Image © Adobe Images

Watch the Bank of England and New Zealand labour market statistics this week.

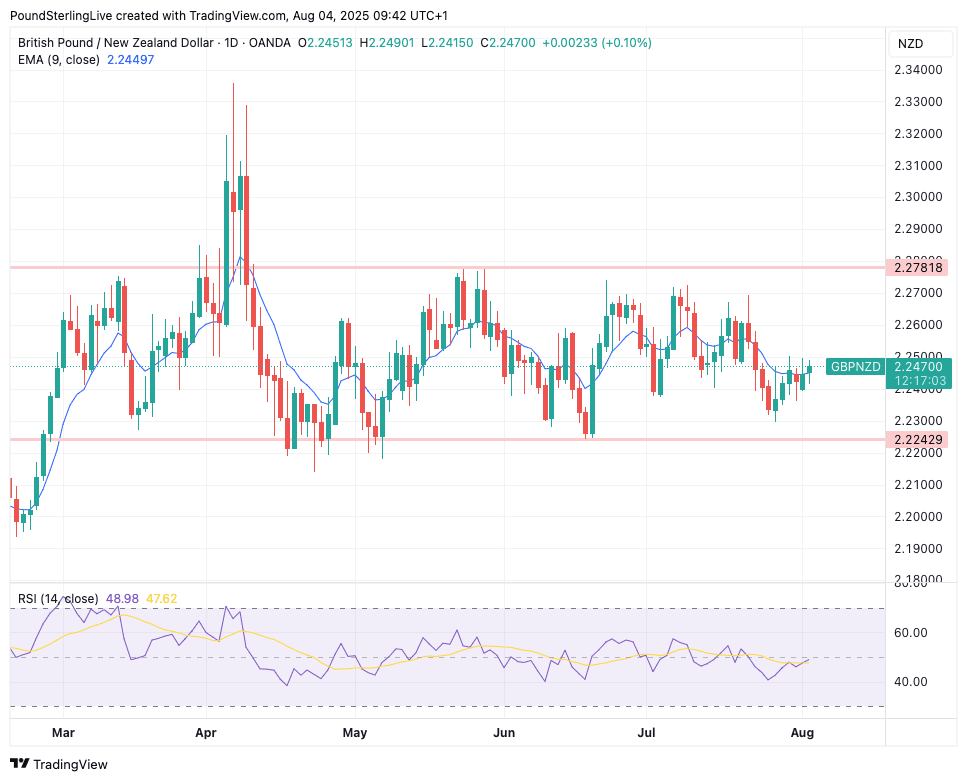

The Pound to New Zealand Dollar exchange rate (GBP/NZD) starts the new week at 2.2450, which is near the middle of the multi-month range of 2.2781 and 2.2242.

The pair is noticeably rangebound and trending sideways via a series of shallow rises and falls. We're in an upward oscillation at present, which suggests near-term price action should stay supportive and take us back above 2.2500 this week.

That being said, the prospect of any meaningful advance is strictly limited for now, given the flat technical indicators and mean-reverting tendencies that are so strongly on display.

The data calendar is relatively busy this week, with the Bank of England dominating GBP's outlook and some labour figures due out of New Zealand.

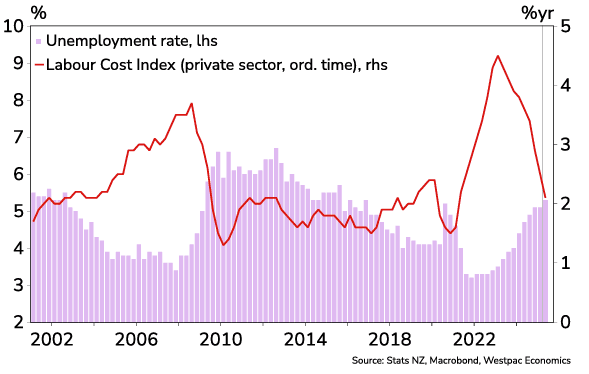

Midweek we get a New Zealand labour market report, where the unemployment rate is expected to be revised higher to 5.3% from 5.1% in the second quarter.

This would indicate a softening labour market that should dampen wage pressures and allow the Reserve Bank of New Zealand to cut interest rates further.

The market continues to assess an 85% probability of a 25bp cut at the RBNZ on 20 August, with another cut likely early in 2026.

These odds would be bolstered by a weaker-than-expected jobs report, which would weigh on the NZ Dollar this week. Should the figures be better than expected, then the Kiwi could recover and pressure GBP/NZD off its recent highs.

Above: NZ wage pressures are easing as unemployment rises.

The Bank of England's decision on Thursday should yield an interest rate cut of 25 basis points, which is widely expected.

With the rate cut 'in the price' of GBP/NZD, it falls to the guidance to shift the exchange rate: Does the Bank see the deterioration in the jobs market, and its associated slowing wage pressures, as reason enough to signal further hikes?

If so, GBP will come under pressure.

Or does the Bank remember its mandate is to bring inflation back to 2.0%, and signal a cautious approach is still warranted?

The arguments in favour of both are strong and it would not be unreasonable to think either side wins out. However, we think this seemingly contradictory economic fundamentals will simply translate into another divided Monetary Policy Committee vote, which should ensure the status quo remains intact.

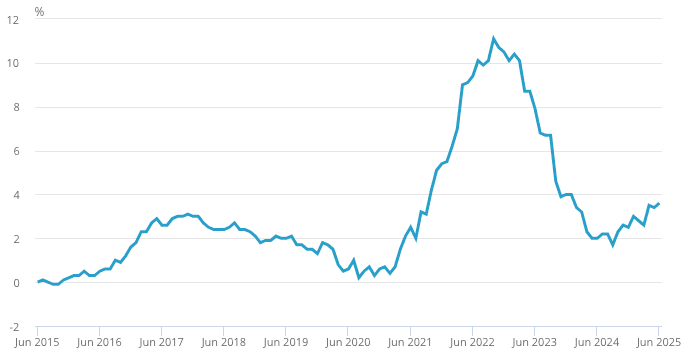

UK inflation is rising again, making it tricky for the Bank to justify an acceleration in interest rate cuts.

As a reminder, that status quo is the preference to maintain a quarterly pace to the cutting cycle, while retaining an ambiguous guidance whereby the Bank says risks to inflation lie to the upside and downside and that it will continue to monitor the data.

Given the scope of the GBP's recent decline, we would imagine that the market is already relatively pitted against Sterling, meaning that it will take a noticeably 'dovish' policy event to trigger a turn lower in GBP/NZD. Given this, the risks are skewed to the upside for the exchange rate if cautious guidelines are maintained.

"We have a hawkish Bank Rate forecast, expecting August to see the final cut this year, and the last cut until after 2027," says Rob Wood, Chief UK Economist at Pantheon Macroeconomics.