Image © Adobe Images

Some food for thought for those watching the Pound to Dollar exchange rate (GBP/USD) at the minute.

The Dollar has certainly come under pressure in 2025, and the selloff is not necessarily over.

However, a pause appears to be setting in, with scope for a more meaningful recovery starting to build.

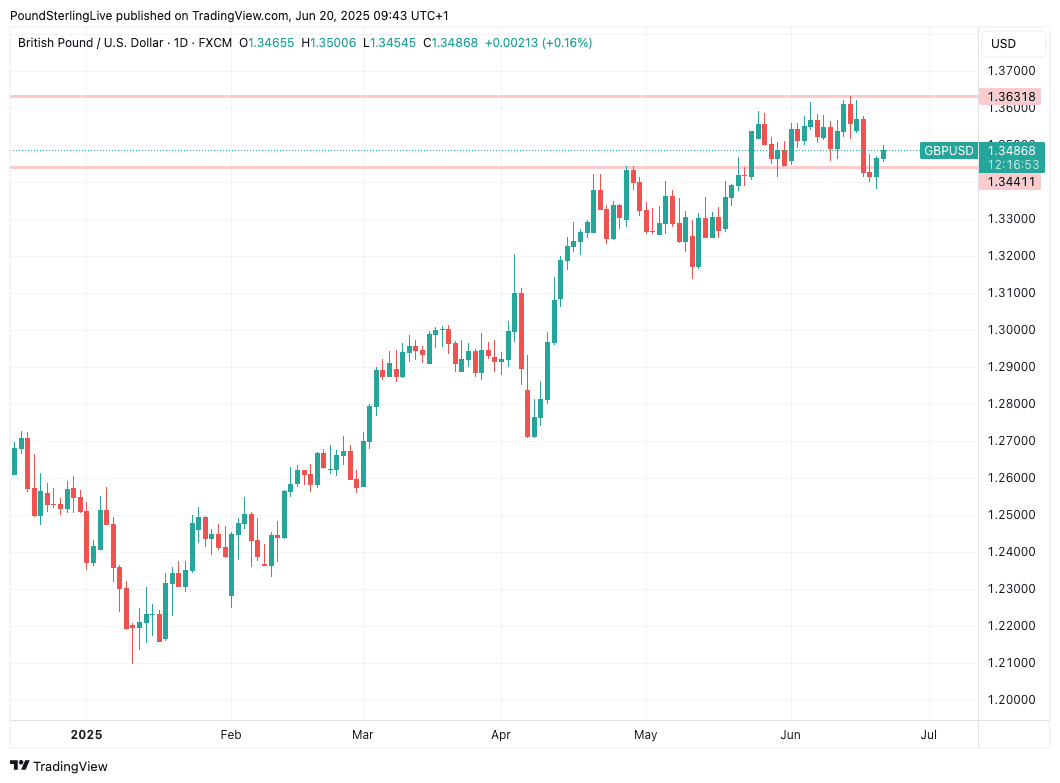

This leaves the likes of the GBP/USD at risk of a deeper retrenchment from highs at 1.36 over the coming days and weeks.

According to Humphrey Percy, analyst at SGM Foreign Exchange Ltd, such a development would make a lot of sense right now.

He explains:

"All the talk of the USD having had its day may be gaining in credence every day that goes by with the POTUS and his Administration seemingly determined to dismantle the post WW2 global currency order and depreciate the USD, but most people operate in a much shorter timeframe than the time it will take to engineer a global shift in USD’s strategic importance."

"Shorter term currency decision making encompasses asset acquisition in the current financial year, repatriation of profits, taking a vacation, sending a lucky child to study in a foreign country or electing to emigrate as examples.

"For the twin prime reasons of ultra high geo-political uncertainty, and the lack of a credible alternative given that USD accounts for 88% of one side of all currency transactions globally, for the next 6 months at least USD remains a currency to buy rather than sell."

Above: GBP/USD is in a clear uptrend, but is the case for a pullback building over the coming months?

The Dollar has certainly lost its shine this year amidst the U.S. President's isolationist tendencies, coupled with his trade mark erratic and transactional approach to international affairs.

The uncertainty has dented the appeal of the U.S. Dollar and U.S. assets generally, prompting a fall in value.

Analysts at Société Générale say they see signs of "de-dollarisation" in global financial markets, as central banks and institutional investors diversify away from U.S. assets in response to geopolitical risks, policy unpredictability, and structural shifts in the global economy.

Société Générale’s latest fund flow analysis also identifies structural shifts in capital allocation. U.S. equity and bond markets are seeing relatively weaker foreign inflows compared to previous cycles, particularly from reserve managers and sovereign wealth funds.

Meanwhile, allocations to non-U.S. markets, especially in Asia, have steadily increased.