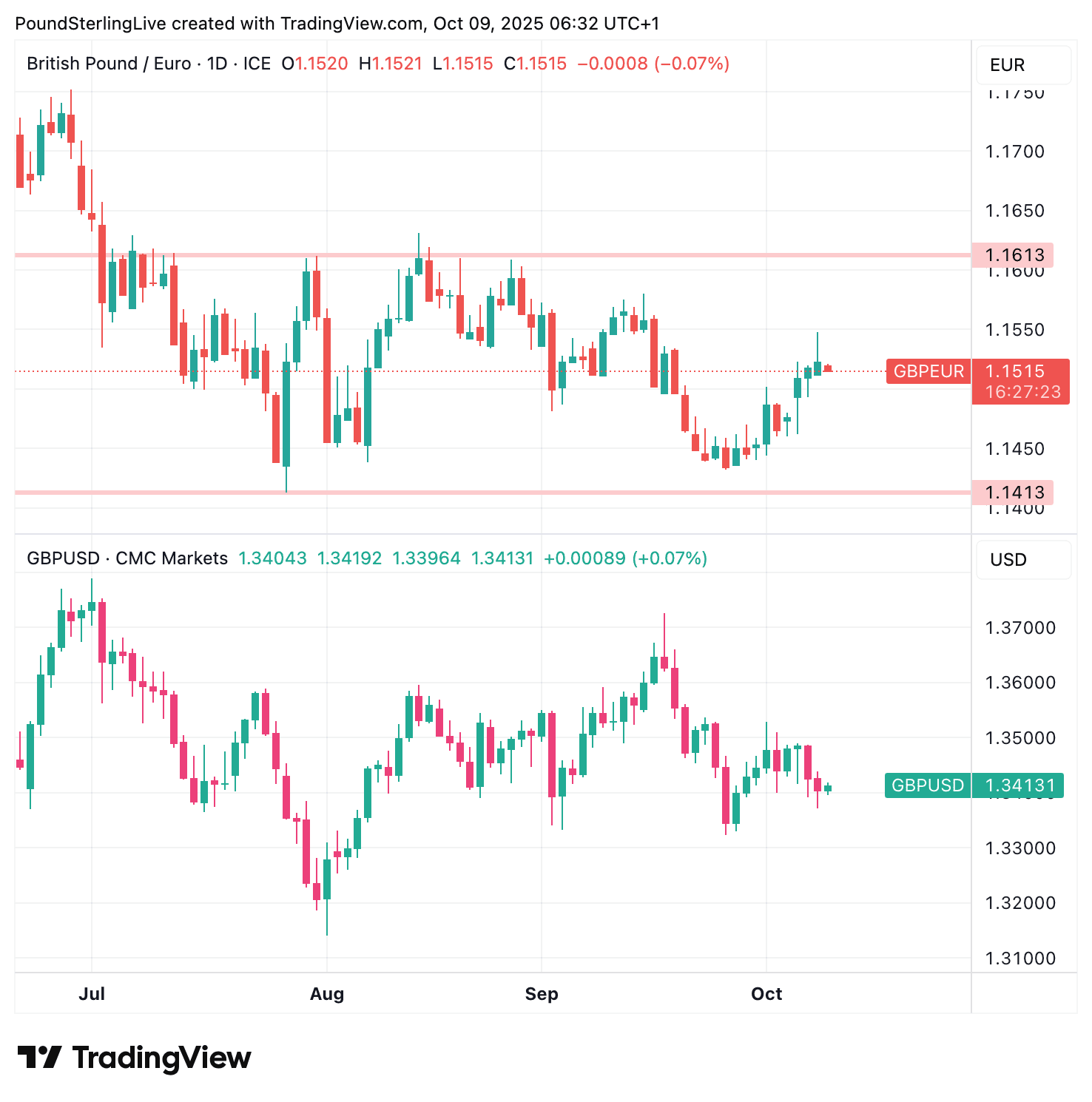

The British pound can extend its current recovery against the euro and other major currencies if the Bank of England leaves interest rates unchanged at next month's policy decision.

Hugh Pill, the Bank's Chief Economist, will be instrumental in influencing what fellow Monetary Policy Committee (MPC) members opt to do, and luckily, we have some crucial new insights into how he might vote.

Pill told an audience in Birmingham on Wednesday that the Bank's "monetary policy should be resolutely focused on price stability."

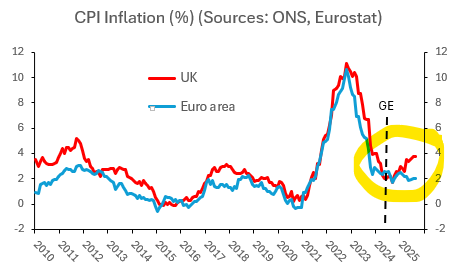

With inflation expected to peak close to 4.0% this quarter, Pill's speech makes clear that getting inflation back down to 2.0% should be the Bank's primary objective.

Given the UK's high inflation rates, the odds of a rate cut would certainly be off the table were it not for a number of Pill's colleagues who would rather cut interest rates to insure against any deterioration in the employment situation.

For sure, unemployment is ticking higher with PAYE payroll data showing a consistent month-on-month decline since last year. Q3 survey data have meanwhile showed the economy is also losing momentum.

"Holding policy too tight for too long comes with costs to output and employment, which could then pull inflation below target," said Sarah Breeden, Pill's fellow MPC member, in a recent speech. Dave Ramsden, Alan Taylor and Swati Dhingra are all likely to share these concerns.

Were the Bank to take heed of these developments and cut interest rates, the pound would come under pressure.

"Markets currently price only 41 bps of cuts over the next year. We expect the BoE to ease more aggressively than that and maintain an overweight in Gilts. We also remain underweight the pound as it will likely suffer in an environment where the BoE cuts rates more than expected," says a note from strategists at BCA Research.

Above: UK inflation is heading the wrong way. Image courtesy of economist Julian Jessop.

A November rate cut potentially sets the pound up for a soft year-end and would mean the recent pick-up in the pound to euro exchange rate is unwound. It would also potentially confirm that the pound to dollar rate's rally has ended, risking a slip back to 1.30.

However, if the Bank does not cut intererest rates, pound sterling could find support from the UK's elevated interest rates relative to elsewhere.

As Chief Economist at the Bank, Pill has significant sway, particularly over how his fellow permanent MPC members vote.

He said in his speech that the Bank's mandate is clear: it must achieve price stability consistent with 2.0% inflation.

Above: A November cut could send GBP to its range lows against EUR and USD.

With UK inflation potentially hitting 4.0% y/y in September, Huw argues "that monetary policymakers should make a clear and credible commitment to achieve their price stability objective."

He warns the Bank must pursue a "credible commitment to an aggressive monetary policy response should inflation get out of hand" as this "induces behaviour that makes it much less likely that inflation will get out of hand. A virtuous, self-reinforcing cycle of stability is created."

How Pill's thinking sways Governor Andrew Bailey will be important, as it could well be the Governor's vote that provides the tie-breaker in November.

With anxiety over the UK budget likely to grow in the coming weeks, the pound will, at the very least, need a credible inflation-fighting central bank in its corner.