Image © Adobe Images

The pound to dollar exchange rate (GBP/USD) can rise before coming under pressure again over the coming days as U.S. data risks beating expectations.

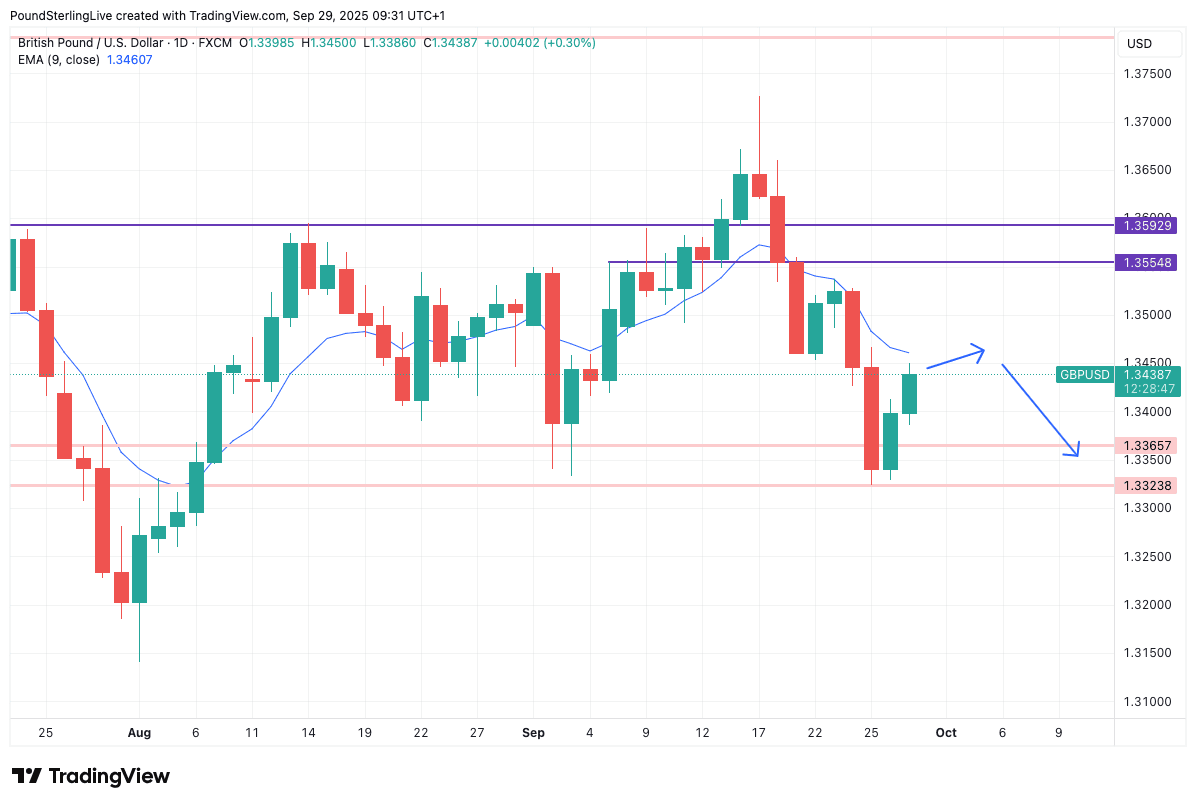

GBP/USD starts the new week with a spring in its step, extending a rebound from that solid floor of support that lies at 1.3365-1.3323.

This level has underpinned Sterling since May, forming the approximate lower-bound of a range that has been in place for much of the year:

The exchange rate bounced off 1.3323 last Friday and is building on that recovery through the early Monday session, in tune with a broader bout of USD weakness.

However, the pair remains below the nine-day exponential moving average (EMA) at 1.3459, which means our Week Ahead Forecast model signals ongoing weakness.

The assumption at this point is that the rally we are seeing on Monday can extend a little further, as GBP/USD washes out some recent weakness and technical considerations are respected.

However, for now, strength is likely to ultimately be sold into as traders target an extension of the broader USD rally.

Given this, a test of 1.33 and lower is possible in the coming five days.

In the UK, we will be watching the Labour Party's conference for further signs the government will be pressured to adopt more spendthrift policies that will require greater levels of borrowing.

In a world awash with debt, the UK will likely be challenged by markets before its fellow economies, for various structural reasons that we won't jump into in this article.

The bottom line, however, is that markets are concerned about the outlook for UK finances, and bad headlines could trigger selloffs in UK gilts (government bonds) and the pound.

We aren't saying it's a certainty for this week, but it is something we are highly alert of, noting episodes of nervousness can pop out of the blue.

Those with impending money transfers from GBP into USD should adopt a cautious approach given these risks.

If the GBP gets through the week unscathed, it will be the USD side of the GBP/USD equation that will be dominant, as is typically the case.

Last week, U.S. Treasury yields rose as investors responded to a mix of strong U.S. economic data and slightly 'hawkish' signals from the Federal Reserve, leading to gains for the dollar.

U.S. second-quarter GDP was upgraded to 3.8% annualised, marking the fastest pace of growth in nearly two years.

Such a clip of growth doesn't exactly scream of a need for the Federal Reserve to lower interest rates, drawing a massive question mark over the market's prior expectation that the Fed will cut rates at every meeting this year.

As the tide goes out on maximum Fed rate cut bets, so the dollar rises.

"Fed Chair Powell pushed back against expectations for aggressive rate cuts, emphasising the need to remain vigilant on inflation risks, while acknowledging the recent slowdown in jobs growth," says a note from Lloyds Bank.

In the U.S. this week, the theme of U.S. economic resilience and the debate about Fed rate cuts will continue, with ISM PMI survey data due for release (Wednesday: manufacturing ISM, Friday: services ISM).

These surveys will give a good snapshot of activity in September, and all indications point to a set of robust figures that can further bolster the dollar.

"Risks to US activity should gradually be shifting in a more positive direction, due to past monetary and upcoming fiscal easing and a more benign adjustment to the tariff shock," says Themistoklis Fiotakis, an analyst at Barclays.

Analysts are nevertheless wary that labour market data will disappoint, underpinning a picture of an economy that is shedding jobs, even if top-line activity is good.

Non-farm payrolls are the week's highlight in this regard, with the market looking for another downshift in job creation.

The expectation is for just 39K jobs to have been created.

For the dollar, any above-consensus outcomes will provide a boost and further pressure GBP/USD.