Image © Adobe Images

The pound is forecast to lose further value against the New Zealand Dollar this week.

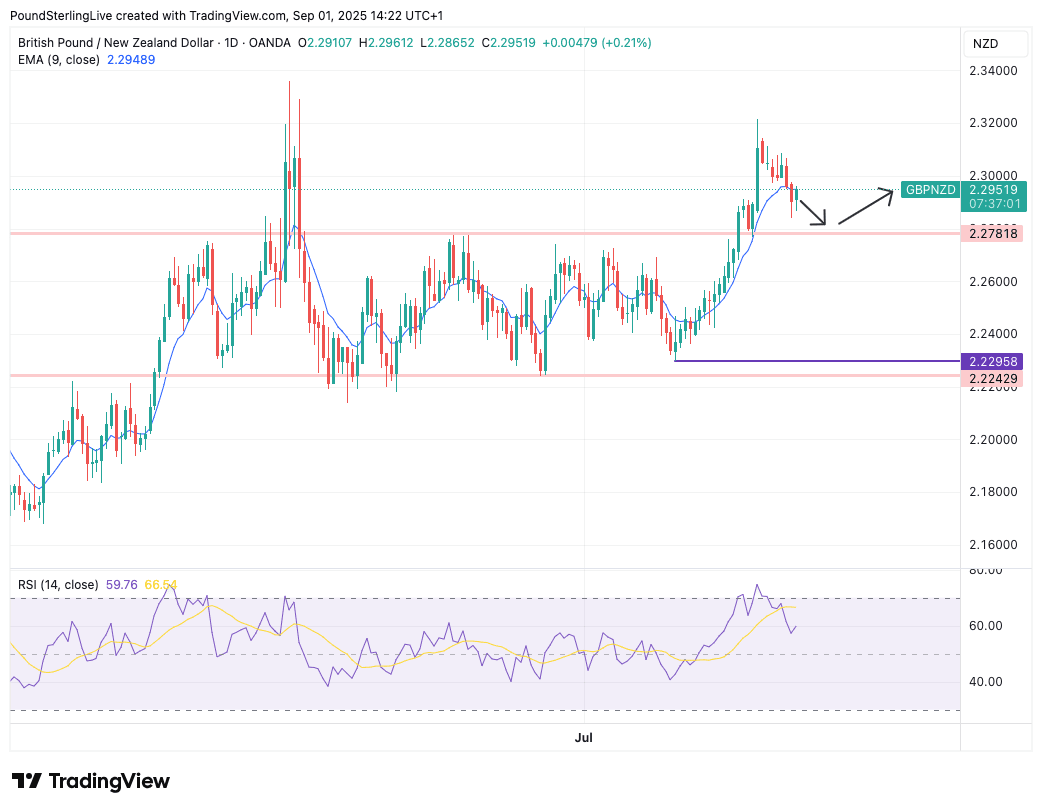

The Pound to New Zealand Dollar exchange rate (GBP/NZD) looks susceptible to further weakness in the coming days, although losses should be contained.

The big, multi-year uptrend in GBP/NZD is intact; it drove the pair to break into a new, higher range in late August, with Aug. 20 seeing a high printed at 2.3216.

The gains were rapid and the achievement of that peak coincided with the exchange rate becoming overbought and needing to take a breather in the form of a pullback.

That pullback is underway, and because we regard it as a correction from overbought conditions, the extent of the decline should be limited and does not indicate a turn in the trend.

Those with GBP purchases should consider locking in a portion of their payment exposure at current rates, given they are historically elevated, while setting orders for a return to higher levels, if you can afford to wait.

The Week Ahead Forecast model looks for a return back down to 2.2781, which is the previous resistance level that capped the exchange rate for much of the year.

That cap now turns to a floor that can offer Pound Sterling support during periods of weakness.

We look for that support to hold and potentially evolve into the lower-bound of a new, higher range in GBP/NZD that sits above the range that constrained the pair during the February-August period.

GBP/NZD is below the 9-day exponential moving average (EMA), which confirms our Week Ahead Forecast model anticipates downside in the next five days.

Weakness here is consistent with softness right across the GBP strip, where subdued trade is seen against most peer currencies at the start of the new month.

This weakness likely reflects a growing anxiety about the UK's economic and fiscal outlook as the UK government continues to spend more than it thought it would need to. The response will be higher taxes in the Autumn, which will potentially weigh heavily on households and businesses.

The cost of borrowing to fund the deficit is growing as lenders demand a greater premium when lending to the government, with some long-dated bond yields nearing multi-decade records.

This cocktail poses a risk to GBP in the coming months.

However, the New Zealand Dollar continues to underperform, allowing Sterling to make gains despite worries centred on the UK.

This NZD weakness comes despite rising global equity markets, which is indicative of a bullish global investor backdrop that traditionally bolsters the Kiwi Dollar.

Failure to respond to this supportive backdrop signals ongoing concerns about the state of the NZ economy and a realisation that further RBNZ rate cuts are to come, which is proving a decisive drag on NZD.