File image of Chancellor Reeves. Picture by Lauren Hurley / DESNZ.

Falling bond yields are weighing heavily on the pound.

Some Big Downside Moves

The British pound is under renewed selling pressure against the euro, dollar and other major currencies on Wednesday, lead by a fall in UK bond yields.

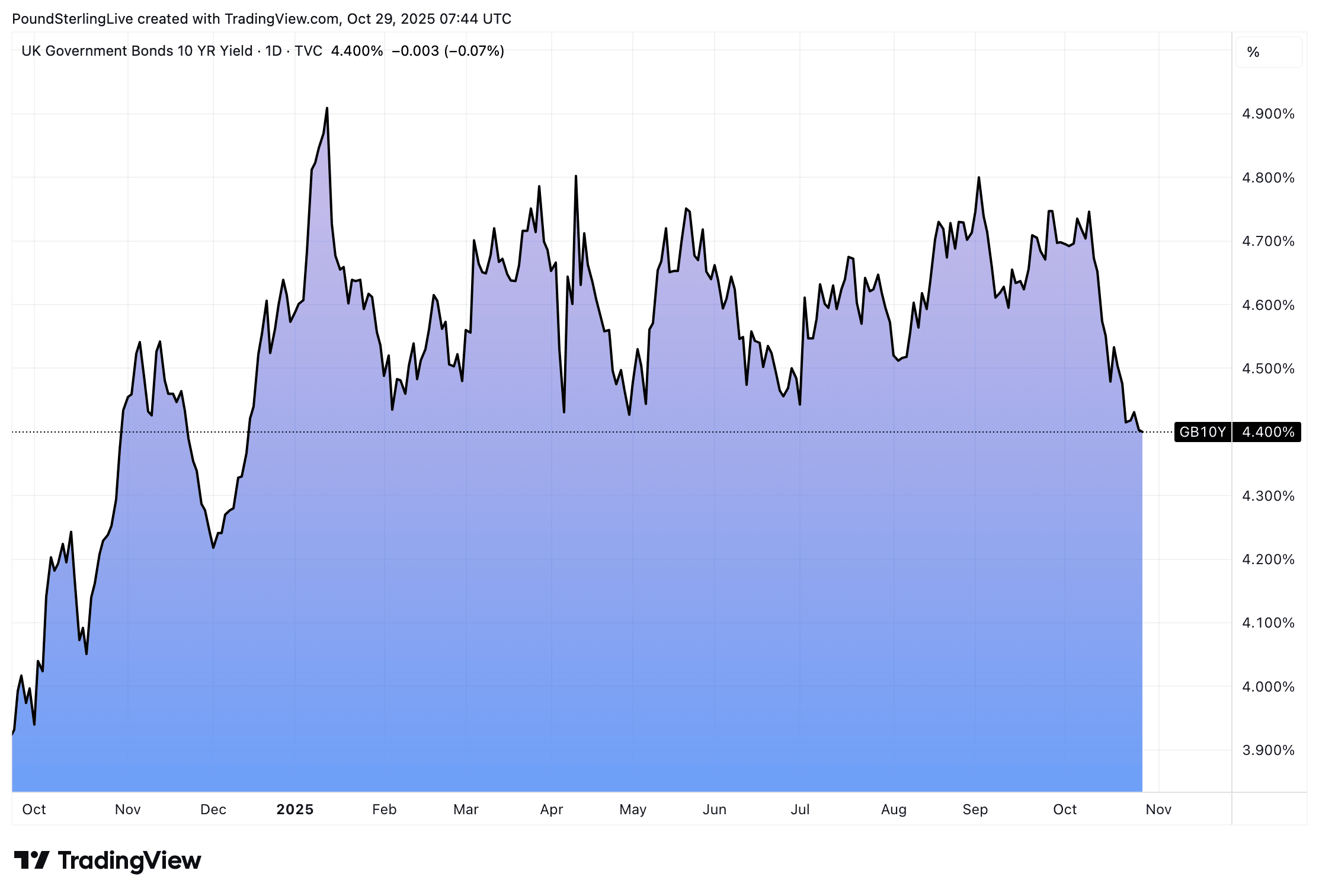

To be sure, bond yields are falling globally, but they're falling by greater margins in the UK.

This is unambiguously good news for the UK's embattled Chancellor, Rachel Reeves, ahead of the November 26 budget, as it means the cost of government borrowing is coming down.

But for sterling, it implies weakness: bond markets play an overwhelmingly large influence over currency movements.

Two-year Lows

Confirmation of this dynamic is clear:

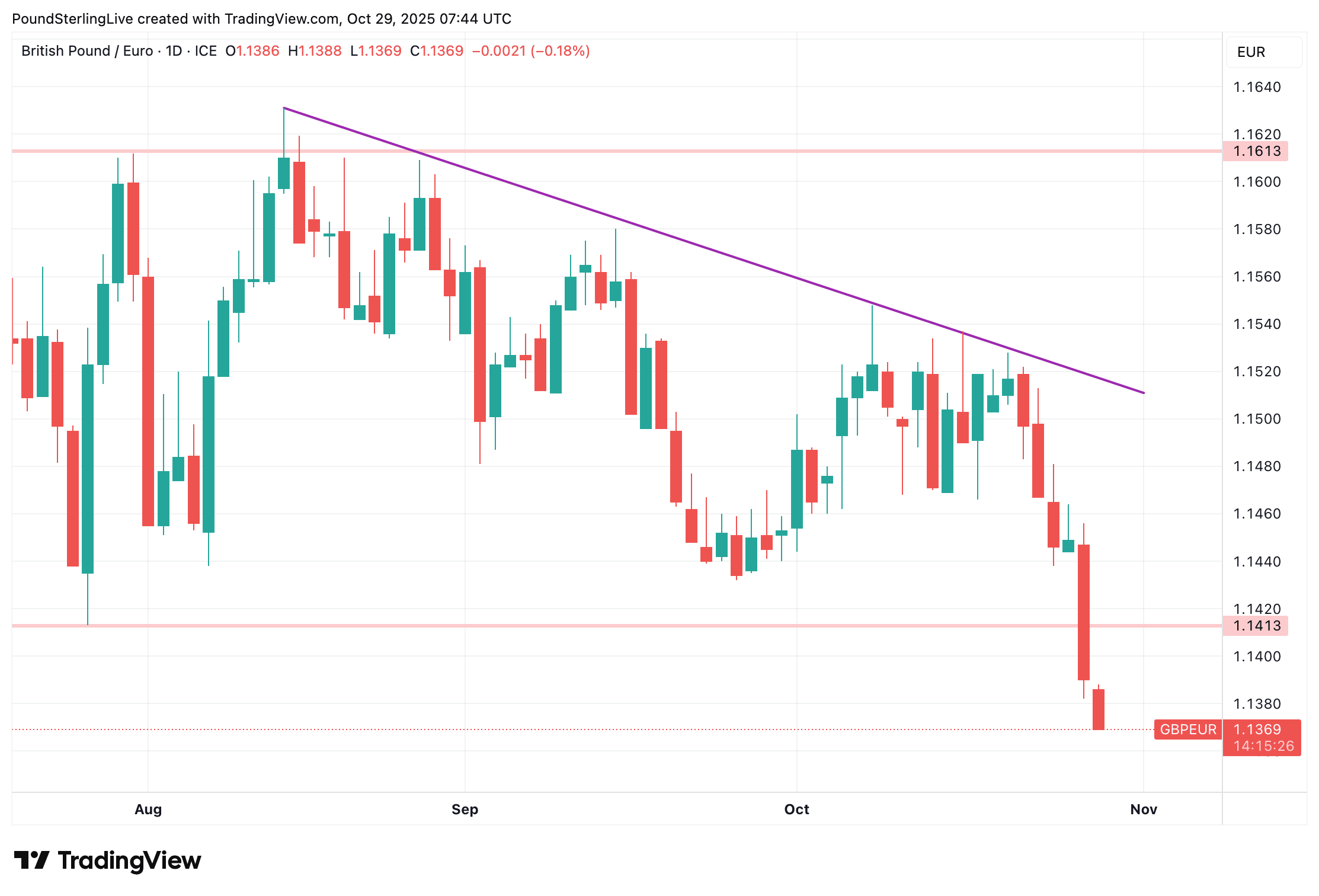

The pound to euro exchange rate is testing new two-year lows at 1.1373 on Wednesday morning after the UK ten-year bond yield - a key benchmark in bond markets - fell to its lowest level in 2025 on Tuesday at 4.37%.

The pound to dollar exchange rate has on Wednesday fallen to its lowest level since August 01 at 1.3229. Other notable moves include GBP/AUD, which is at its lowest level since February and is about to hit 2.0.

Announcement: The investment bank consensus forecast targets for the next 12 months are out. Request your GBP/EUR copy here, and GBP/USD copy here.

Why This is Happening Now

The key to understanding GBP weakness rests with falling borrowing costs, which rests with expectations for future Bank of England interest rates.

In turn, what the Bank of England does at upcoming interest rate meetings will rest with what the government does at next month's budget, reflecting the fact that bond yields lie at the intersection of government and central bank decision-making.

Above: Borrowing costs are fallinig. Image shows the ten-year cost of borrowing.

The view is that the government is going to have to squeeze the economy, not necessarily through spending restraint, but via higher taxation.

Economic theory suggests that such constraints will pressure inflation lower, allowing the Bank of England to cut faster, which is leading to lower bond yields.

The Trigger

The trigger to the pound's fall, which is mirroring that fall in bond yields, is yesterday's confirmation that the government will need to find an additional £30BN in taxes and savings next month.

An FT signalled that the OBR (the UK fiscal watchdog) would downgrade productivity growth by even more than first assumed in its next forecast. A 0.3ppt downgrade effectively means the government faces a £20BN shortfall. Add to this the need to run a minimum breathing space surplus of £10BN, and we are looking at a black hole of at least £30BN.

Above: GBP/EUR has fallen to two-year lows.

"This means that the fiscal backdrop will be even more tricky than previously assumed," says Danske Bank in a morning note.

This amounts to a significant fiscal squeeze that will hinder inflation and allow the Bank of England to cut rates faster and further.

That assessment by markets is reflected in falling bond yields and the pound.

"This means that we will have to see an even more significant tightening of fiscal policy from the government to meet its fiscal objectives. We think the latest developments only further highlight the tricky backdrop for the UK economy and stay negative GBP," adds Danske.

Is There Scope for a GBP Rebound?

Some might argue the pound is looking pretty oversold at current levels, particularly given there are no clear negative news events driving the move lower in sterling.

Indeed, we always knew the government would need to deliver eye-watering tax increases.

We also knew the Bank of England would likely cut interest rates further than money market pricing has implied.

So we think this selling is getting ahead of itself, but from a tactical perspective, fighting the trend would be costly, so it's prudent to position for further losses near-term.

"It is our central view that GBP will continue to edge lower vs the EUR into 2026," says Jane Foley, Senior FX Strategist at Rabobank. "The pound is on the back foot again vs. the single currency."

However, once the budget day passes, and assuming no major mistakes are committed by Reeves, scope for a rebound into year-end becomes clearer, particularly if the pound starts trading at a discount against fair value.