Image © Adobe Images

The New Zealand Dollar is falling amidst disappointment in China and growing odds of an interest rate cut at the Reserve Bank of New Zealand (RBNZ).

Auckland Savings Bank (ASB) says it has again revised its expectations for an RBNZ cut, bringing forward the start date to October, with a swift follow-up cut in November.

This is the second revision to the bank's RBNZ rate cut call this July, reflecting a broader reappraisal of RBNZ expectations that has weighed on the NZD.

"NZD eases on lower NZ interest rate expectations," says Chris Tennent-Brown, Senior Economist at ASB. "Inflation pressures are falling fast enough that the RBNZ doesn’t need to wait for the release of the Q3 CPI data."

Last week, New Zealand reported that its headline inflation rate fell to 3.3% year-on-year in the second quarter from 4.0% in the first quarter. ASB notes that various measures of core inflation, "including in the RBNZ’s sectoral factor model, fell noticeably."

Foreign exchange markets are sensitive to shifting interest rate expectations. New Zealand has the highest base rate in the G10, but markets think it also has the greatest scope to cut.

The quantum of incoming cuts is being reassessed, and for the NZD, this is a headwind.

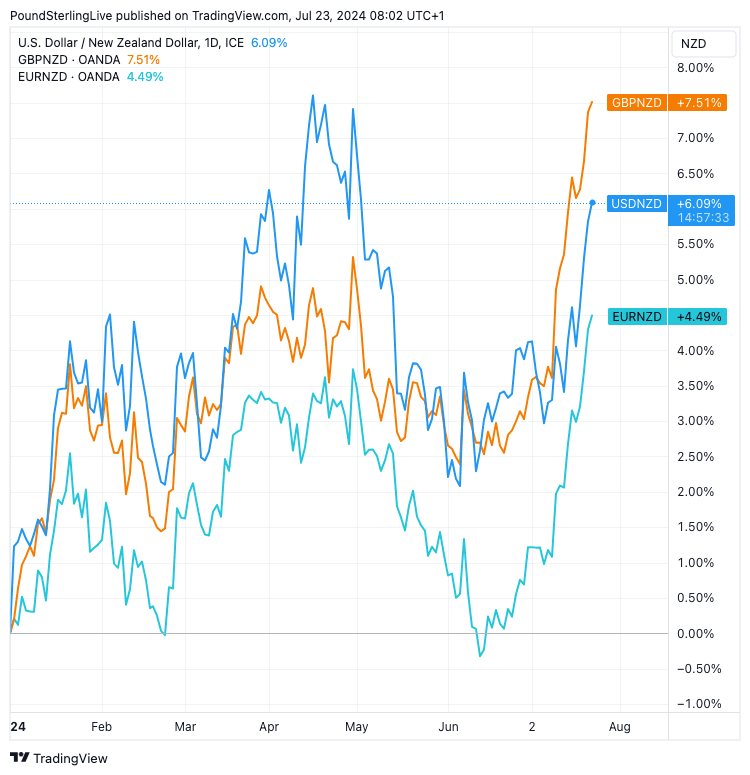

The New Zealand Dollar has already fallen 4.3% against the British Pound in July, putting it on course to register its largest monthly loss since September 2022. Against the Euro it is 3.72% lower and against the U.S. Dollar the monthly loss stands at 2.10%.

Above: Key NZD exchange rates in 2024. Track NZD with your custom alerts; find out more here

The New Zealand Dollar started the new week with fresh losses as investors expressed disappointment that Chinese authorities did not announce any significant new steps to boost the economy, which is a key source of demand for Kiwi exports.

"Markets are underperforming on continued disappointment following the Third Plenum and also concern over the rationale for the PBOC’s surprise interest rate cut yesterday," says Jim Reid, an analyst at Deutsche Bank.

The plenum is a five-yearly top-level meeting which, on occasion, has delivered important signals of Beijing's grand economic strategy. The Third Plenum was seen to offer continuity and was therefore short on any major stimulus initiatives.

The PBoC, meanwhile, cut interest rates, but markets think the cut is a sign of weakness, as it suggests that Chinese authorities are worried about the economy.

The PBoC cut the 7-day reverse repo rate, together with the 1-year and 5-year loan prime rate.

"The move was somewhat of a dovish surprise to markets, given that most participants expected the PBOC to wait for better clarity from the Fed or the July Politburo meeting before cutting, and was also somewhat unusual given it was announced much earlier at 8AM," says Michael Wan, Senior Currency Analyst at MUFG Bank Ltd.

"The surprise rate cuts by the PBoC on Monday can be seen as a signal that Beijing is concerned about the economy and is actively trying to support growth and meet the 5% target for this year," says Tommy Wu, Senior Economist at Commerzbank.