Rachel Reeves looks forward to a summer of planning more tax rises to cover rising debt costs. Picture by Kirsty O'Connor / Treasury.

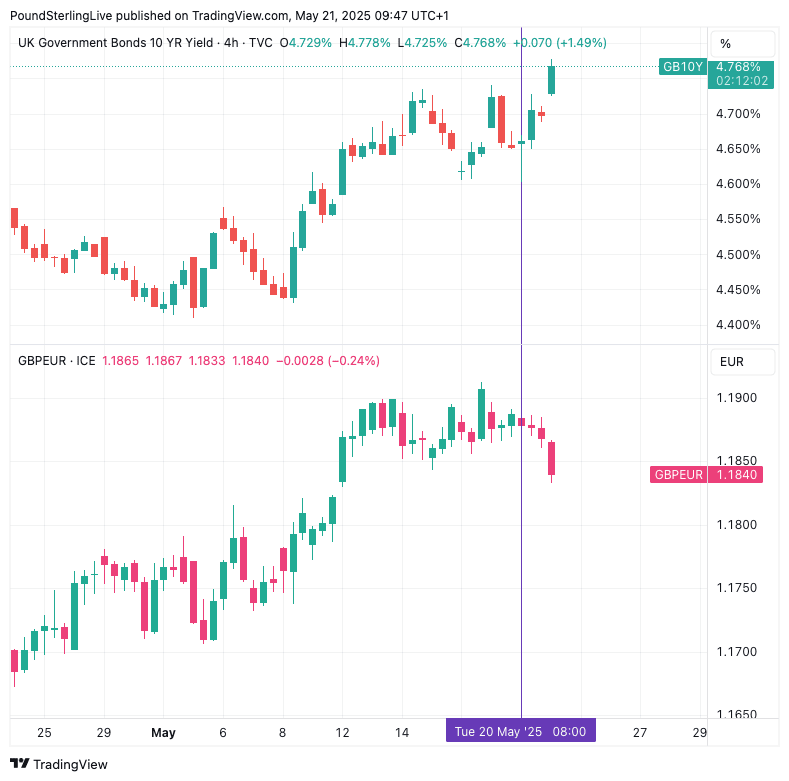

The British Pound's refusal to track bond yields higher is a warning sign.

Financial markets are struggling to determine whether the UK's rising bond yields are beneficial or detrimental to the currency:

Bonds fell and their yields rose following Wednesday's inflation release that showed inflation breezed past consensus expectations in April. On Thursday, yields pushed towards 2025 highs after UK public borrowing beat expectations.

Under typical circumstances, international buyers would purchase these discounted bonds to take advantage of the increased yield they offer, which in turn bids the Pound higher. However, the Pound weakened on Wednesday and is treading water on Thursday, signalling some concerns over the UK's inflation and debt dynamics.

Sterling's failure to launch should be taken as a warning to investors and those watching the market that risks are building.

We have seen breakdowns in the relationship between yields and the Pound in the past: most recently in January, when markets fretted about the UK's debt dynamics amidst a slowdown in UK growth. However, it was the famous fall in the Pound and spike in yields that followed Liz Truss' mini-budget that most readers will remember.

During the Truss selloff, investors worried about the UK's ability to repay its debt, and what we are seeing now is a hint that similar concerns are building.

Britain's ten-year bond yield - a benchmark measure of government borrowing costs - spiked to 4.79% on Thursday, bringing it to within touching distance of 2025 highs.

This was after the ONS said the government borrowed £20.155BN in April, the fourth-highest April borrowing since records began in 1993, exceeding economist estimates for £17.9BN.

Parting ways: UK bonds up, Pound to Euro rate down. A sign of investor unease with inflation and debt dynamics.

The above chart shows the Pound usually tracks rates higher, but it has failed to make gains recently, a sign that foreign investors have concerns.

"The failure of GBP to hold onto gains following hawkish CPI data may suggest the market is more concerned about stagflation than inflation," says Daragh Maher, Senior FX Strategist at HSBC. "GBP gains on rates have justifiably reversed on stagflation concerns."

Stagflation is where prices rise but the economy stagnates or even shrinks, which is a headwind to the domestic currency.

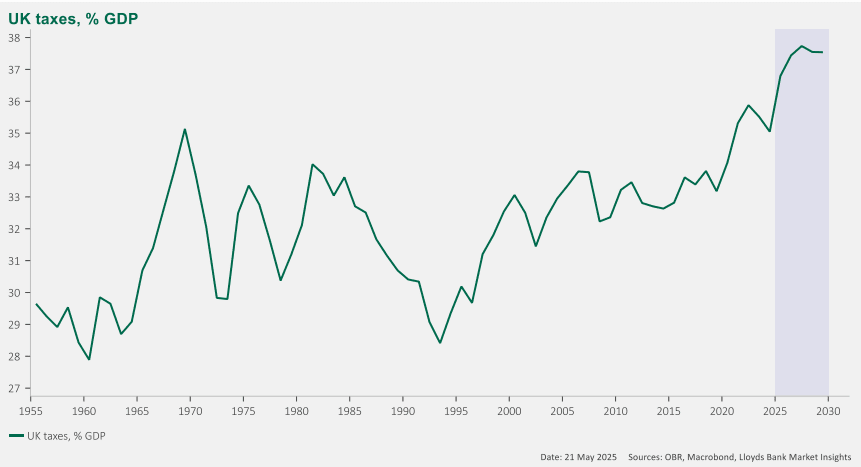

Hot inflation also raises the cost of the UK's debt repayments and UK Chancellor Rachel Reeves will have to find more ways to cut spending and raise taxes to ensure she meets her rules to bring debt down again by the end of the Parliament at the end of the decade.

Reports suggest it is tax hikes that will be on the menu, which will raise the UK's tax burden beyond the record highs that we are already witnessing, threatening future economic growth.

"As inflation surges, we need to remember that 25% of our debt is index linked i.e. roughly one-quarter of the UK government's borrowing is tied to inflation," says The Taxpayers' Alliance. "So if inflation goes up, so will the payments on the national debt which already costs taxpayers over £100bn a year."

The UK tax burden will reach new records.

And it's not just the government that faces higher borrowing costs; already, we are hearing that mortgage providers are revising rates as they anticipate the Bank of England will need to hold back from cutting interest rates over the coming months.

"What is most worrying about the current situation is the persistently positive trend in inflation," says Alex Kuptsikevich, chief market analyst at FXPro. "Further policy easing will now require more justification from the central bank."

Money markets see just one further 25 basis point interest rate cut coming from the Bank in 2025, with a second being priced at 50/50.

"This makes for an uncomfortable print for the BoE worried about the inflation hump and inflation persistence," says Sonali Punhani, UK Economist at Bank of America.

Yet, It's Too Soon to Dump the Pound

When a confidence crisis hits, it hits hard, and the Pound would be at risk of plummeting.

However, we're not at a crisis point yet, and it could be costly to bet too heavily on a major GBP selloff.

There is a decent chance that nerves calm and foreign buyers step back into the UK market and push the Pound higher.

"A slower pace of rate cuts is likely to support GBP against both EUR and USD," says Nick Andrews, Senior FX Strategist at HSBC.

The question is whether and when that demand comes back.

If what we are seeing are market jitters that give way to a return in confidence, then the Pound should bounce back in relatively short order and extend gains.