Image © Adobe Images

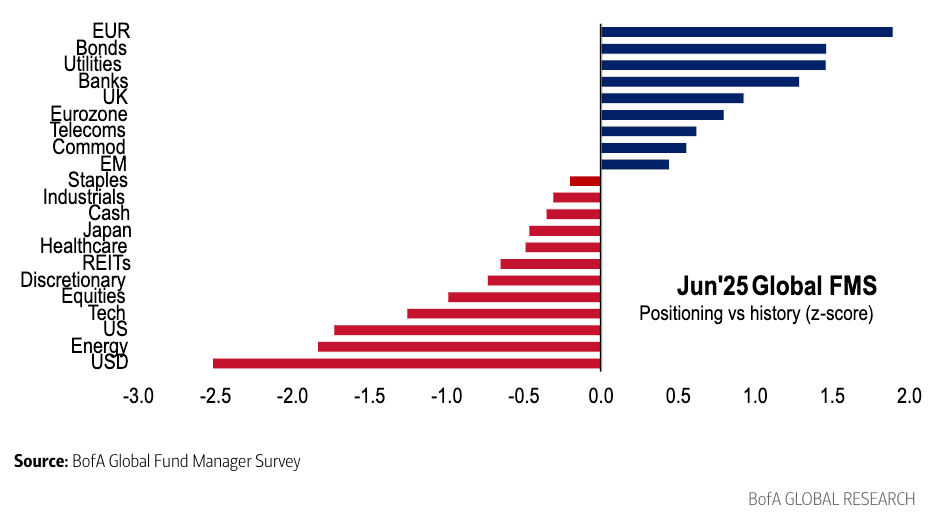

"Relative to history, investors are overweight the Euro, bonds, & utilities and are underweight the U.S. dollar"

Global fund managers are more underweight the U.S. dollar than at any point in the past two decades, according to Bank of America’s latest Global Fund Manager Survey, reflecting a major shift in sentiment amid concerns over U.S. fiscal stability and diminishing rate support.

The June survey, which polled 206 participants managing a collective $640 billion in assets, found that net investor positioning on the dollar has fallen to its lowest level since 2004.

This marks a stark reversal from recent years when dollar strength dominated global currency markets on the back of aggressive Federal Reserve tightening and safe-haven flows.

"Relative to history, investors are overweight the Euro, bonds, & utilities and are underweight the U.S. dollar, energy, & US stocks," says Bank of America.

Above: Positioning vs history (z-score). Relative to history fund managers are overweight the Euro, bonds, utilities vs underweight US$, energy, US stocks.

Bank of America attributed the shift to a growing consensus that U.S. exceptionalism is fading.

"Confidence in the dollar as a safe haven has been damaged: in the wake of the introduction of tariffs, US Treasuries were sold, and with them the dollar, which was thus not in demand as a safe haven as is usually the case. In addition to economic concerns, increasing fiscal risks have also played a role in this recently," says Thu Lan Nguyen,

Head of FX and Commodity Research at Commerzbank.

Softer U.S. growth data, coupled with sticky deficits and political uncertainty in an election year, have left investors questioning the dollar’s long-term appeal.

Meanwhile, expectations for Fed rate cuts later this year have reduced the greenback's yield advantage. Yield advantage describes how U.S. bond yields have been elevated relative to elsewhere, attracting foreign investor demand, which benefits the Dollar. Declining yield advantage is cited by analysts as a significant factor behind USD weakness in 2025.

"The USD is the most underweight it’s been in 20 years," the report says, adding that this de-dollarisation of portfolios aligns with broader moves into non-U.S. assets, including European equities and emerging market debt.

The Dollar extended a multi-month decline that saw the Dollar index - a measure of broader USD performance - fall to its lowest level since March 2022 last week.

According to the BofA survey, global growth optimism remains intact, but investors increasingly prefer assets tied to currencies they view as undervalued or less exposed to U.S. policy volatility.

The results suggest that a protracted spell of rich valuation and overweight allocations, the dollar is falling out of favour with institutional money managers.