Image © Adobe Stock

The Pound is forecast to remain under pressure against the Dollar in the coming week.

The British Pound gapped lower in early Monday trade as global markets responded to weekend news that the U.S. had bombed Iran's nuclear facilities, with fears mounting that Iran will respond by closing the critical Strait of Hormuz to shipping.

The Strait carries about a fifth of the world's oil, and any disruption would cause a spike in prices that will substantially lower the growth prospects for the world economy.

Initial market reactions show Brent crude oil briefly surpassed $80 p/b but eased back to $78. The dollar gained, the pound softened.

"The moves are limited and orderly. This might suggest that markets consider the Iran conflict will remain regional," says Mathias Van der Jeugt, analyst at KBC Bank.

"At the same time, for markets it also becomes ever more difficult to hedge/react to (geopolitical) event risk that might again change very soon. In this respect, this modest reaction also feels a bit like ‘paralysis’ and being unable to anticipate the next step," he adds.

The closure of the Strait of Hormuz was still considered a low-odds outcome until Saturday. However, odds are now decidedly higher, and any attempt to close it would be supportive for the Dollar in two obvious ways:

1) Oil is priced in USD, meaning higher oil prices = greater demand for the USD. The U.S. is also the world's biggest oil producer, meaning its terms of trade could actually improve if export values rise.

2) The U.S. Dollar is still a safe-haven in times of geopolitical tensions, meaning investors tend to opt for the safety of USD cash when markets are falling and risks are rising, as would be the case on further escalation in the Middle East conflict.

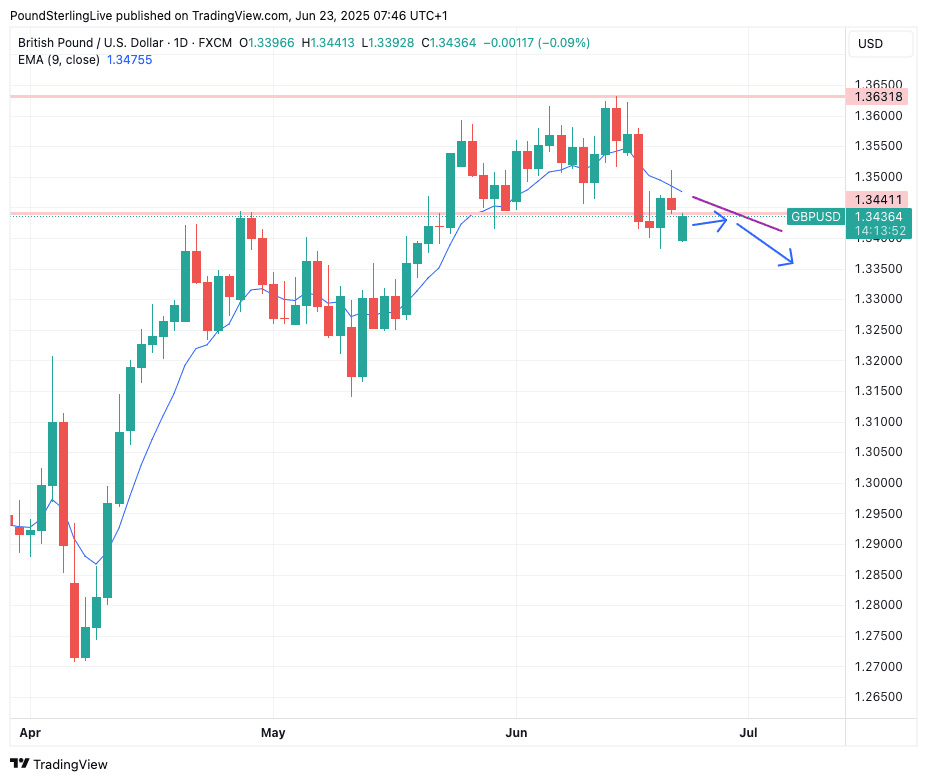

This all translates into a drawdown in the Pound to Dollar exchange rate (GBP/USD) to 1.3432 at the time of writing, from highs of 1.3631 reached on Friday, June 13.

Above: GBP/USD at daily intervals.

This looks to have been the interim peak for the 2025 rally, and a retracement from these highs is underway.

The exchange rate has slipped below both the nine-day exponential moving average (1.3474) and the horizontal graphical support at 1.3441, with both developments advocating for a heavier tone to proceedings.

Given this, we would look for an eventual move to 1.3550 later in the week.

Note that the GBP/USD could revert higher to the nine-day EMA in the short term, particularly amidst any wait-and-see price action in financial markets as investors await further developments in the Middle East.

However, given the emerging setup, strength would be considered a short-term phenomenon that will ultimately be sold into.

To be sure, the bigger picture remains one in which the Dollar is declining following multi-year overvaluations, but a rebound could be in store over the summer months.

"For the twin prime reasons of ultra high geo-political uncertainty, and the lack of a credible alternative given that USD accounts for 88% of one side of all currency transactions globally, for the next 6 months at least USD remains a currency to buy rather than sell," says Humphrey Percy, analyst at SGM Foreign Exchange Ltd.

The Week Ahead

Geopolitics will be the key driver of GBP/USD in the coming week, however, there are some calendar events that should provide some interest.

Upcoming data and events come in the context of a UK economy that has churned out disappointing data over the course of the past month, and this has weighed on GBP more broadly.

?? United Kingdom

? Monday, 23 June

S&P Global UK PMIs (June, preliminary) at 09:30 BST:

Composite PMI: Watch for movement around 53.0 level.

Services PMI (prior: 50.9): Expected to rise to 51.3.

Manufacturing PMI: Directional surprises could sway sentiment.

? Key Sensitivities: Watch employment and business costs, recent releases flagged dovish risks.

? Tuesday, 24 June

BoE Speakers:

Greene at 10:30 BST

Ramsden at 14:35 BST

Bailey (Governor) at House of Lords hearing at 15:00 BST

Breeden at 16:50 BST

? Market Implication: No major policy shift expected, but tone on inflation and growth will be monitored. Markets still lean toward an August rate cut.

? Wednesday & Thursday, 25–26 June

BoE Lombardelli speaks Wednesday at 09:45 BST

BoE Breeden and Bailey speak again on Thursday (09:30 and 12:00 BST respectively)

? Tone Watch: Commentary follows last week's decision to hold interest rates unchanged, although the odds of an August rate cut are elevated. Commentary is likely to reinforce this expectation, which will contribute to the Pound's soft underbelly.

?? United States Week Ahead

? Monday, 23 June

? Flash PMIs (June, preliminary):

S&P Global Composite PMI: Watch for signals on the overall economy

Services PMI: Previous: 54.8

Manufacturing PMI: Previous: 51.3

? Market Sensitivity:

Citi notes markets are “overly sensitive” to this data now.

Strong readings → USD support as they imply solid demand, inflation persistence.

Weak surprise → Could revive rate cut bets, pressuring USD.

? Tuesday, 24 June

? New Home Sales (May):

Prior: 634k

Consensus: Expected slight rebound

? Market Sensitivity:

Watch for signs of housing resilience.

Stronger print = continued domestic demand = USD supportive

Weakness may signal softening growth backdrop = USD mildly bearish

? Fed Governor Waller speaks at 17:45 BST (12:45 EDT)

? Market Focus:

His views are often closely watched; recent tone has been less dovish

Hawkish lean = supports USD; dovish tilt = pressures USD

? Wednesday, 25 June

? Durable Goods Orders (May):

Core Orders (ex-aircraft): Key component

Prior headline: +0.6%

? USD Implications:

Another positive print reinforces U.S. growth resilience → USD support

A slowdown or miss would pressure growth expectations → bearish USD

? Thursday, 26 June

? Q1 GDP (Final):

Previous: +1.3% (2nd est.)

Focus: Revisions to core PCE deflator and consumption

? Market Sensitivity:

Little change expected, but if inflation metrics revised up → USD positive

Weaker consumption or downward revision → softens USD

? Initial Jobless Claims:

Prior: 238k

Recent readings have trended higher

? USD Implications:

Above 250k could flag labour softening = USD negative

A drop back to low 230k = tight labour market = supports USD

? Friday, 27 June

? Core PCE Price Index (May):

Consensus: +0.1–0.2% MoM

Previous: +0.2% MoM

YoY Core PCE: Expected around 2.6% YoY

? Market Sensitivity:

This is the Fed’s main inflation gauge, meaning it matters. "For the USD to truly make a comeback, U.S. data has to improve and so too does the outlook for fiscal sustainability. US PCE and consumer confidence data will therefore be important," says Valentin Marinov, Head of FX Research at Crédit Agricole.

A hotter-than-expected number → delays rate cuts → USD bullish

A softer print could reignite dovish momentum → USD bearish

? Personal Spending & Income (May):

Strong consumption = supports growth narrative = USD positive

Weak data = less pressure on inflation = USD negative

? University of Michigan Final Consumer Sentiment (June):

Includes inflation expectations

? USD Implications:

Stable expectations = limited impact

Sharp shifts in inflation outlook could influence USD short-term