Image © Adobe Images

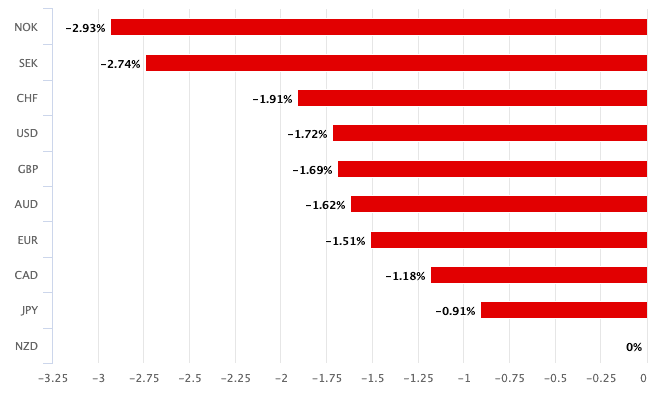

The New Zealand dollar has underperformed every other G10 currency over the past month, with relative performance data showing a decline of nearly 3 per cent.

ASB says the weakness reflects the Reserve Bank of New Zealand's more aggressive easing stance amidst signs of a stalling economy.

"The RBNZ cut the OCR by 25bp to 3.00%, consistent with the policy guidance that the RBNZ signalled back in the May MPS," ASB writes, referencing the August policy decision where interest rates were cut by 25 basis points.

However, the Committee vote split was 4-2 in favour of a 25bp cut versus a 50bp cut, highlighting the unexpected depth of the easing bias, which duly weighed on the NZD.

"If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further," said the RBNZ.

ASB notes the OCR track was "shaded down relative to the May MPS projections" and is "projected to end the year at 2.71%… signalling the likelihood of a further 50bp of OCR cuts by year end… and a 2.50% OCR."

The downgrade in forecasts is paired with a softer economic outlook:

"Views on the NZ economic outlook have softened, with both global and local headwinds,” ASB says, noting that growth and labour market forecasts were also marked lower. A broad range of indicators suggest that significant spare capacity in the New Zealand economy persists,” the report states, citing an output gap of −1.8% in Q3 2025".

Above: NZD on a one-month timeframe.

That gap is expected to push "overall inflation down towards 2%" after a near-term peak of 3% in Q3, reinforcing the case for additional easing.

ASB says New Zealand's economic recovery has effectively stalled, with household and business spending constrained by policy uncertainty, falling employment, higher essentials prices, and declining house prices.

The report notes that consumption has "failed to fire despite OCR cuts," citing weak household income growth and subdued house prices as limiting factors.

The impact on the NZ Dollar is notable: The NZD lost −2.93% against NOK, −2.74% against SEK, and −1.72% against USD over the past month, while sliding −1.69% against GBP and −1.51% against EUR.

Against the pound, the decline is particularly notable given sterling’s own mixed performance, leaving GBP/NZD stronger by nearly 1.7%.

ASB concludes: "We now expect a further 50bp of cuts before year end and a 2.50% OCR as the RBNZ frontloads policy stimulus."

This policy trajectory explains why the New Zealand dollar has emerged as the G10 laggard, with monetary divergence and soft domestic fundamentals weighing heavily on investor demand.