Image © Adobe Images

The Pound to New Zealand Dollar exchange rate (GBP/NZD) is set to retreat in the coming days as the uptrend takes a breather.

The Kiwi Dollar strengthens at the start of the new week alongside its fellow antipodean, the Australian Dollar.

Both have been boosted by supportive news from China, where the policy-setting politburo signalled that authorities will likely be more proactive in supporting the world's second-largest economy in 2025.

Today's Politburo's official announcement stated that China's policy stance would now become 'moderately loose', whereas previously, it was to be 'prudent'.

This is the first time such a stimulative stance has been adopted since late 2010.

Further support could bolster the Chinese economy, New Zealand's most important export destination, explaining why NZD and AUD are often traded as China proxies.

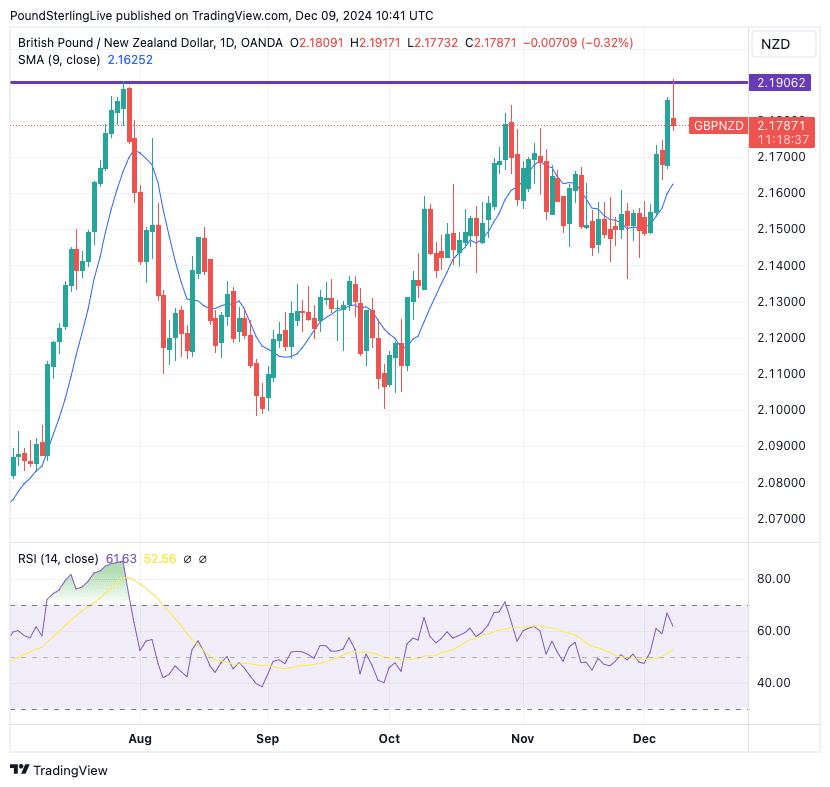

The impact on the GBP/NZD chart of these developments is a pullback from recent highs:

As can be seen, the retreat to 2.1774 follows a test of the horizontal resistance line at 2.19, which could mark a near-term limit.

2.1906 is the previous 2024 peak and a setback for GBP/NZD here on Monday will illustrate it to be a resistance level that traders sell into, thereby denying GBP further upside.

Note, too, that the Relative Strength Index (RSI) was close to overbought last week as it approached 70 but has since turned lower.

Also, GBP/NZD is trading well above its 9-day moving average, which it prefers to hug.

Thus a retreat to approximately 2.1624 could be in store for the next few days.

But bigger picture, the setup remains constructive, and we could see further GBP/NZD upside as markets anticipate another 50 basis point cut from the Reserve Bank of New Zealand in 2025.

The Bank of England is meanwhile expected to forgo another rate cut in December, while only 100 basis points of cuts are priced in for the entirety of 2025.

This means UK interest rates will be elevated relative to those of New Zealand, which would imply GBP/NZD upside as capital tends to flow from low interest rate regions to where interest rates are higher.

Looking at the calendar, it's a quiet week ahead for New Zealand, which can allow the aforementioned technical pullback in GBP/NZD to evolve.

Watch U.S. inflation data midweek, which could shake markets. An above-consensus reading would spark some USD buying and a potential setback to global stock markets.

The NZD has a higher correlation with global equities than GBP, which would imply GBP/NZD recovery.

In the UK, Friday brings GDP and output data for November.

Analysts think the economy contracted by 0.1% month-on-month in October. Anything deeper is likely to weigh on the Pound, as this would encourage investors to bet on more Bank of England rate cuts in 2025.

Anything stronger, and GBP could strengthen into the weekend. Also of interest on the day will be GfK consumer confidence data, where we will be looking for evidence of further consumer sentiment deterioration in the wake of the government's budget.

The big releases for the Pound come next week, when inflation and labour market figures are released. These figures should provide some finality to expectations for the December 19 Bank of England interest rate decision.