Image © Adobe Images

A short-term rebound in the Pound to Dollar exchange rate looks set to extend this week. The U.S. inflation data release is the key focus.

Pound Sterling has now risen for two consecutive weeks against the Dollar as it looks to claw its way out of a multi-week selloff that followed a spurt of above-consensus U.S. economic growth and the election of Donald Trump.

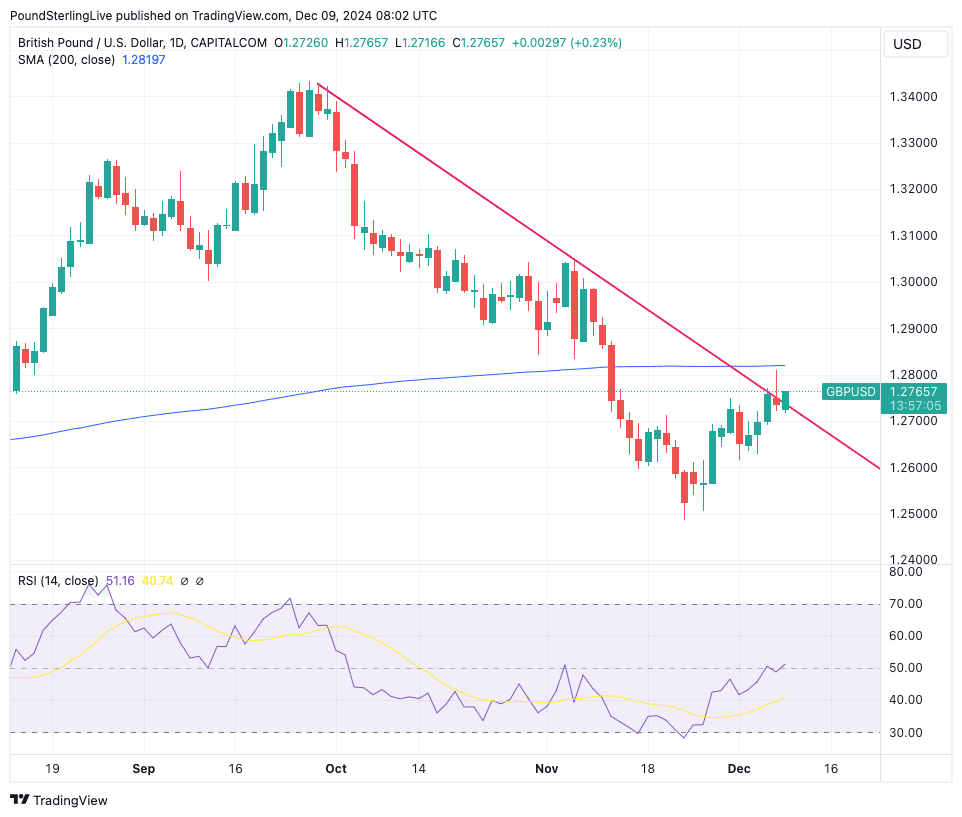

As the below chart shows, those claws are dug into the descending trendline, and a conclusive break above the line would be the latest, albeit tentative, signal that the Pound is in a near-term rebound:

Above: GBP/USD at daily intervals with descending channel and 200-day moving average annotated.

GBP/USD is again trading above the 21-day moving average, which would be the first key moving average that needs to be broken if the outlook is to flip to something more constructive.

The Relative Strength Index (lower panel) has turned constructive by rising above 50 and is still pointing higher, which advocates for near-term advancement.

However, the market is still below the more important trend lines, which are the 50- and 100-day moving averages. What is interesting, however, is that the 200-day moving average is close at hand at 1.2819, a level that appears to have provided resistance to Friday's attempted bounce after the U.S. job report.

We will watch this level closely, as a break above it would be an important technical development that favours further upside in the GBP.

More broadly, FX markets are currently experiencing a USD correction that can continue into the new year.

"The FX price action in recent days has highlighted the limits of the so-called 'Trump trade'," says Valentin Marinov, Head of G10 FX Strategy at Crédit Agricole. "In addition, the fact that U.S. rates and UST yields remain close to their recent lows has become a key headwind for the USD."

The U.S. Dollar ended Friday somewhat stronger following the release of the U.S. jobs report, although the strength was not significant. This suggests that the data release was largely in line with expectations.

To be sure, news that the U.S. economy added 227K jobs in November while the unemployment rate rose to 4.2% won't prevent the Federal Reserve from cutting interest rates again next week.

But there is one more major data release that will influence the Fed's decision: Wednesday's inflation release.

"The focus shifts to this week’s inflation print on Wednesday," says Dominic Schnider, Strategist at UBS Switzerland AG. "This marks the last important data point before the Federal Reserve meeting on 18 December."

The market expects headline CPI inflation to be 0.2% month-on-month and 2.7% year-on-year.

"Markets expect CPI, as well as the core measure, to remain broadly unchanged and see a 75% chance of a December rate cut. We think the Fed will lower rates by 25bps at the meeting, which would weaken the dollar into the year-end. Furthermore, the USD also seems to be consolidating from a technical perspective," says Schneider.

Should the inflation numbers beat expectations in a more convincing fashion, then the U.S. Dollar can stage a more meaningful rebound as the market would lose confidence in a December rate cut.

Pound Sterling sees some risk on Friday when UK economic output data is revealed.

Analysts think the economy contracted by 0.1% month-on-month in October. Anything deeper is likely to weigh on the Pound, as this would encourage investors to bet on more Bank of England rate cuts in 2025.

Anything stronger, and GBP could strengthen into the weekend. Also of interest on the day will be GfK consumer confidence data, where we will be looking for evidence of further consumer sentiment deterioration in the wake of the government's budget.

The big releases for the Pound come next week, when inflation and labour market figures are released. These figures should provide some finality to expectations for the December 19 Bank of England interest rate decision.