Image © Adobe Images

Why Pound Sterling doesn't like news of rocketing inflation and bond yields.

The Pound is down and yields are up following above-consensus inflation.

Rising bond yields and a falling Pound mean there is a disconnect in how financial markets usually work, hinting at growing investor concerns, as yields and the currency typically move in tandem.

Headline inflation surged to 3.5% year-on-year in April from 2.6% in March, said the ONS, surpassing estimates for a reading of 3.3%. Core inflation jumped to 3.8% y/y from 3.4%, and worryingly, services inflation jumped from 5.0% in March to 5.4% in April.

Although there were some real seasonal surges that won't be repeated next month, there was a wide breadth of rises across the entire inflation basket, spelling concerns that underlying pressures are more acute than previously estimated.

"Get used to this," says Andrew Wishart, UK Economist at Berenberg Bank, "strong underlying inflation is more obvious. CPI inflation of between 3.5% and 4.0% for the rest of the year is likely to be too strong for the Bank of England (BoE) to cut interest rates again."

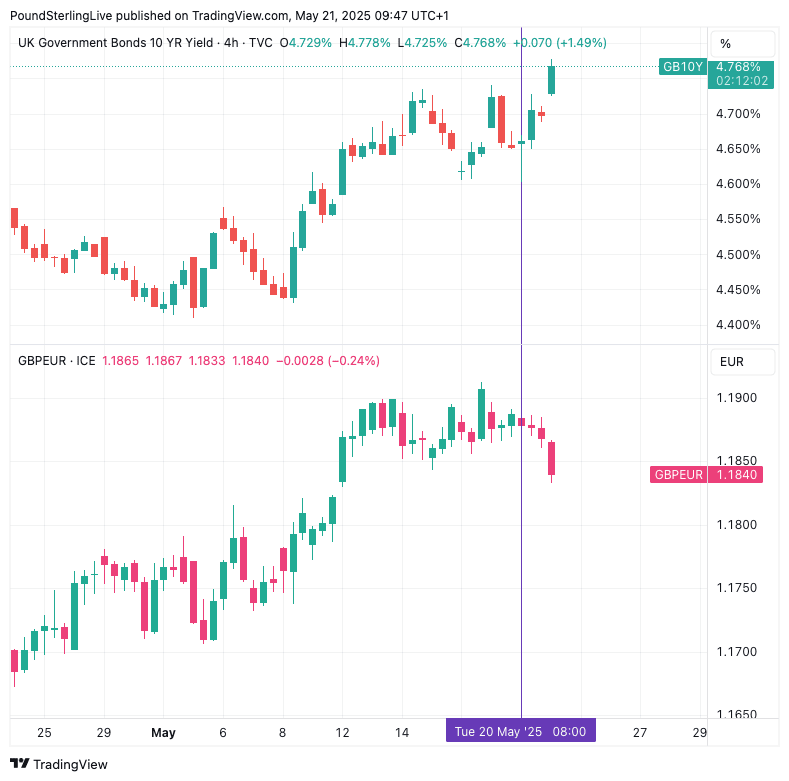

Above: UK ten-year bond yields leap, but GBP falls (lower panel). This disconnect in the reaction function is a red flag.

The market agrees, and money market pricing shows just one more 25 basis point interest rate cut is now expected this year.

Reflecting this shift in expectations is a surge in UK bond yields, with the ten year rallying 1.50% on the day to 4.77%, meaning the cost of government borrowing is rising in response.

Typically, rising bond yields lift the Pound, but we are seeing the opposite: the Pound is down, which means investors are nervous of the unsavoury cocktail that is being stirred, one which gives a bitter taste of rising inflation and falling growth.

We'll call it the Stagflation Cocktail.

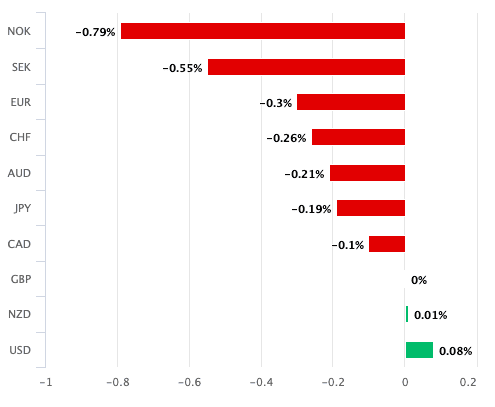

The Pound to Euro exchange rate initially rose in response to the data, but is now trending lower to 1.1832. The Pound to Dollar rose to a new 2025 high, but this was exclusively on the back of the bigger USD selloff we are seeing. It is now at 1.3402.

Confirming idiosyncratic worries, we see Pound Sterling is down against the majority of its peers:

GBP on May 21.

Berenberg's Wishart says services inflation could rise further from here, making a return to the Bank of England's 2.0% target almost nigh impossible for the foreseeable future. He explains that rising services inflation "would be evidence that demand is solid enough for companies to pass on increases in their costs."

It would force the Bank of England to take an extended pause in its cutting cycle until services inflation is on a downward path again, he says.

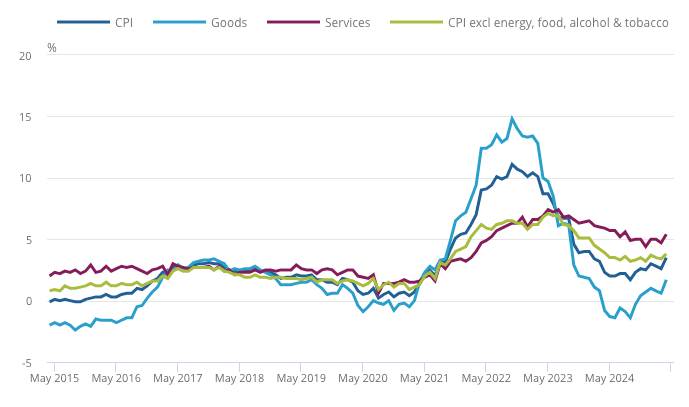

Services inflation matters, as headline inflation can't fall sustainably to the 2.0% level until it falls, and it needs to fall materially. Yet, instead of falling, it is actually rising.

The last time the ten-year bond yield rose to these levels, Sterling fell (April 09), suggesting the market has a line in the sand for what it thinks is a sustainable cost of debt.

Discomfort is clearly weighing on the Pound today.

Above: Until services inflation falls, headline CPI will remain above the Bank of England's 2.0% target.

These data come just a day after the Bank of England's Chief Economist, Huw Pill, said he thought the Bank of England was cutting interest rates too fast.

News of above-consensus figures will bolster Pill's argument and curtail bets for an August rate hike, meaning we might have to wait until November for the next reduction.

"Service price momentum still looks sticky – as Huw Pill noted in his speech yesterday," says George Buckley, European Economist at Nomura. "We’ll need to see further progress on disinflation (from underlying pay growth, services inflation, the price balances of the surveys and inflation expectations) to be confident in expecting another rate cut in August."

Stagflation Risks...

Sometimes the market can react negatively to high inflation data if it thinks they point to stagflationary risks. Stagflation is where inflation rises but growth falls, creating an awful domestic cocktail for investors, businesses and consumers.

"Businesses are facing a perfect storm of cost pressures which is fuelling inflation alongside rising household bills. While April’s jump was expected, the scale, to 3.5%, is concerning," says Stuart Morrison, Research Manager at the British Chambers of Commerce.

... or a Temporary Blip

Another constraint on upside in the British Pound is the view at the Bank of England that inflation will spike temporarily and then suddenly fall back to its target 2.0% level at some time in the near future.

It is this perennial optimism that the Bank is prone to displaying that allows it to keep raising interest rates. As mentioned, Huw Pill sees the risks. However, some of his colleagues are outright bent on cutting interest rates, regardless of inflation.

They will point to elements of the inflation print that are likely to be temporary:

- Gas and Electricity Prices (Energy): +7.5% (gas), +2.9% (electricity)

- Vehicle Excise Duty (VED) Changes

- Airfares (Transport Division): +27.5%

- Water and Sewerage Charges: +26.1% (MoM)

The risk, however, is that high inflation begets higher inflation, i.e. firms and consumers start expecting it, and therefore start changing their own behaviour accordingly. This means inflation expectations become embedded and contribute to sticky inflation rates.

"The Bank of England remains concerned about persistently high services inflation, along with the rise in expectations for inflation amongst households and businesses which have the potential to influence price and wage setting behaviour. This jump in inflation is not helpful against that backdrop," says Anna Leach, Chief Economist at the Institute of Directors.

Rising inflation expectations will frustrate the Bank's efforts to lower inflation and ultimately risk its credibility, which would be bad for UK assets, including the Pound.